✍️ The S&P 500 Report: Performance, Profitability & Special Metrics – #Ed 4

Dear all,

first of all, thank you very much to all the folks that did donate/tip this ad free & paywall free publication which is all about independent investment research. Namely, hats off to Vinny G., Johanna K., Darryl B., Arny T., Don C., Rhino I., and all the anonymous individuals that showed their generosity which is highly appreciated! (for privacy reasons, I didn’t post the full name which is the best approach I would say).

Now it’s December, that special time of the year when many people do a lot of good and engage in charity work. This time around my huge request is to NOT donate/tip and support my publication, but choose maybe the local community where you live: could be financial support, sorting out your home with clothes, shoes, devices, toys, anything that you do not really need! Your own personal work & time is awesome also!

Thanks, appreciate & as always: give your best shot to be a positive force out there!

Welcome to the 4th edition of the S&P 500 Report, a unique report via data driven research & visually appealing charts that simply tell 10,000 words. If you know a better and more comprehensive S&P 500 coverage (free or even paid), please let me know!

This S&P 500 coverage focuses on Performance, Profitability & Special Metrics. Valuation focus and deep dive will be covered in the dedicated ‘Valuation’ section.

A perfect time for another S&P 500 deep dive now that the Q3 2023 earnings are out.

Structured in 7 parts + bonus charts & designed to have a natural flow:

📊 Performance Ins & Outs

📊 Earnings, Profitability, Flows, Value & Growth

📊 Sentiment & Chatter

📊 Seasonality, Volatility & Breadth

📊 Technical Analysis: Short Term & Long Term

📊 The 11 Sectors Performance Breakdown

📊 Special & Alternative Metrics

👍 Bonus Charts 👍

📊 Performance Ins & Outs

👉 Bears Make Headlines & Lose Money, Bulls Make Money! As always …

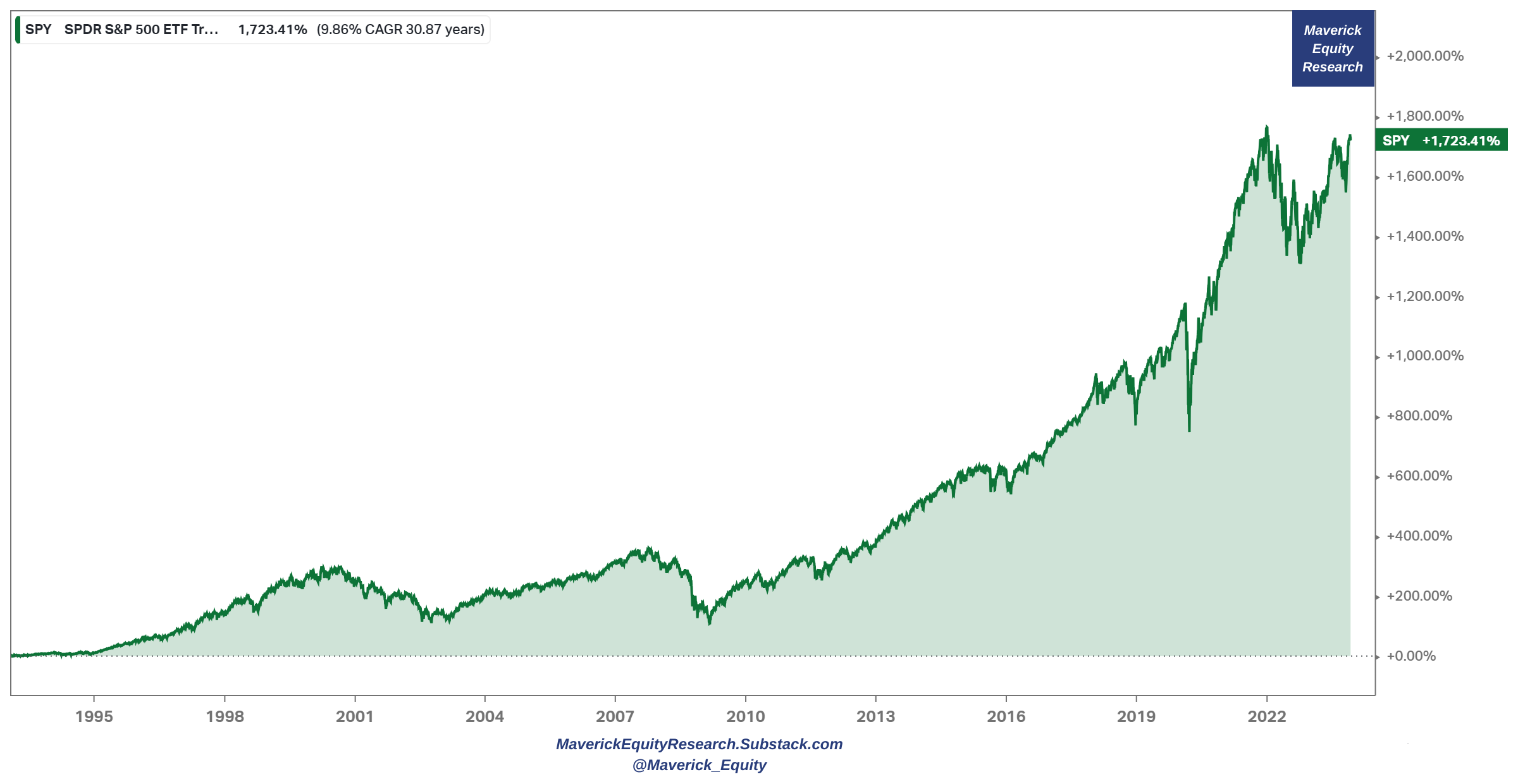

S&P 500 last 30 years: +1,723% return with 10% CAGR … compounding surely works …

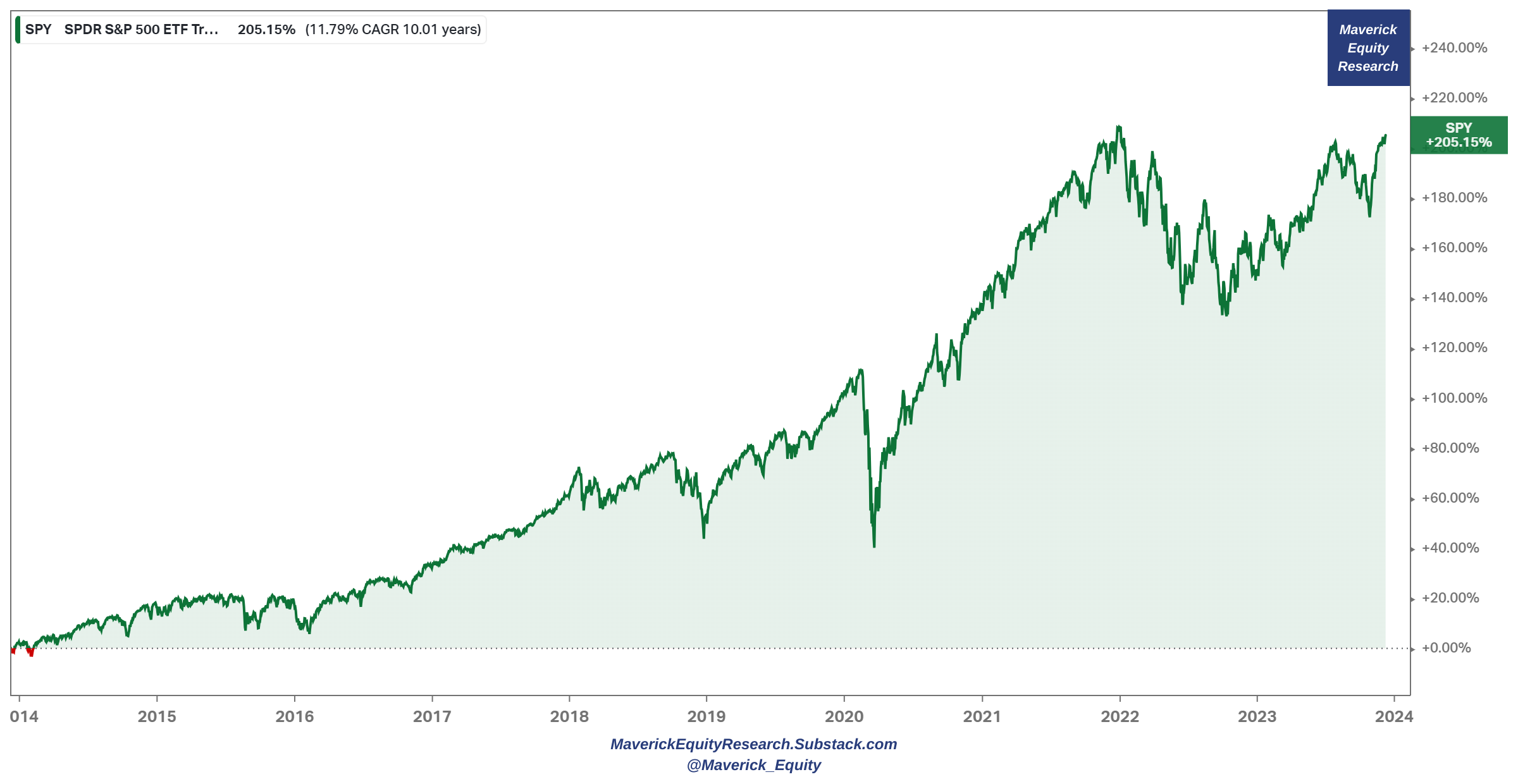

👉 Last 10 years, more than tripled at 205% and 11.8% CAGR …

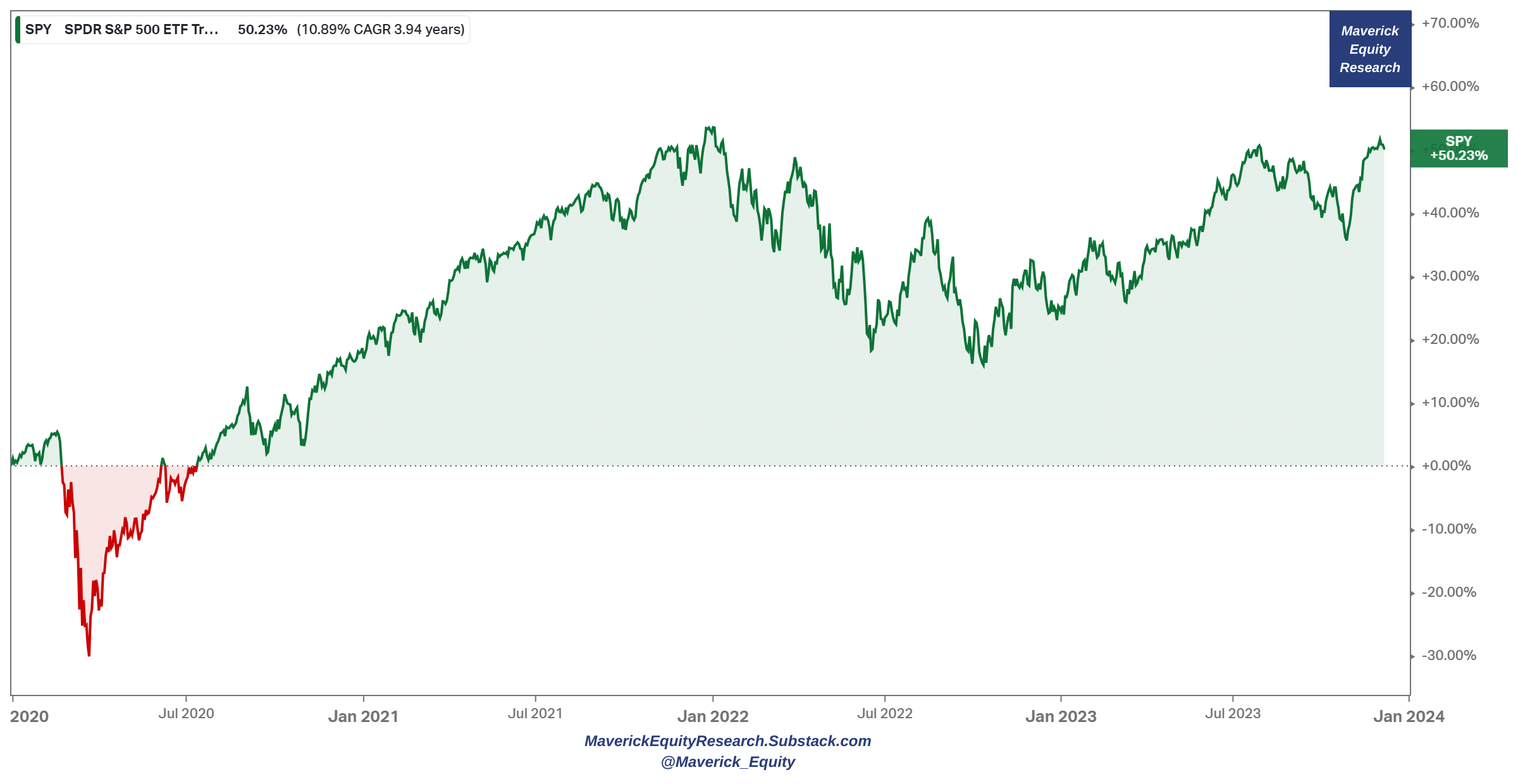

👉 Since 2020 we had many outliers: a pandemic, ramping inflation & interest rates (from 0% to 5.5%), an energy crisis, some banks that went bust (Credit Suisse in Europe, SVB & FRC in USA), a worldwide bottled supply chain, a war in Europe, then now Israel Hamas war …

A key question now: how did the S&P 500 do despite all that? Let this one sink in:

-

+50% = 10.8% CAGR to investors = very very good … given the recent context!

