How Nvidia & Apple can be the Global, US Open Source AI Champions vs China. AI-RTZ #1089

The Bigger Picture, Sunday, May 17, 2026

I’ve written many times in these AI-RTZ pages on open source Large Language Model LLM AIs vs closed-source. All in these early days of the AI Tech Wave. (see links in appendix below).

Over decades, and multiple major tech waves, open source software and hardware have delivered massive operating and financial efficiencies to businesses and users globally, that can be documented in the hundreds of billions. Open source software today provides the under pinnings of over 75%+ of the software used by us all for decades. Be it as consumers, businesses and governments globally.

Despite the on-going arguments against open source by companies that benefit from the closed-source variety. Often couched these days, on geopolitical and national security grounds as it applies to AI.

My professional experience at Goldman Sachs (GS) since 1982, around technology industry and company analysis, has taught me how open source can add value beyond closed source software and hardware. I’ve seen it first-hand since the PC Era in the 1980s. And followed its history post GS and its ensuing benefits. As I’ll outline here briefly today.

I had a front-row seat at the original commercial validation of open source software as a business model. In August 1999, Goldman Sachs took Red Hat public on NASDAQ at $14 a share. It closed the first day at $52. I was the Firm’s co-lead research analyst on that IPO, having founded the Goldman Sachs Internet Research group five years earlier.

Twenty years later, when IBM bought Red Hat for $34 billion — the largest software acquisition in history at the time — Goldman was on the IBM side of that deal. Goldman bracketed both ends of Red Hat’s 20-year public-market journey.

I bring up that arc because history is rhyming on open source at the AI tier — and the question of who carries the AI open-source banner forward for the US over the next five years has a potentially different answer than most observers may currently think. Especially as the world is focused on China currently leading open source AI vs the US.

Current AI market leader Anthropic is currently aggressively lobbying for the US to curtail China AI advances. Unsaid is an effort to slow down open source AI models globally.

In my view, the US open source AI opportunity going forward, lies with Nvidia and Apple. Driven particularly by their unique, foundational presence at the silicon chip and hardware levels.

Both are the relatively under-appreciated open-source AI champions in the US for structural reasons I’ll lay out below.

And both arrive at the moment when the Mag 7 companies that originally built the open-source playbook — Google, Meta, Microsoft, even the company literally named “OpenAI“, along with its sibling rival Anthropic— have all pivoted toward closed strategies at the frontier of AI. Even Elon Musk is steering towards a closed Grok/xAI LLMs, after promising an open source direction for years.

That is the ‘Bigger Picture‘ I’d like to discuss this Sunday. Today’s piece is a bit longer than usual, and has more analysis than my usual posts. I let my inner analyst out this weekend to make my case here. There are even some tables to provide more data and context for the narratives ahead.

Open source as a corporate strategy, not a development methodology

Most outside observers still treat open source as a development methodology — code on GitHub, MIT licenses, Linux distributions. The reality at this point in the AI Tech Wave is that open source is also a corporate-strategy weapon, and has been for at least fifteen years.

A handful of companies have used it deliberately to neutralize a stronger competitor, commoditize an expensive input, or align an industry around a shared standard no single vendor controls. Most plays are defensive at heart. The offensive payoff arrives later, often as a byproduct.