-

Recall “The first rule of compounding: never interrupt it unnecessarily.” Munger

-

for that not to happen, one should have a solid plan, a good broker that does not charge them very high fees, and consider taxes when optimising own investments

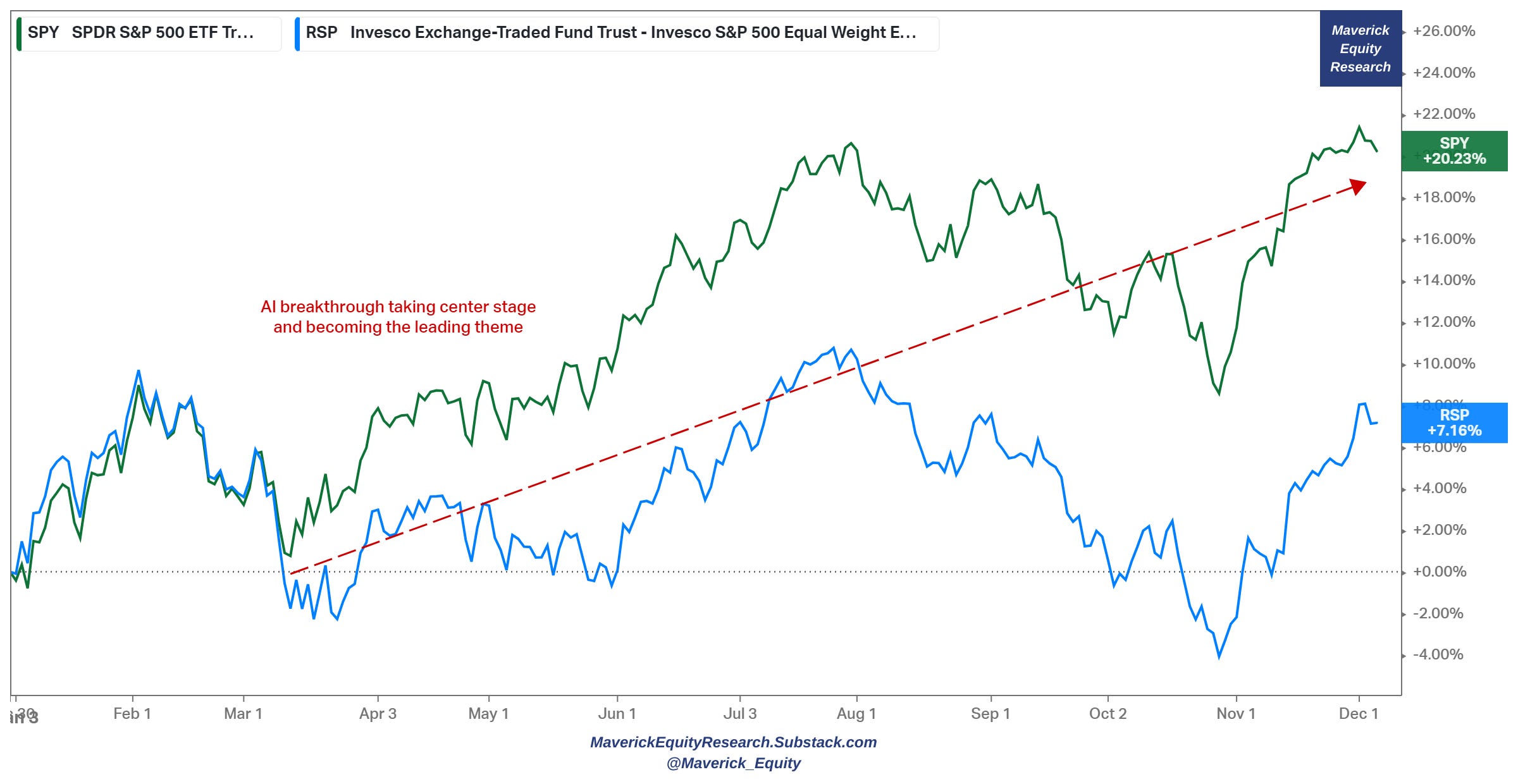

👉 2023 performance now: great +20% for SPY while note the unweighted RSP +7%

-

divergence started in March when the recent AI breakthroughs & narrative took over completely the center stage

-

I am quite certain that there will be big AI winners in the next 5-20 years, though also certain that many will pump their AI capabilities and real world use cases, hence hype is almost a given, hence down the road many will naturally deflate…

👉 this signals us that the 20% SPY return must be concentrated and not distributed

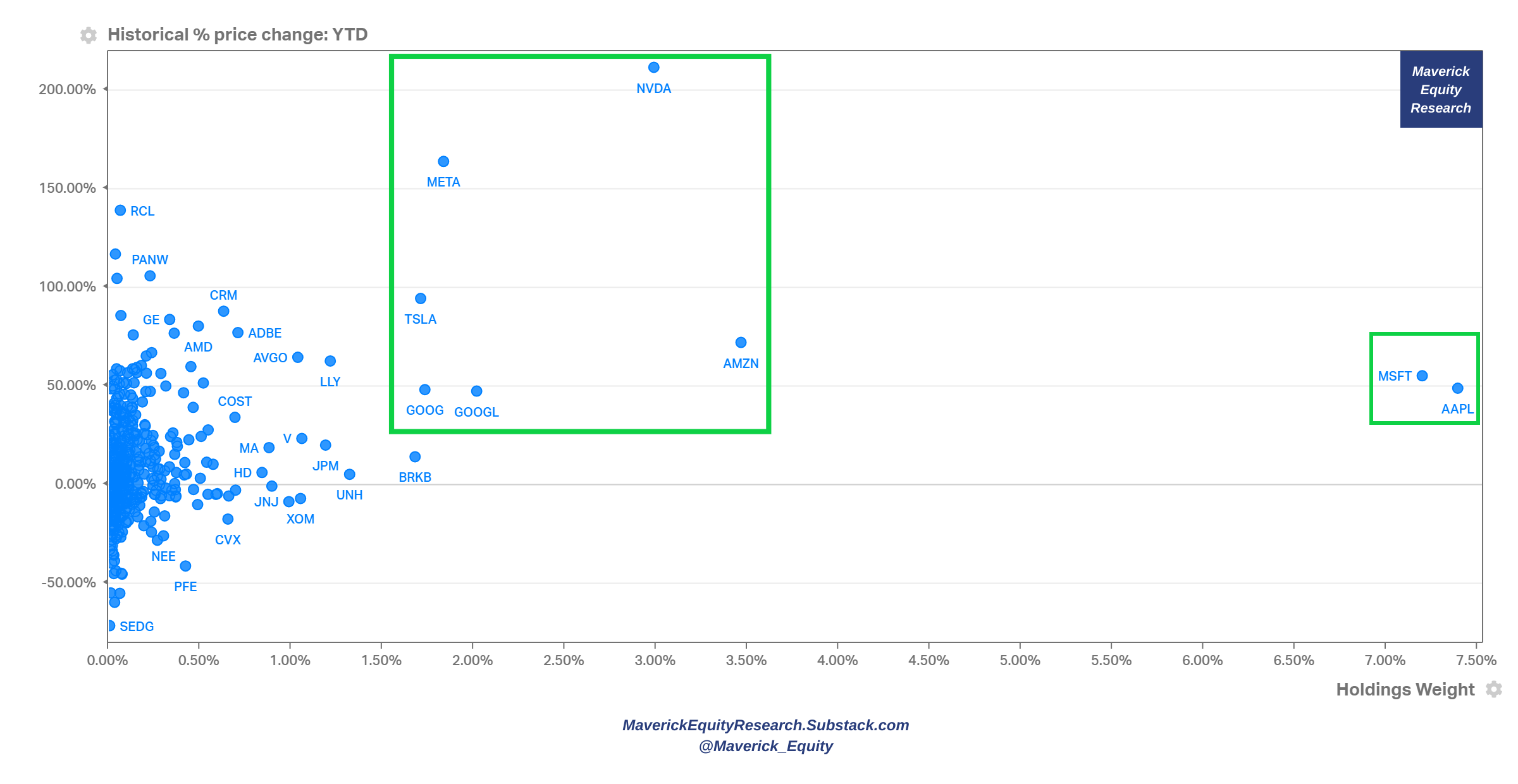

Let’s chop the SPY and look inside of it via: 2023 % returns & the holdings weightings

-

guess who is there with the big weights & big returns? The techie Magnificent 7: Apple, Microsoft, Google, Amazon, Nvidia, Meta and Tesla

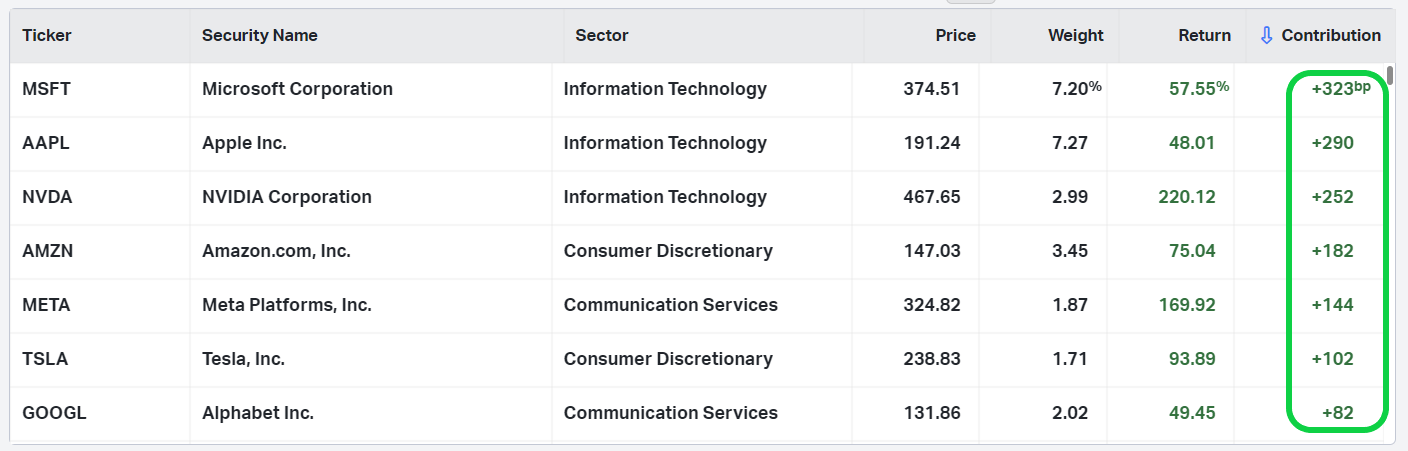

Let’s make that visual into raw numbers via a return attribution analysis to see the M7 group effect on the S&P 500 overall

-

13.75% (1375 b.p basis points) are due to just 7 stocks

-

which is a whooping 67.96% of the 2023 total performance (13.75/20.23)

Let that sink in! And bring the sink if you feel like 😉

Who are the leaders, clear! Who are the 7 laggards?

-

their weight is small in the index, but note that some of the individual % returns are materially negative in 2023: Pfizer, Moderna, Chevron, NextEra Energy, Bristol-Meyers with material drawdowns

👉 now let’s ignore weighting and switch to the S&P 500 unweighted components via the following 2D chart: 2023 % returns & Above 52-Week Low %:

-

Nvidia off the charts the mega outlier after the recent AI driven parabolic run

-

followed by Meta, Royal Caribbean, Carnival, Palo Alto, Pulte Group & Tesla

👉 Complementary: single names in the 11 sectors and 24 industries, size = market cap

-

Which one jumps to you and which one you own or find interesting?

👉 continuing smoothly with the S&P 500 stocks above their 52-week lows & below their 52-week highs as my quick way to see both positive & negative momentum

-

if you see some of your names in one of the extremes, it’s interesting to relate to the other close clusters, peers or market overall and derive insight from there

-

interesting view for momentum traders/investor, and as always outliers in are very interesting

📊 Earnings, Profitability, Flows, Value & Growth

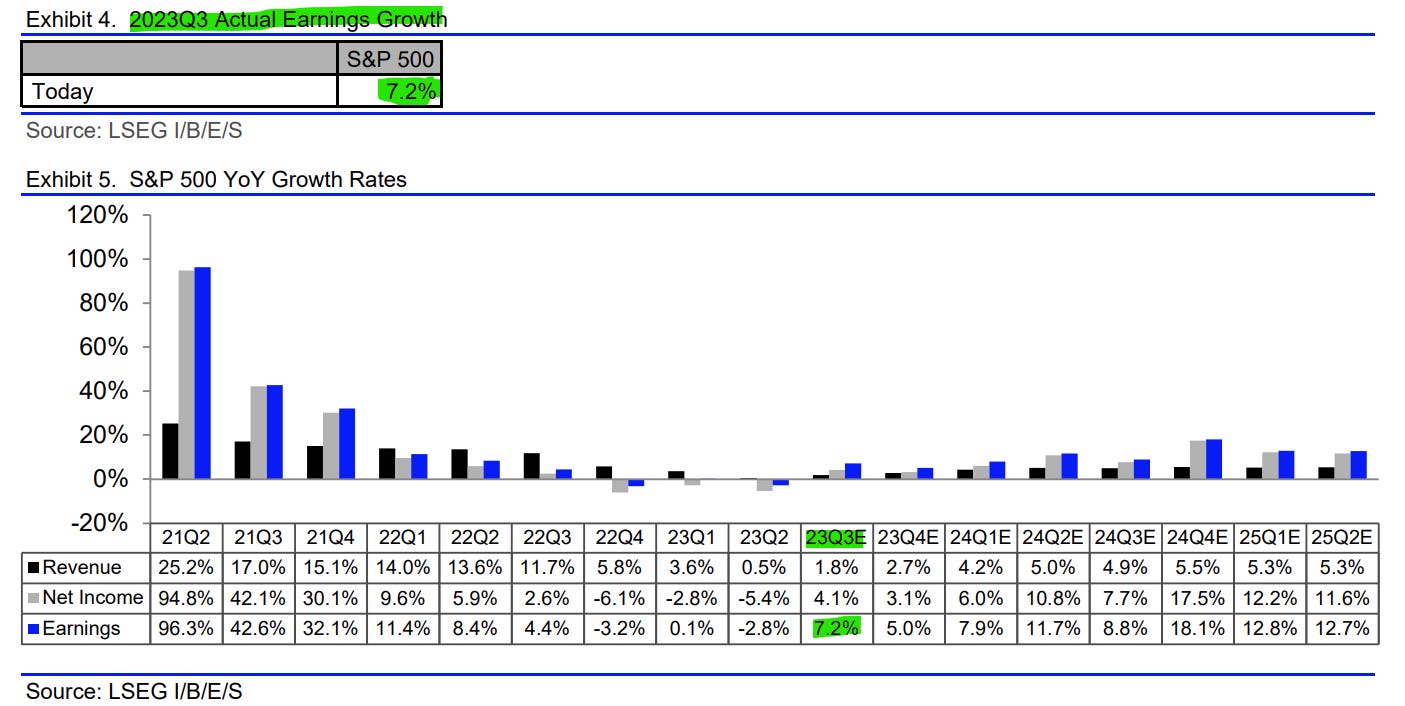

👉 Q3 2023 earnings season

-

Earnings Growth: earnings growth for the S&P 500 is 7.2% and Q3 marks the first quarter of Y-o-Y earnings growth since Q3 2022 (top-line revenue growth at 1.8%)

-

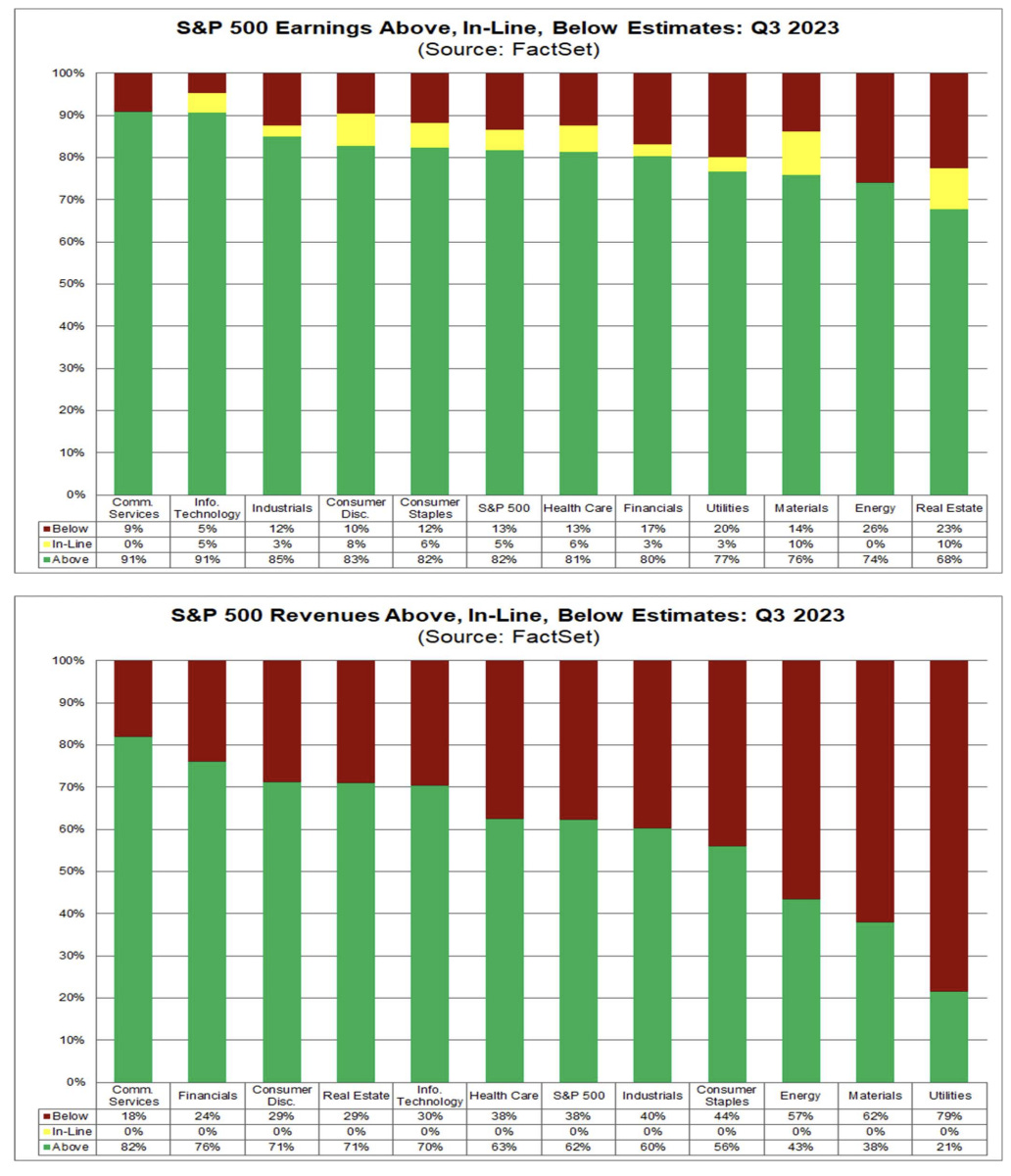

Earnings Guidance: for Q4 2023, 69 S&P 500 companies have issued negative EPS guidance and 38 S&P 500 companies have issued positive EPS guidance

-

Earnings Scorecard: 82% of S&P 500 companies have reported a positive EPS surprise and 62% of S&P 500 companies have reported a positive revenue surprise

👉 Profitability

S&P 500 Profit Margin:

-

stabilizing right around the historical trend line after the big rebound post-pandemic – the very high NPMs I think were possible because the mighty S&P 500 companies have pricing power, hence could squeeze quite some

-

Did the mighty S&P 500 companies cause inflation? No! Now did they take advantage of inflation? Rather yes I would say … thoughts?

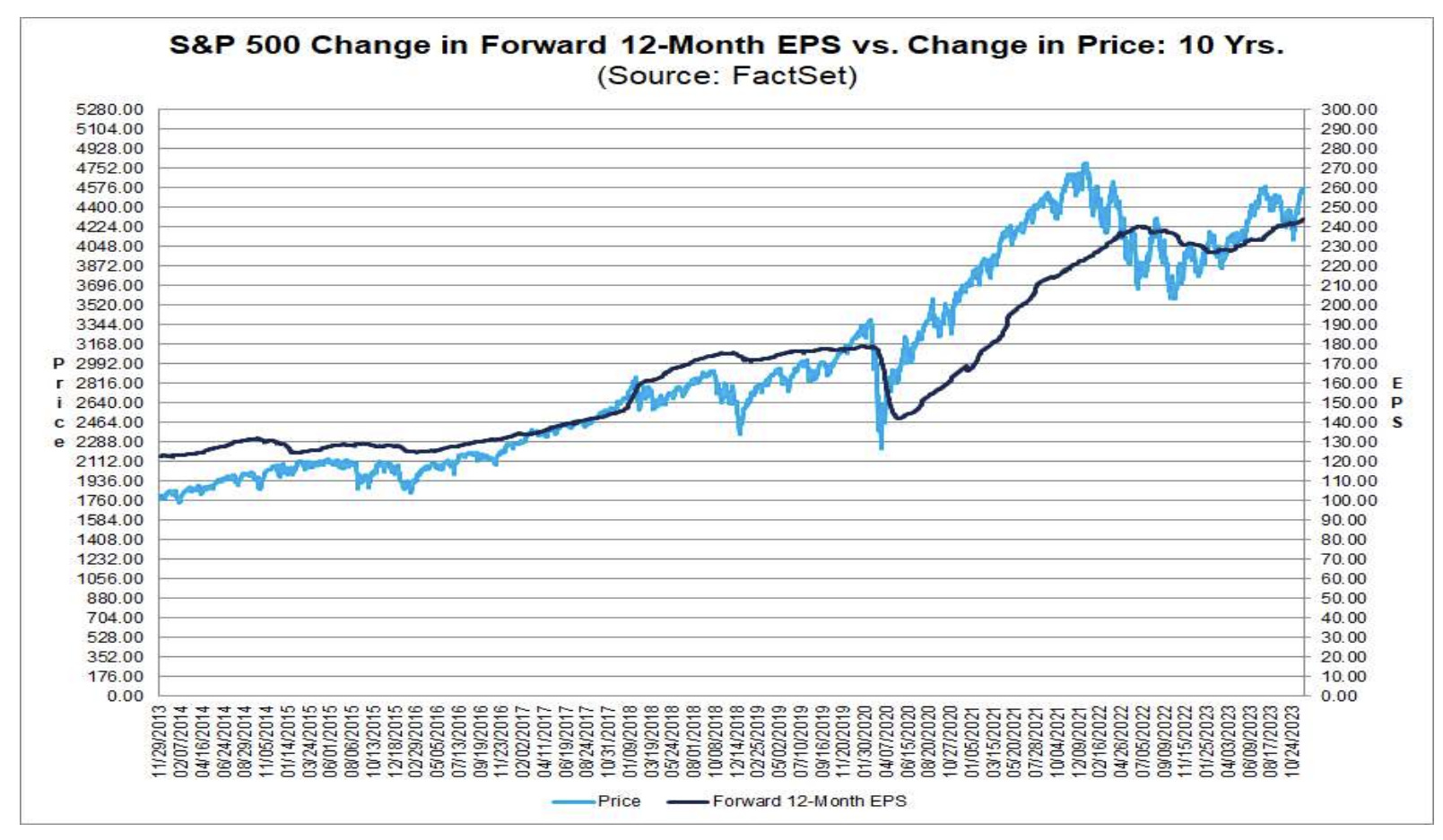

S&P 500 EPS (earnings per share) forward 12-month & price:

-

back to earth & more aligned after the FED (and fiscal policy) induced parabolic run once the Covid outbreak

-

when stock prices go way way above earnings/EPS consider getting cautious …

-

fundamentals matter always sooner or later – in the end of the day, as I heard it on the street, it is all about earnings (not stories, but they do ‘work’ short-term)

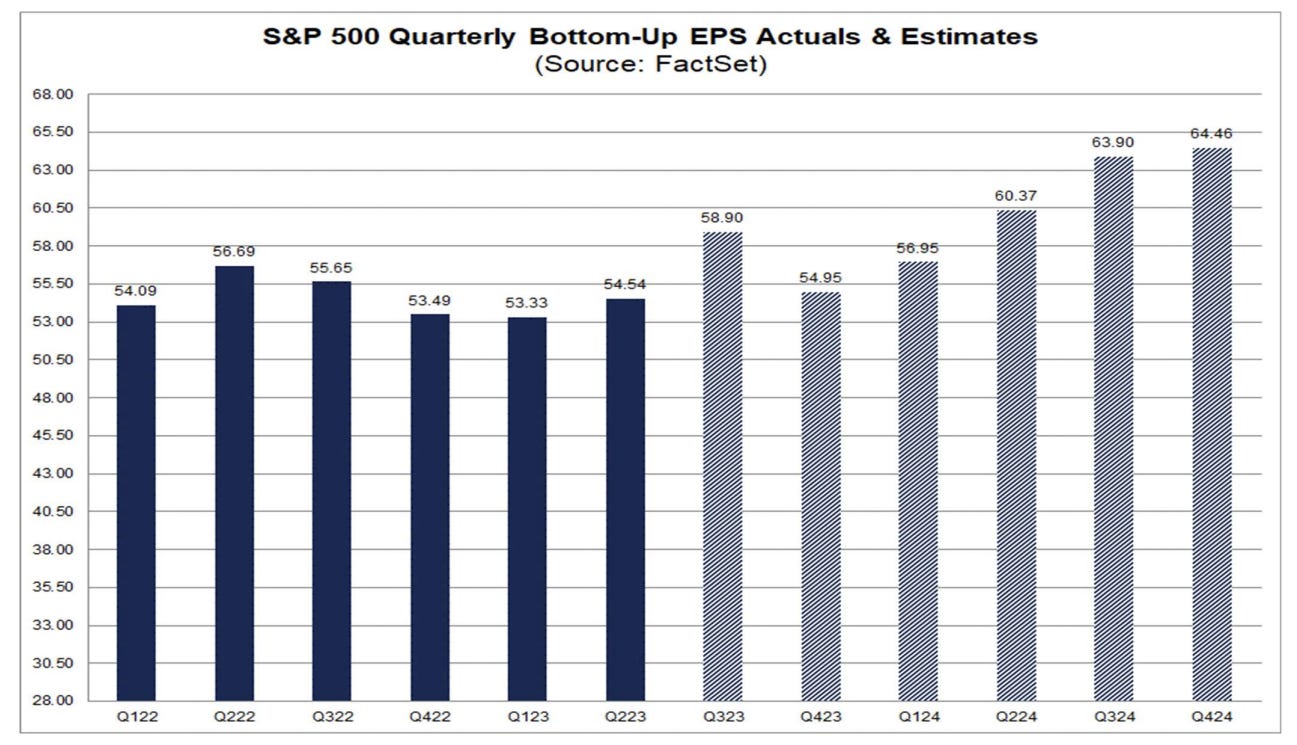

Complementary, the S&P 500 EPS Actuals & Estimates via consensus bottom-up:

-

Quarterly bottom-up: 58.9 for Q3, 54.95 drop for Q4, then pace to pick up

Yearly bottom-up EPS actuals & estimates:

-

221 for 2023 & 246 for 2023. No earnings recession on the horizon …

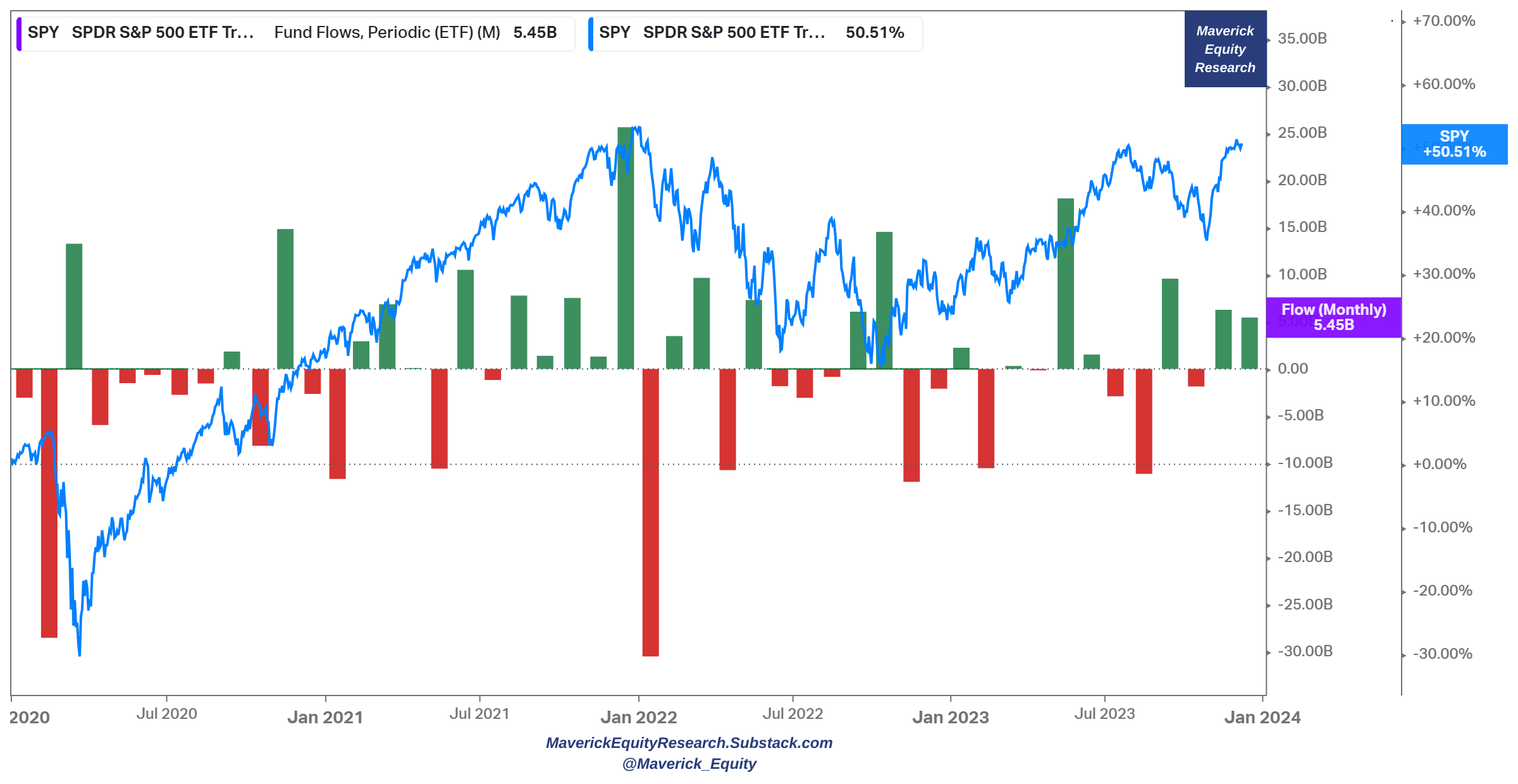

👉 S&P 500 (SPY) monthly financial flows (green/red) & total return (blue) since 2020

-

2020 Covid crash: -$28.5bn in February, +$13.3bn with the March sharp rebound

-

2022 bear market: +$25.6bn in Dec 2021 right at the top, -$30.5bn in Jan 2022 to start the bear market and even bigger than the Covid crash, hence big outflows outliers are a good metric to watch for

Now in 2023:

-

+$18bn in May as this time it was NOT sell in May and go away because they were bigger even than the October 2022 +$14.5bn local bottom which told us there is another leg higher in the 2023 rebound

-

November good with +6.35bn, for December I aim for positive inflows for Christmas mini-rally, but not a strong one, November was a big +month already (one of the strongest November gains on record)

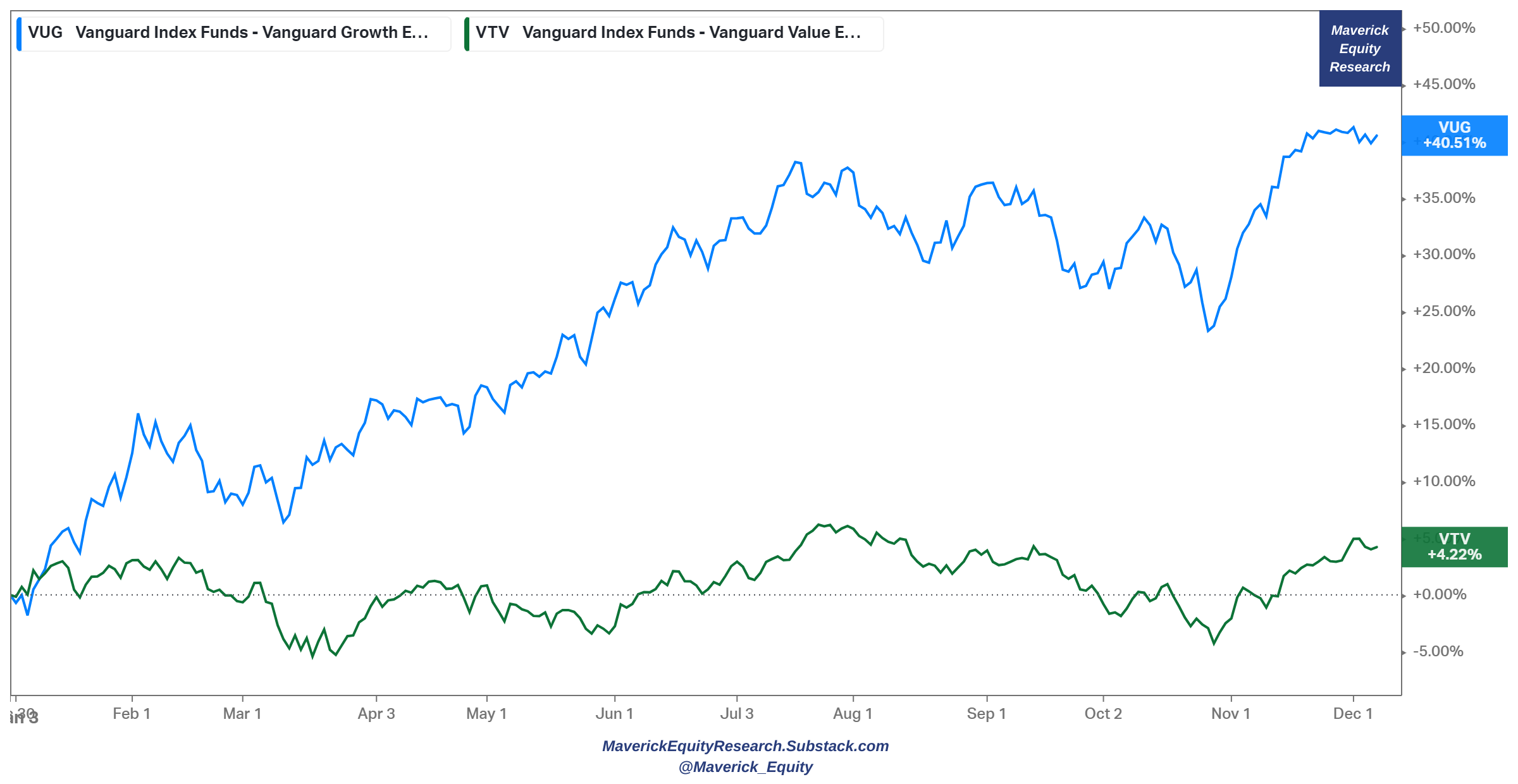

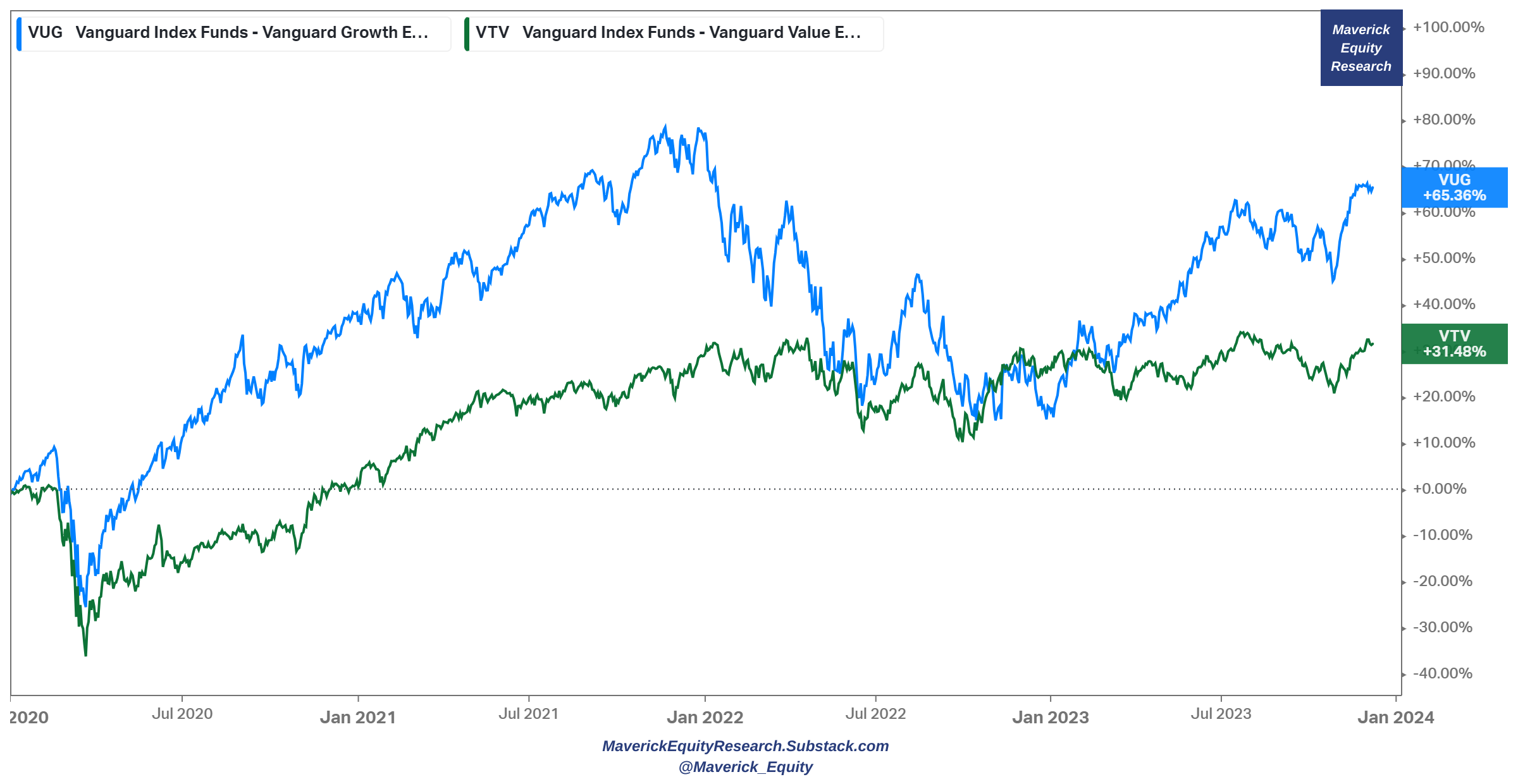

👉 Value & Growth in 2023 for a styles view – growth leading as expected

-

VUG growth (blue) +40.5% rally while VTV value (green) with just +4.2%

-

Since 2020: VTV value (green) did match VTG growth (VUG) for a good part of the 2022 bear market, now Growth is back big via the AI driven run!

Key note now: since 1926, there have been only three decades during which value stocks have underperformed growth stocks: 1930s, 2010s, and 2020 …

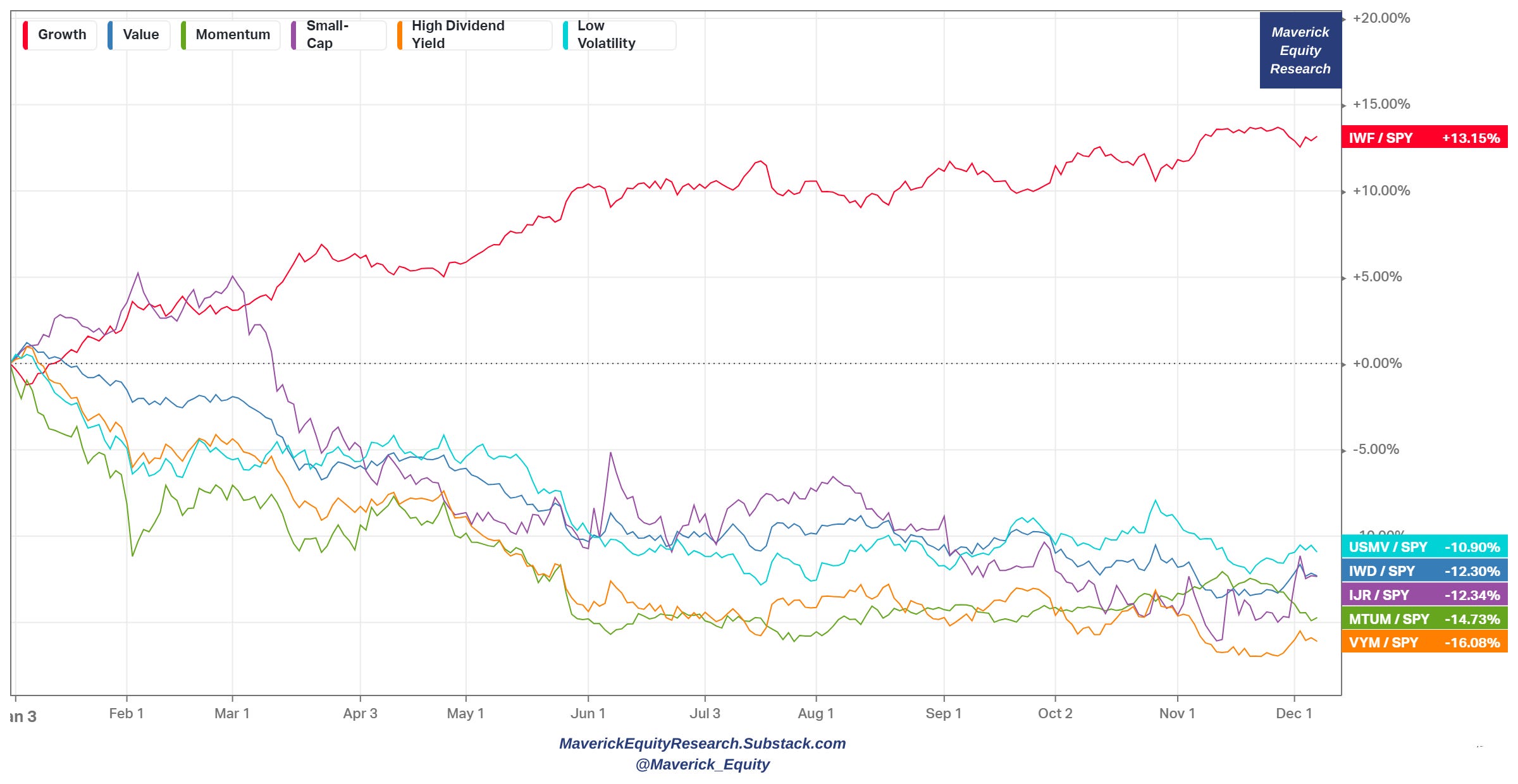

More nuance via factors: growth (IWF) off the charts with the big lead, whereas high dividend yield (VYM) the laggard in 2023

📊 Sentiment & Chatter

👉 Sentiment:

-

Both retail and professional investors believe their personal investments will do better in 2024

-

After the 2022 bear market, retail investor sentiment picking up materially though dipped in November, exactly when a material happened …

-

The Fear & Greed index shows GREED at 64, which is way above the Fear 40 from 1 month ago

-

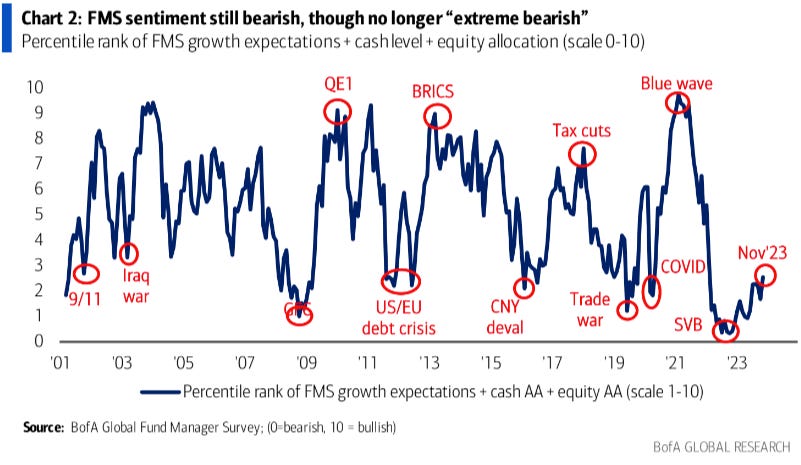

BofAs most broadest measure of Fund Manager Survey sentiment (based on cash positions, equity allocation & economic growth expectations) rose to 2.6 from 1.7 = largest monthly rise since Nov’21

👉 Chatter

AI chatter cooling off … was about time

-

152 companies cited the term “AI” during their Q3 earnings calls

-

this is 16% less when compared to Q2 2023 (180)

The ‘R’ rated chatter: Recession chatter cooling off … was about time after the most anticipated recession ever that we ‘have’ since 2021-2022

Inflation chatter cooling of also … as expected

-

number of inflation discussions trending lower and lower during earnings calls

Inflation & hawkish central banks used to be the biggest ‘tail risk’, though it has dropped materially month after month lately, while replaced now by Geopolitics

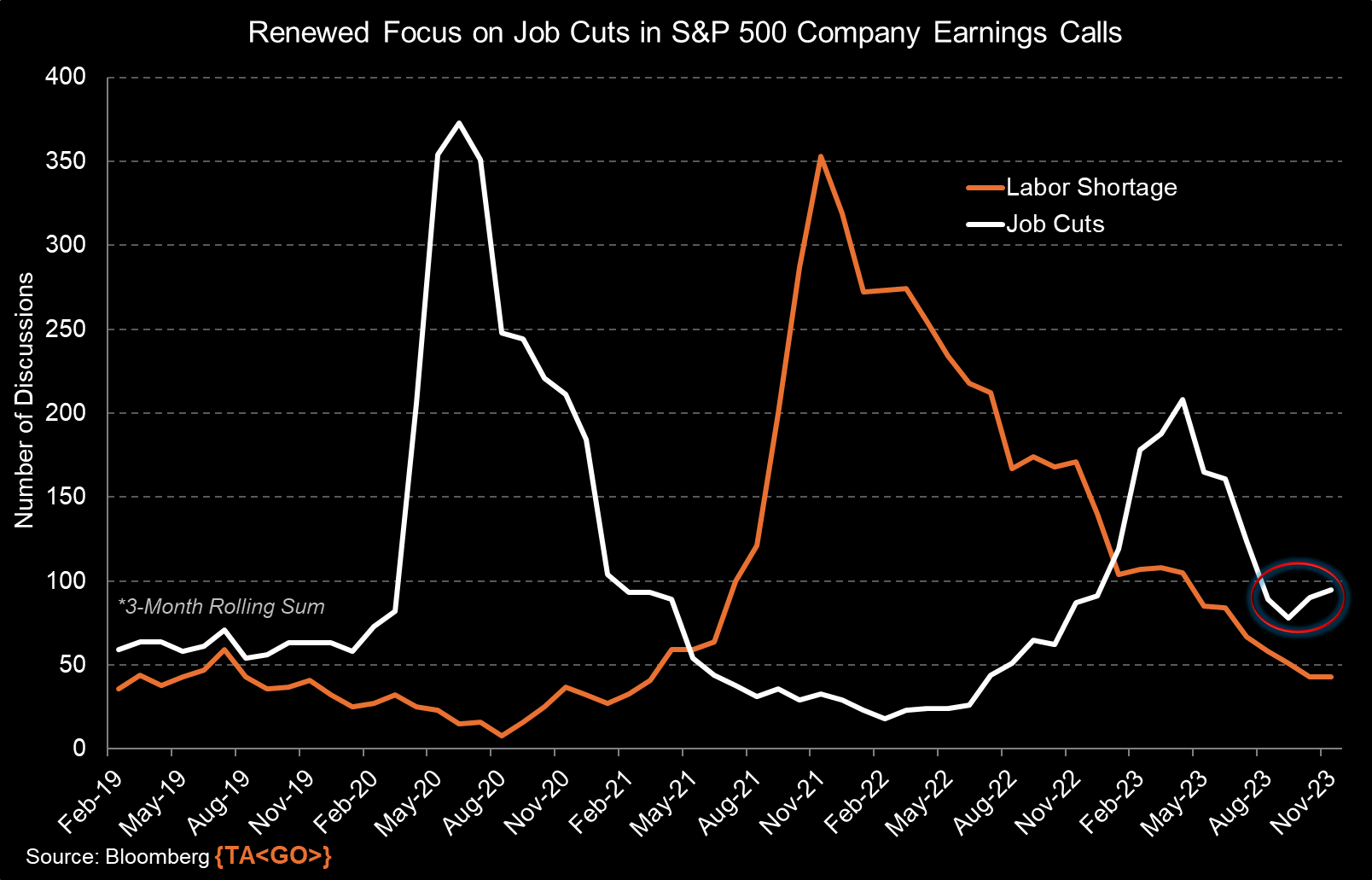

Job Cuts vs Labor Shortages

-

labor shortages less and less of a talking point while note an uptick in job cuts

-

job market normalising after it has been very hot for quite some time

-

sectors wise, Tech and Financials with the most intense job cut chatter

📊 Seasonality, Volatility & Breadth

👉 Seasonality – it’s that time of the year … December Christmas rally

-

S&P 500 has typically outperformed in the 5 days before and after Christmas

-

To hold true in 2023 or did Santa come early this year in the good November?

I expect a positive month, not a big rally … mainly because of the very good November, but guess what? I hope to be wrong 😉

-

Quarterly wise, since 1985 we have a 6.1% return in Q4 which is very good

Personally, I expect less given already a great year, but sure, I hope to be wrong 😉

👉 if you want to look ahead of December, how does January look like?

-

after good/great annual gains (like 2023), January is negative of flat

Overall, a key chart message: we are trading similar to the consolidation phases after the last two big market breaks: dot-com burst of 2000 & 2008 Lehman bankruptcy

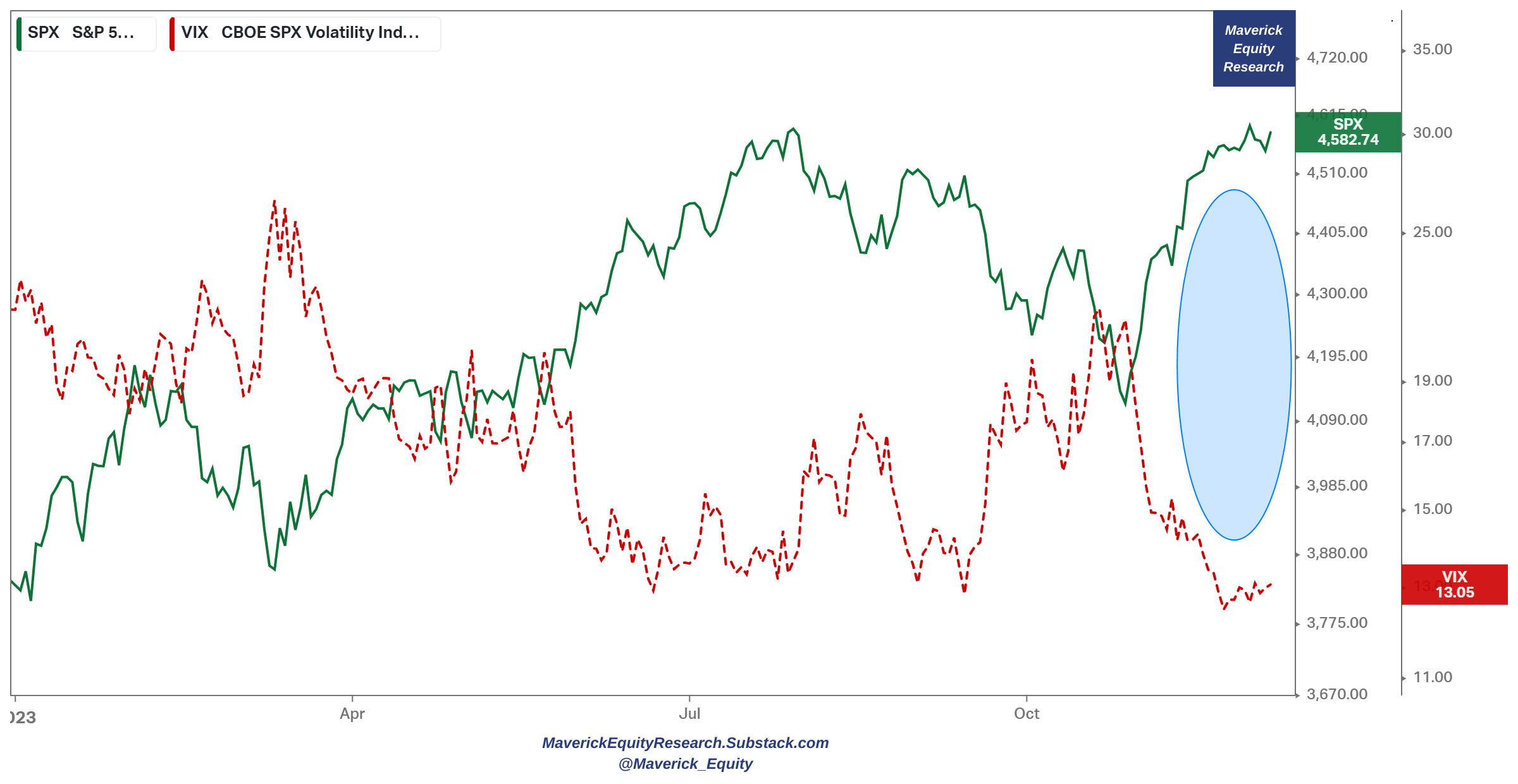

👉 Volatility

-

2023 stock market rally caused VIX (indicator of market uncertainty) to fall in June to its lowest level in more than 3 years (since January 2020)

-

November rebound and very good sentiment caused VIX to go even lower

👉 Breadth

-

breadth is not stinky anymore: % of S&P 500 stocks trading above their 50 day moving average shot up lately

📊 Technical Analysis: Short Term & Long Term

👉 Short Term:

-

trending nicely in an upward channel once we left the 2022 bear market

-

however, the RSI at 69 in oversold conditions as it signalled also before local tops

-

200-day moving average as a support level at 429

👉 Long Term:

-

after the great November, above both 50 & 100-week moving averages which are now support levels going forward, 424 and respectively 415 levels

-

RSI in overbought territory at the 68 level which often signals a move lower

📊 The 11 Sectors Performance Breakdown

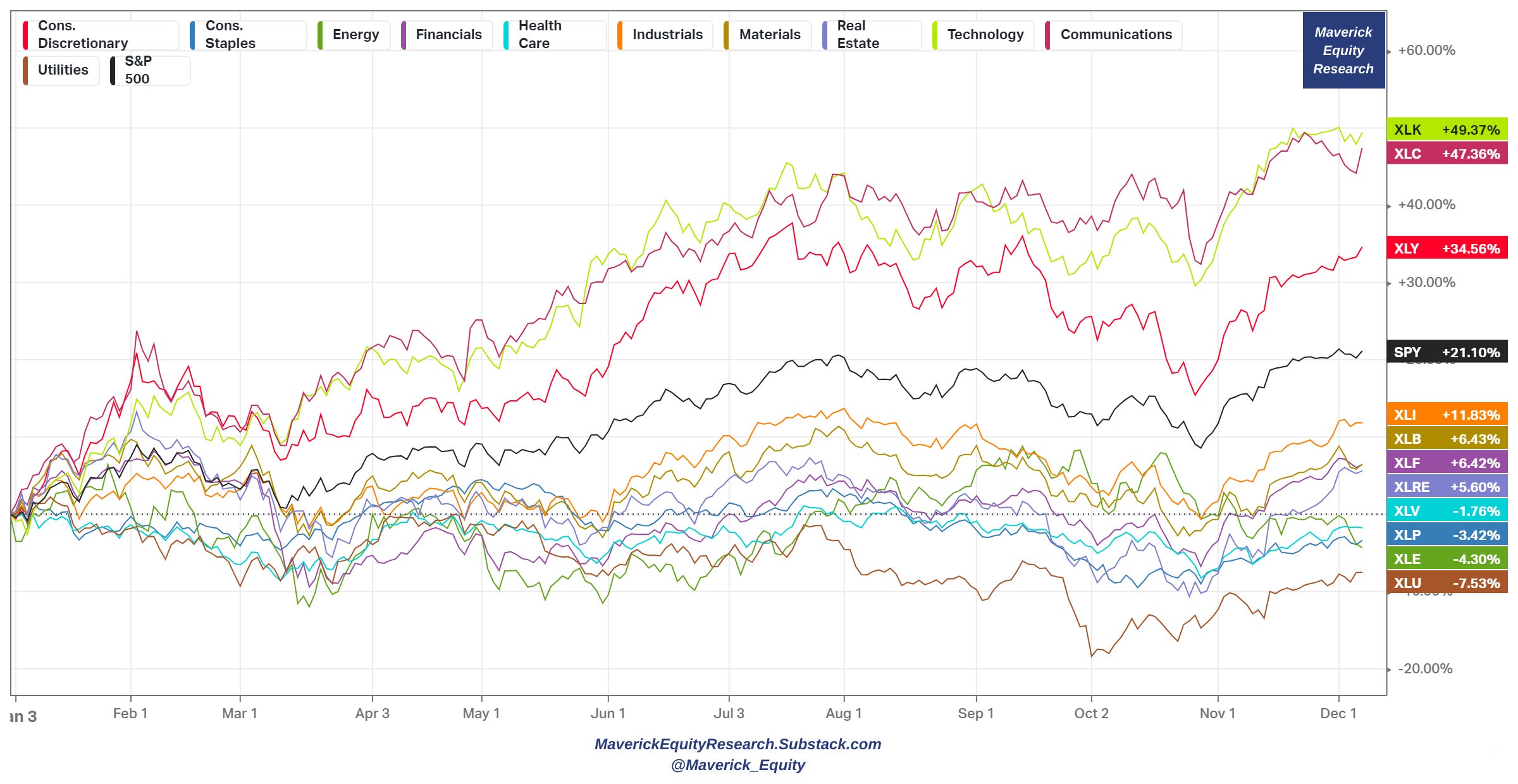

👉 2023 performance of the 11 Sectors that shape the S&P 500:

-

XLX (Tech), XLC (Communications) & XLY (Consumer Discretionary) leading

-

56.8% huge spread between the Top & Bottom sectors which is very rare to see: XLC (Communications) + 49.24% while Utilities (XLU) -7.62%

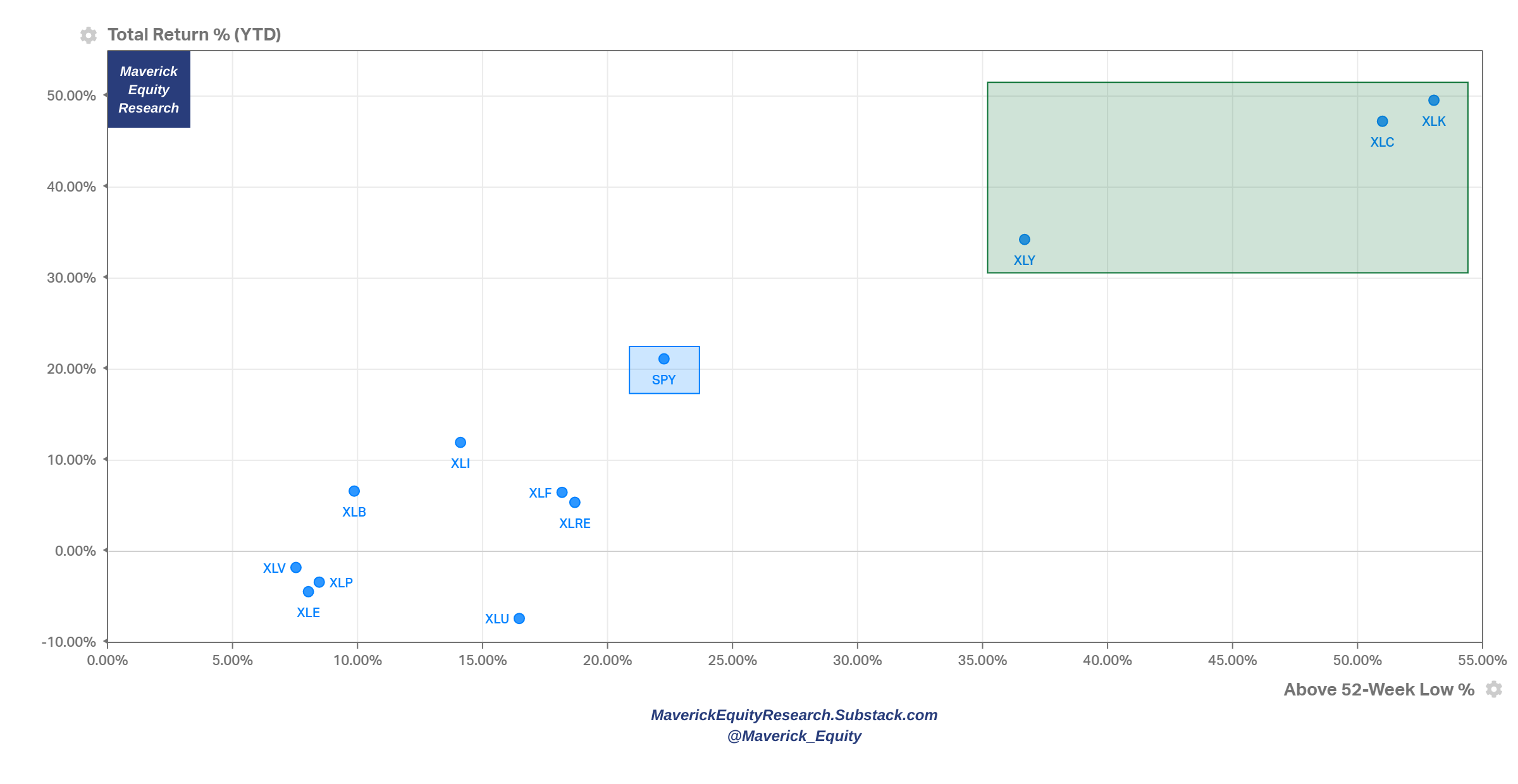

👉 Let’s go 2D: 2023 % returns & Above 52-Week Low % for the 11 Sectors + S&P500

-

XLK, KLC & XLY also with the momentum from their 52-week lows

-

note: Real Estate XLRE and Financials XLF bouncing back from the 52-week lows

👉 Let’s zoom out to check the techie trend – ‘Tech is taking over the world baby!’

Tech relative to S&P 500 – $XLK ETF VS $SPY ETF since 1985:

-

during Covid it broke the +1 standard deviation while in 2023 with the AI run even the +2 SD

-

while tech today is real, works and brings a lot of value (2001 dot-com empty concepts many) … it’s hard to ignore the parabolic run lately

-

and note: I compare it not to some empty/unprofitable/volatile sector, but to the mighty S&P 500 … which is not a shabby construct at all, it’s the 11 sectors of corporate America which also derives 40% of revenues from outside the US … and has performed very well since many many decades … thoughts?

Your feedback? Food for thoughts …

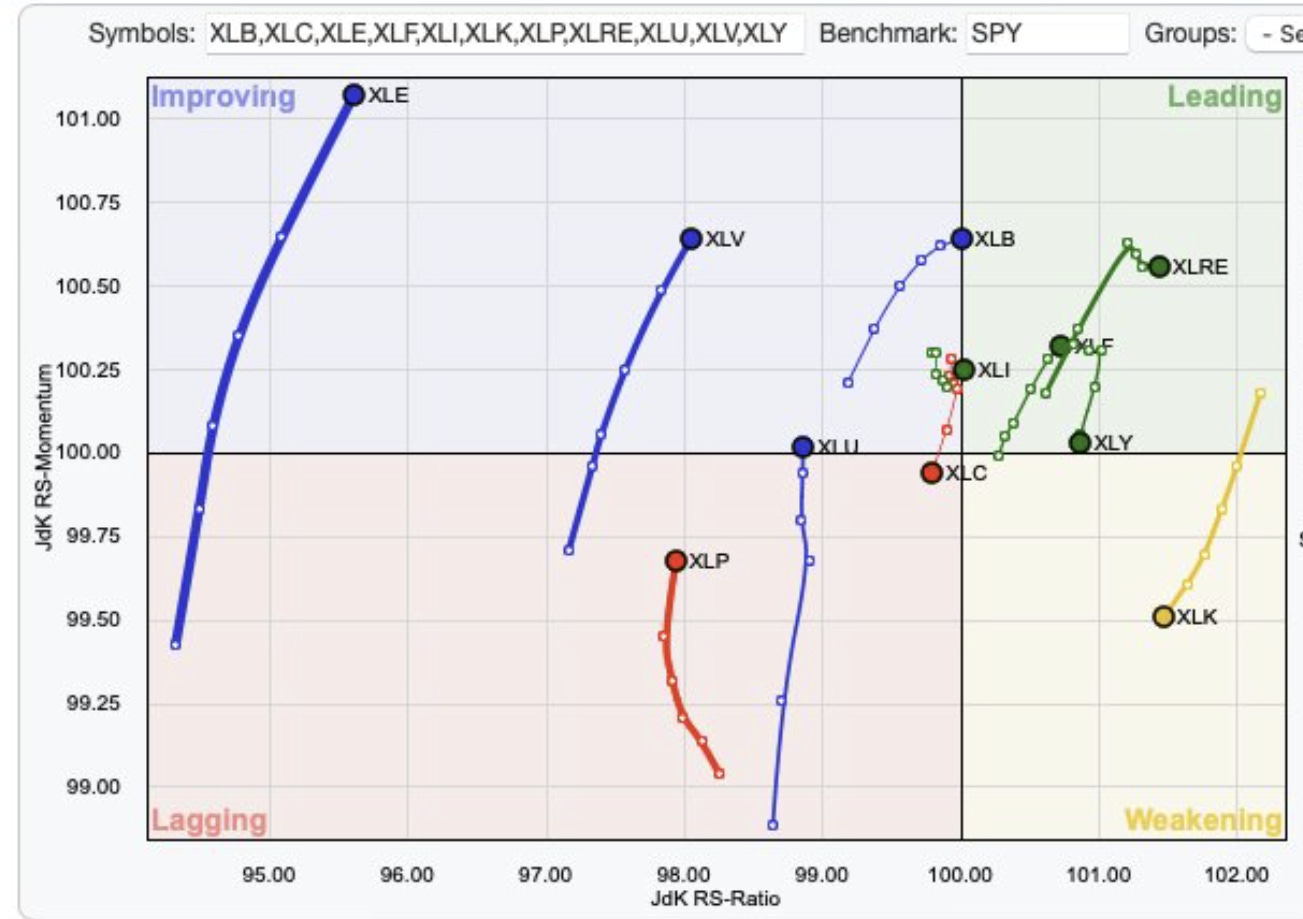

👉 Sectors relative rotation graph, hunting for relative strength & momentum:

-

Leaders: XLRE, XLY, XLF, XLB, XLI

-

Improving: XLE, XLV, XLU

-

Weakening: XLK

-

Laggers: XLP, XLC

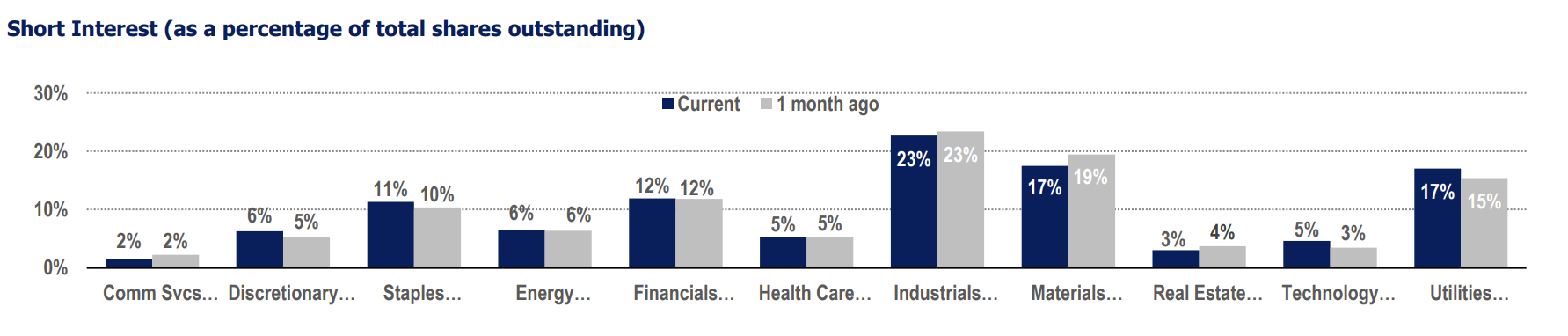

👉 Short Interest breakdown for the 11 sectors: Industrials XLC the most shorted, Tech (XLK), Communication Services (XLC), Real Estate (XLRE) the least

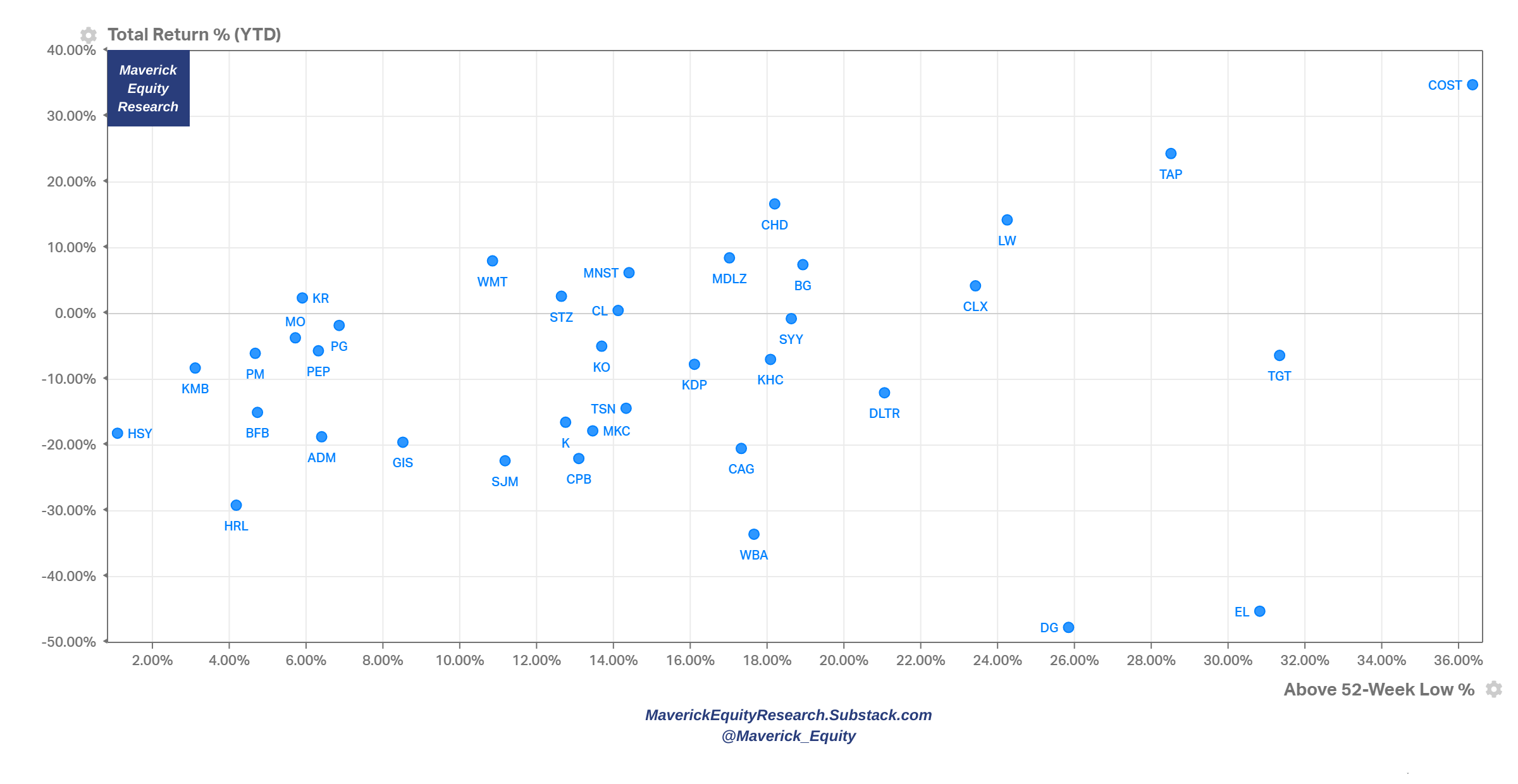

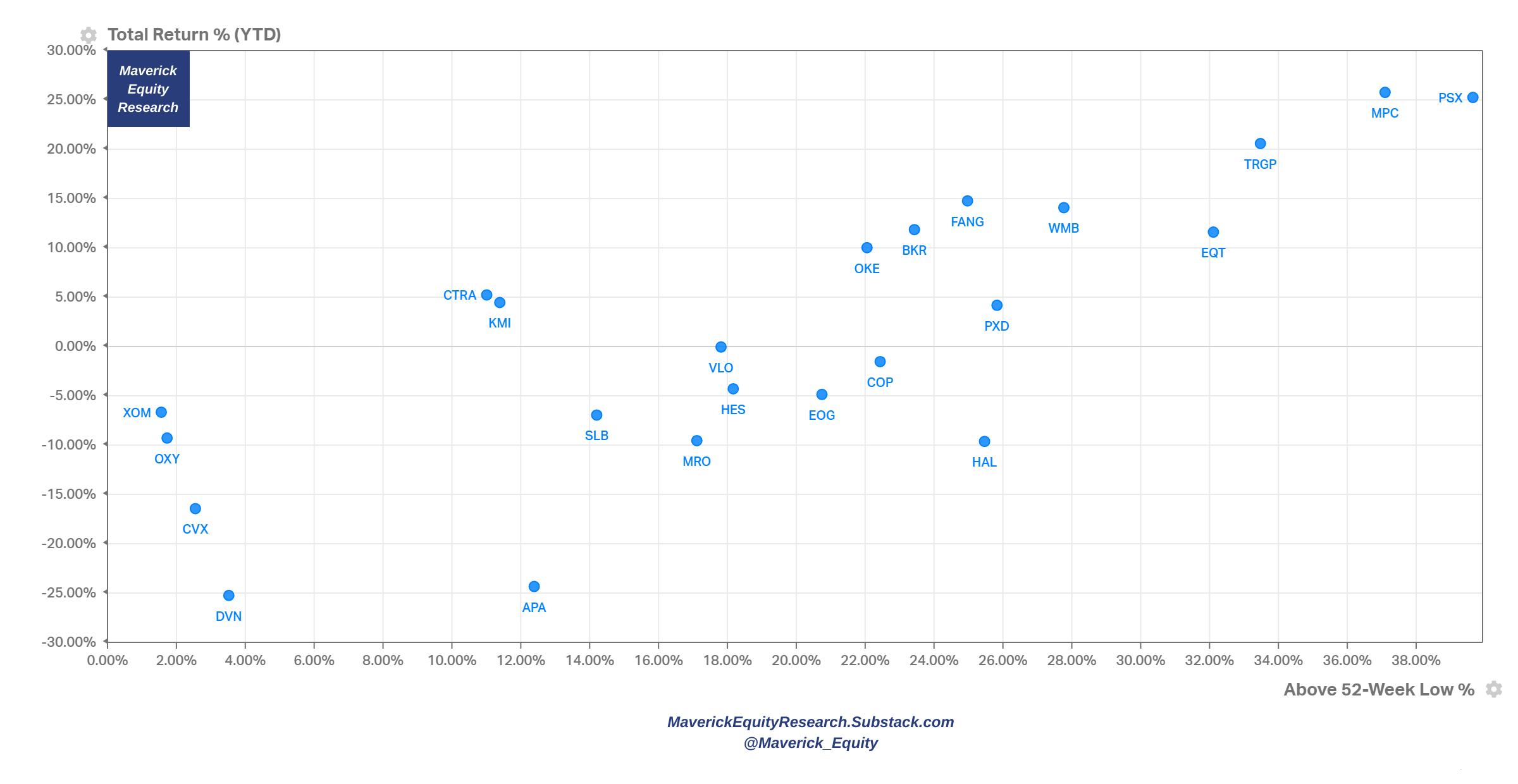

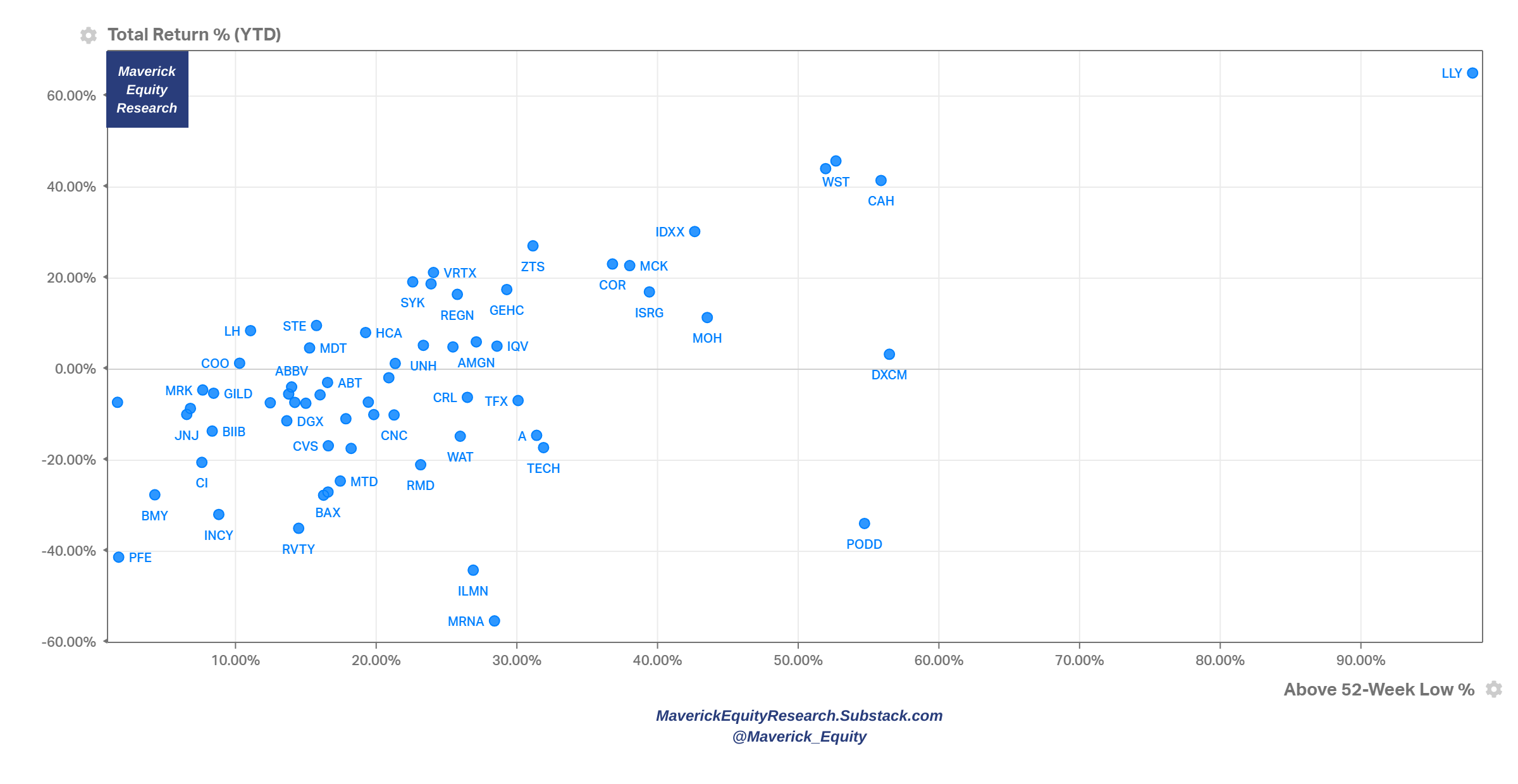

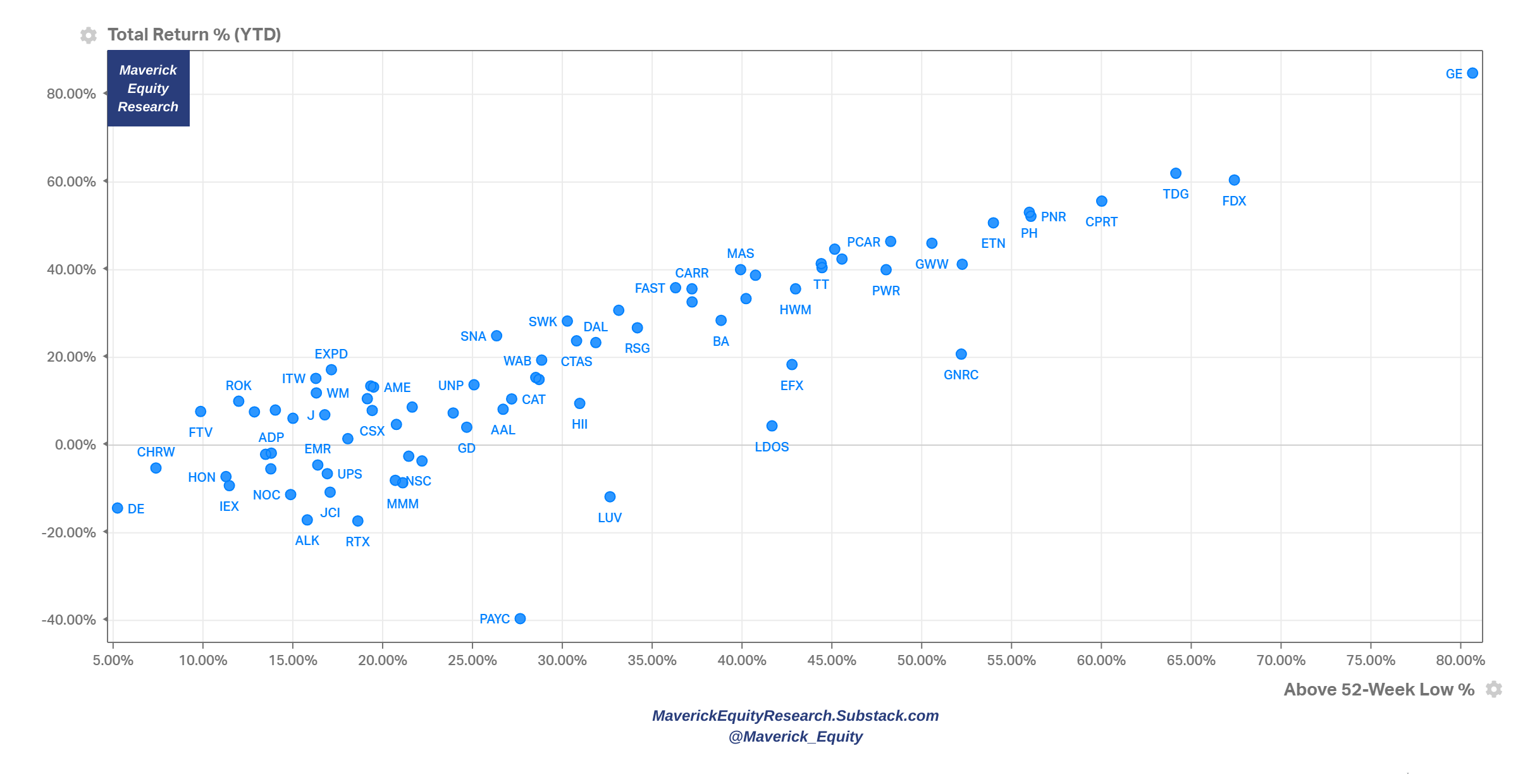

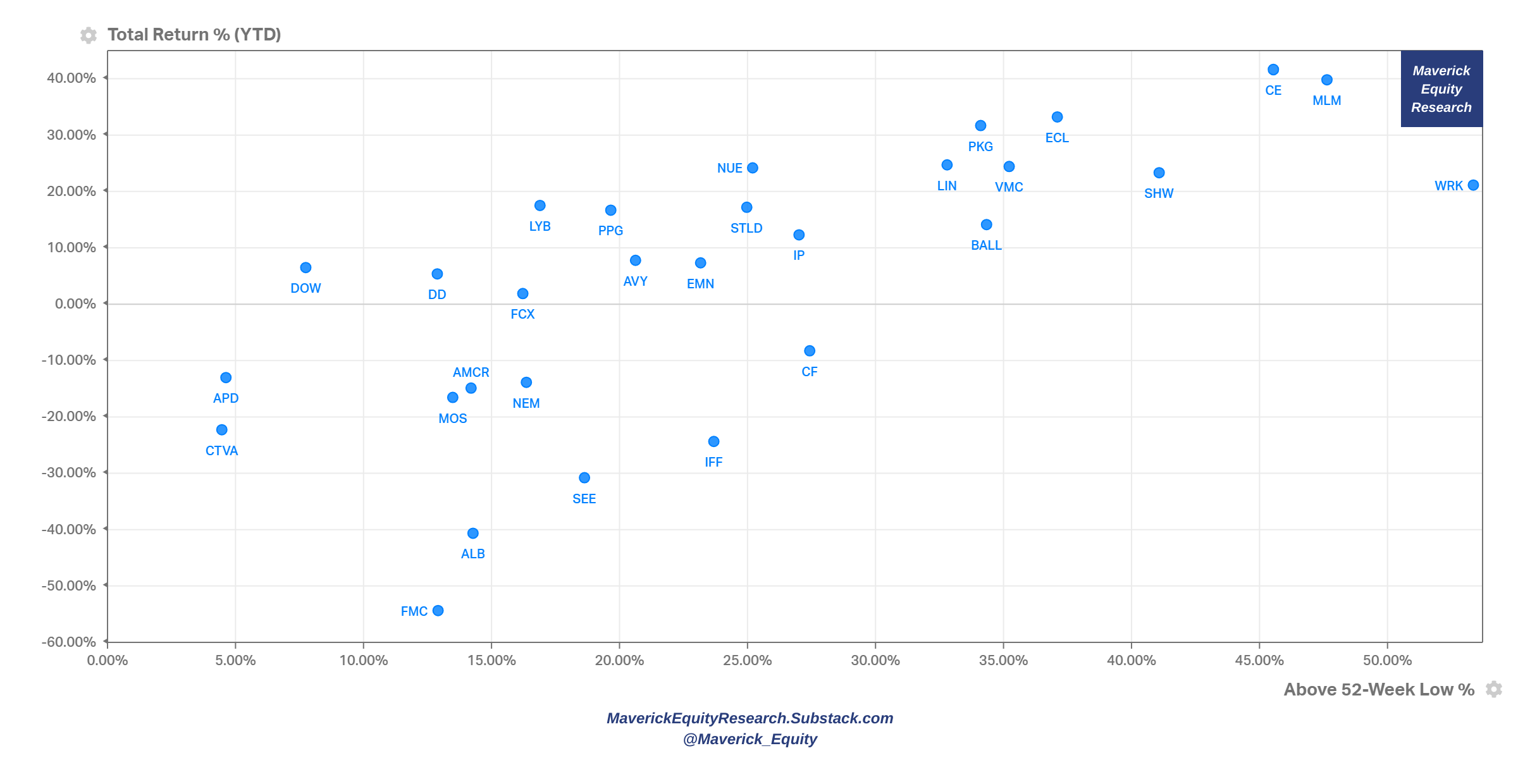

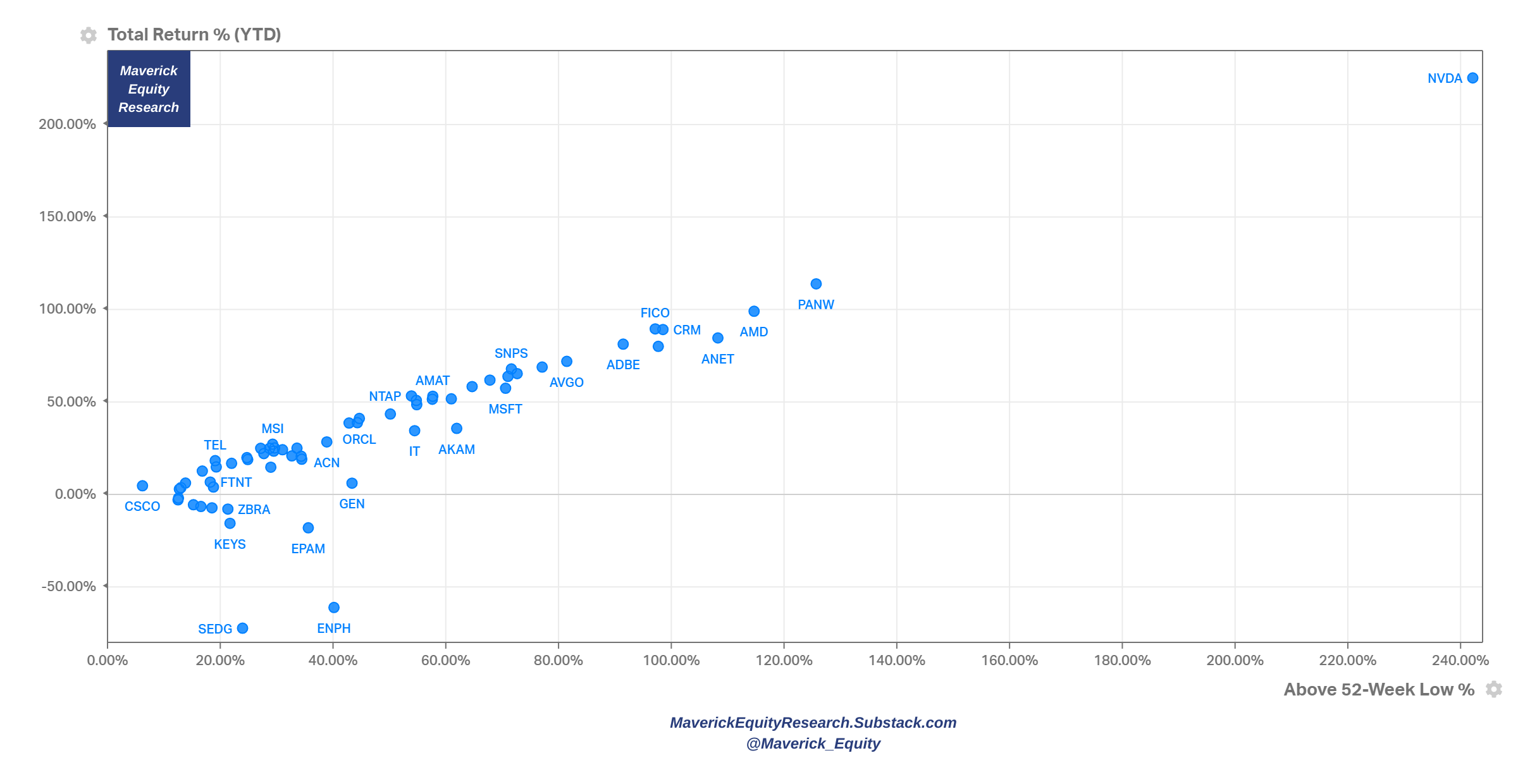

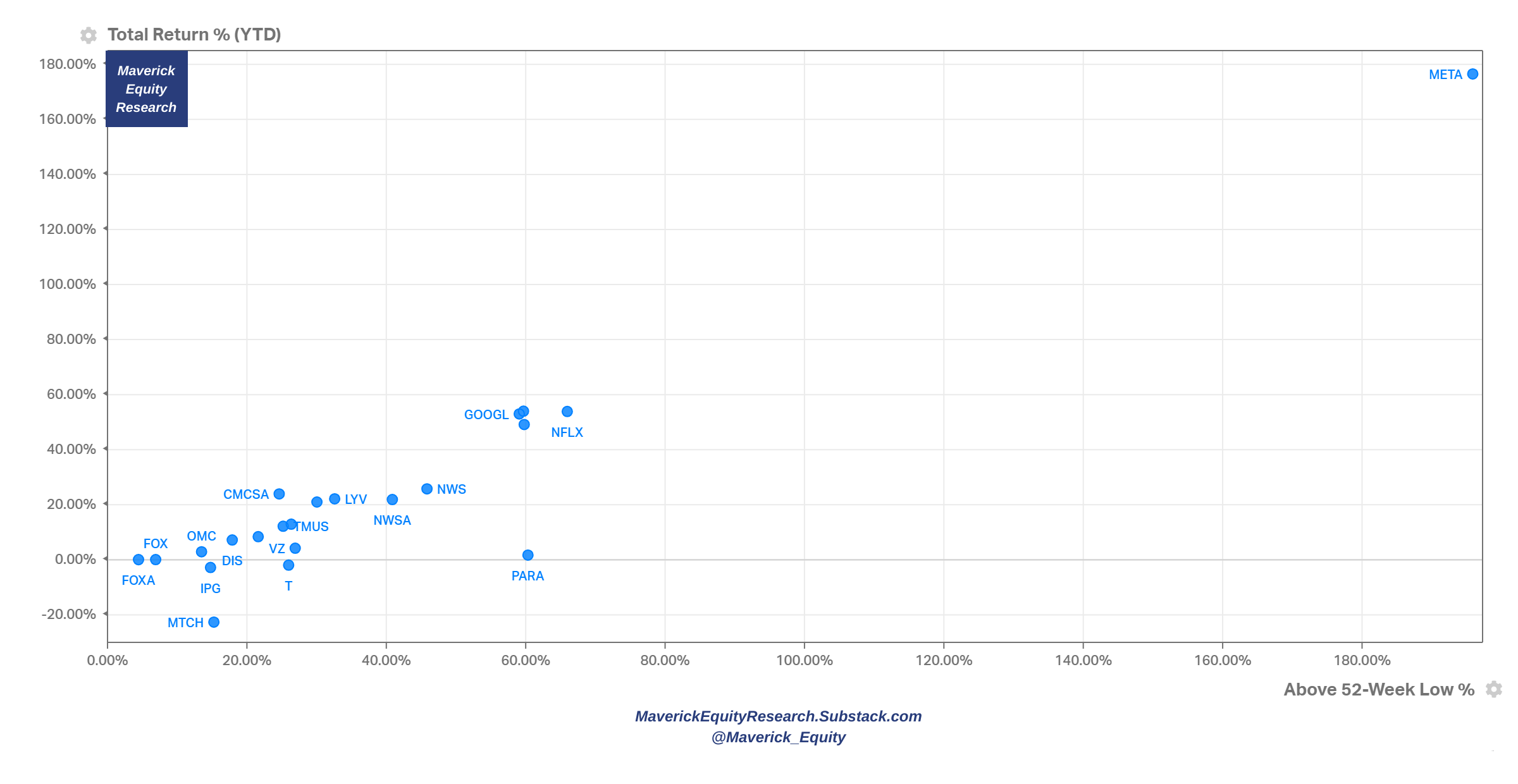

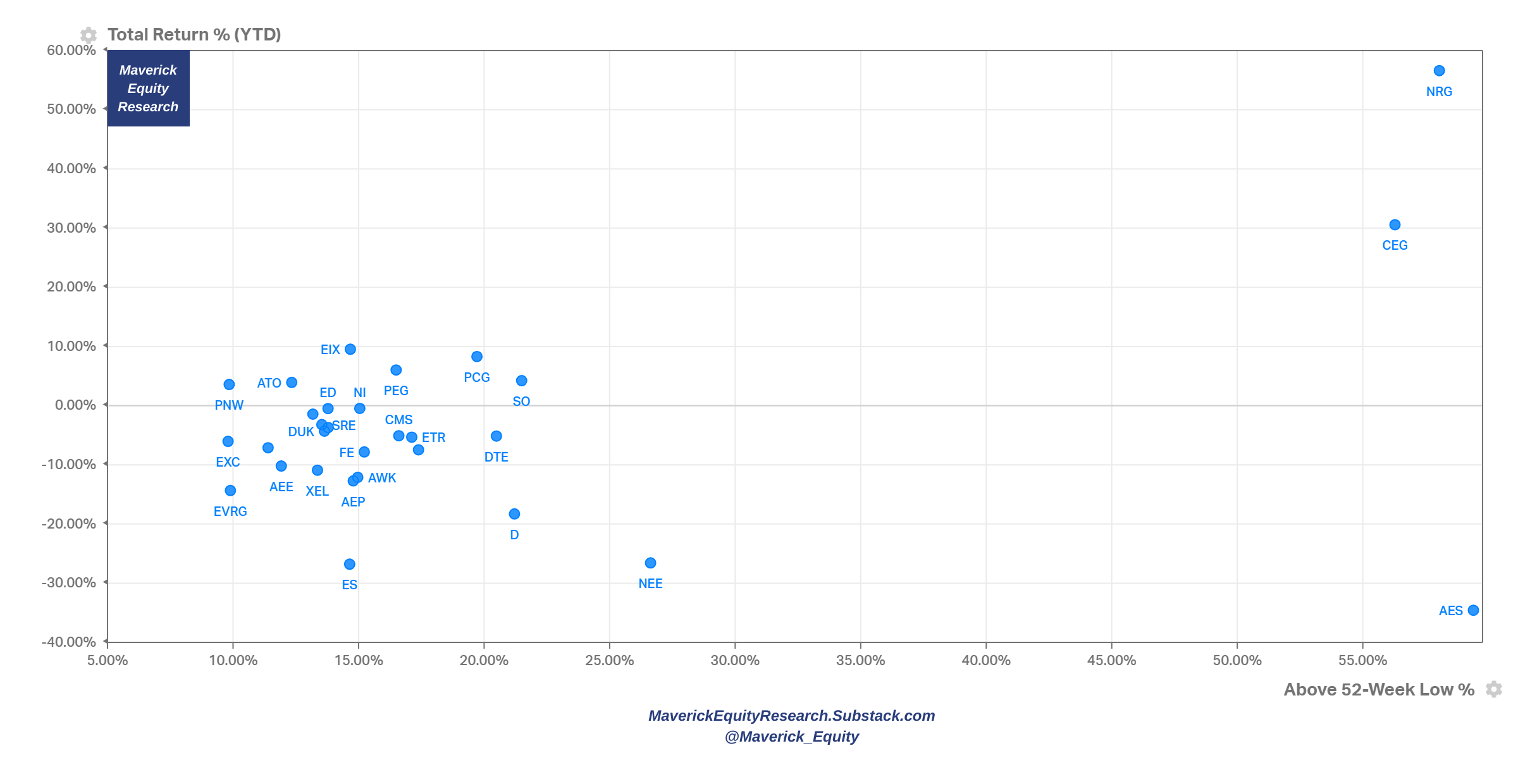

👉And now let’s zoom into the Price/Performance of the 11 sectors via scatterplots: 2023 % returns & above 52-week low % returns. General use cases for this visuals? Check for outliers, market leaders & laggards, positive/negative momentum, relative strength and/or likely un/warranted cheap /expensive stocks:

-

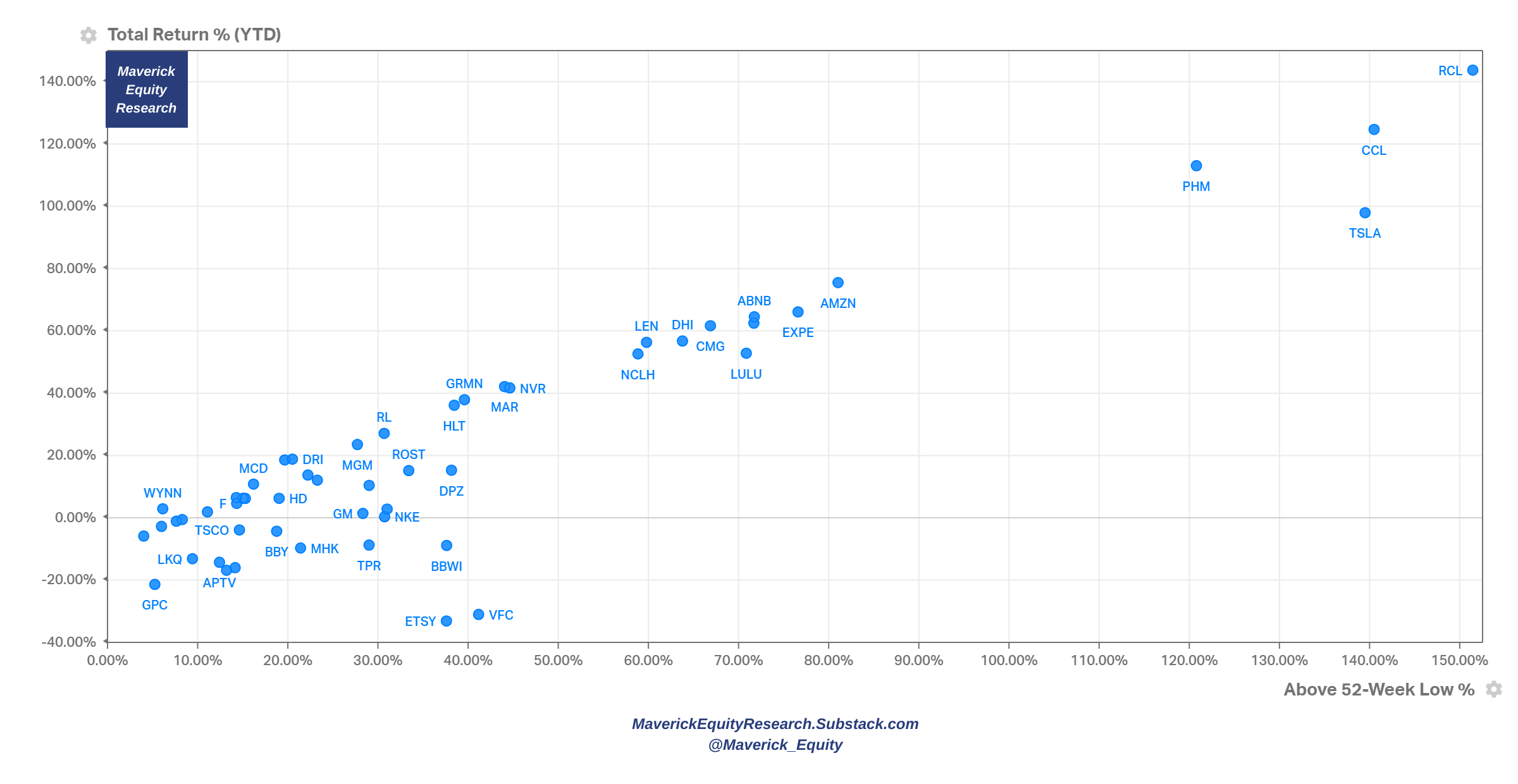

XLY – Consumer Discretionary: Tesla (TSLA) & the cruisers Royal Caribbean (RCL) and Carnival (CCL) rocking the boat …

-

XLP – Consumer Staples: Costco (COST) keeps bringing the goodies, while let’s note also Dollar General’s rebound from the 52-week low after a very rough patch

-

XLE – Energy: Exxon, Oxy and CVX down in 2023 after some great runs, key names to watch for a rebound

-

XLF – Financials: a mixed bag as pretty much most of the times: PayPal (PYPL) continuing the slide in 2023 while ZION with a big rebound from the 52-week low

-

XLV – Health Care: quite some names down this year while Eli Lilly (LLY) the big outlier on the positive side

-

XLI – Industrials: General Electric (GE) and FedEx (FDX) the big leaders, while note John Deere (DE) is down in 2023 (after record gains since 2020)

-

XLB – Basic Materials: quite some names rebounding nicely from the 52-week low … infrastructure needs and demand anyone? … I would say so …

-

XLRE – Real Estate: Digital Realty Trust (DLR) the outlier in this space …

-

XLK – Technology: Nvidia (NVDA) the big outlier, AI AI AI … Cisco, a laggard

-

XLC – Communications: META/Facebook with a mega rebound, currently in the MetaVerse … all that Mark’s training to fight Musk in the ring hlpe it seems 😉 Google (GOOG) & Netflix (NFLX) not chilling anymore with a nice rebound also …

-

XLU – Utilities: NRG Energy (NRG) & Constellation Energy Corporation (CEG) the two positive outliers while most names down in 2023

📊 Special & Alternative Metrics

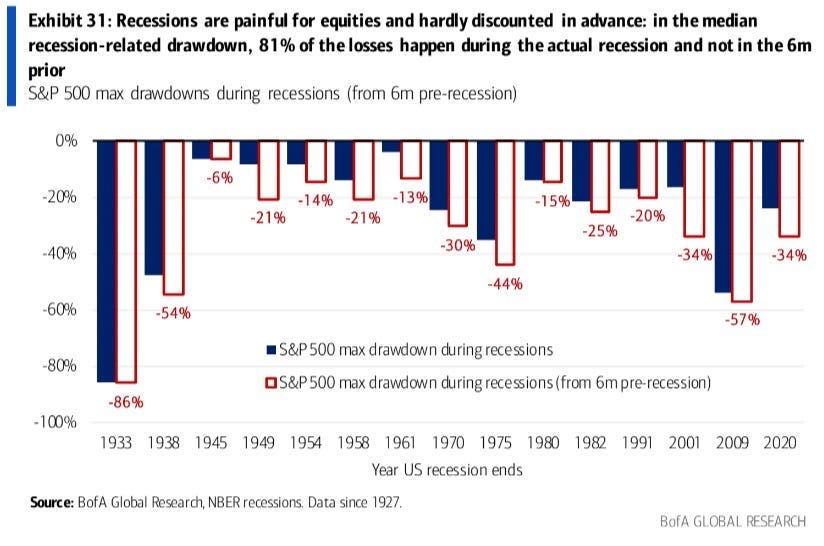

👉 We often hear that the stock market anticipates (by 6 months) & prices in an incoming recession, but that isn’t quite true

-

81% of the drop in value happens during the actual recession & not 6 months prior

-

S&P 500 drawdown during recession (dark blue bars) vs the drawdown including the time period 6-months prior to recession … let that one sink in!

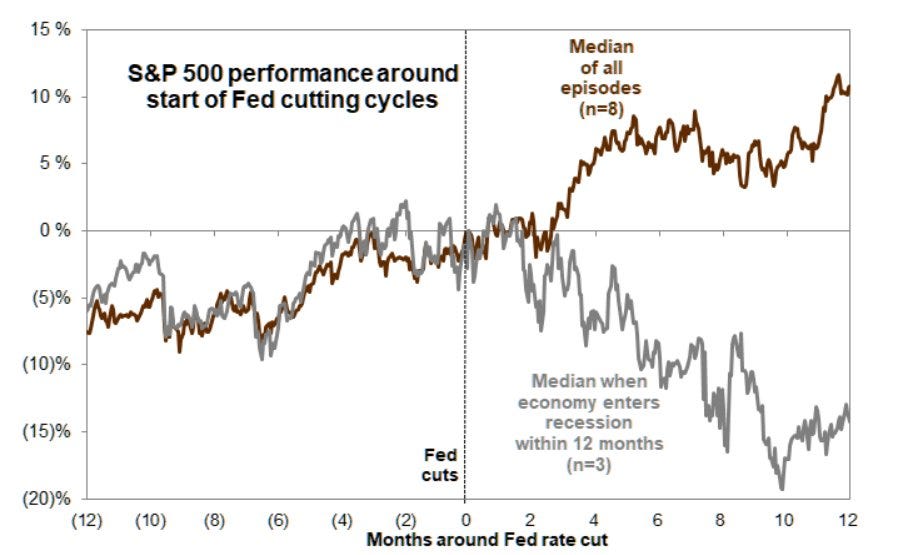

👉 The big chatter in the markets is the scenario in which the FED starts cutting rates which is priced in by the FED funds futures now. Hence, the big key question is: how does the S&P 500 perform around the start of FED cutting cycles?

-

without a recession, actually cuts are beneficial with +11% in 12 months

-

with a recession, a 19% drawdown & -14% 12 months later which is not a biggie

N.B n = 8 and n = 3, not a big sample, but it’s what we have for the last 8 cycles

👉 S&P 500 EPS to be boosted by AI for the next 20 years by +0.5% in annual growth driven by widespread AI adoption (0.5% seems not a lot, but CAGR aka compounded)

👉 S&P 500 set to triple to 14,000 by 2034 via the generational cycles:

-

current 16-18 year cycle likely to peak around 2023

-

3x might sound ridiculously high? It is highish but not crazy and that is because: a) reaching 14,000 would imply around 11% annualised returns which is not that uncommon b) not too long ago in 2010 the S&P 500 was at 1,000

👉 How is the S&P 500 dealing with the high & fast rising rates environment?

-

debt service burden is extremely light

-

strong Corporate America is also a reason for why the most anticipated recession did not happen

Complementary angle to answer, ‘how comes rates are not impacting S&P 500?’

-

almost half of the S&P 500 is set to mature AFTER 2030

-

hence, rate hikes have had not much of an impact on their interest expense so far

-

also, many of the S&P 500 companies have big pricing power etc

👉 The Power of Dividends in the S&P 500:

Dividends contributed almost 30% to the 10.4% annual total returns of the S&P 500 over the long run. Some further key notes:

-

In the 1970s, a decade characterized by high inflation and weak economic growth, dividends made up 70% of total returns

-

The 1990s—the decade of the dot-com bubble—had the lowest contribution from dividends of just 15%

-

The 2000s was the only decade with negative total returns: the dividend returns of nearly 2% provided a cushion to offset negative price returns driven by the bursting of the dot-com bubble and the Global Financial Crisis

👍 Bonus Charts 👍

👉 Share of the 11 S&P 500 sectors and their capitalisation shifting over time …

-

utilities and real estate with just 2% while tech with 27%

Now contrast that with the Net Income contribution of each sector

-

tech 27% with 18%

-

energy 5% with 11%

-

financials 13% with 22%

Your thoughts on the historical evolution and nowadays situation?

Research is NOT behind a paywall and NO pesky ads here unlike most other places!

What would be appreciated? JUST sharing it around with like-minded people and hitting the ❤️ button. This will boost bringing in more and more independent investment research … from an independent guy with a laptop & sometimes 2 screens, usually writing from a library, home or while commuting via a train in Europe.

Looking forward for your feedback, questions & thoughts … Thank you!

Have a great December!

Mav 👋 🤝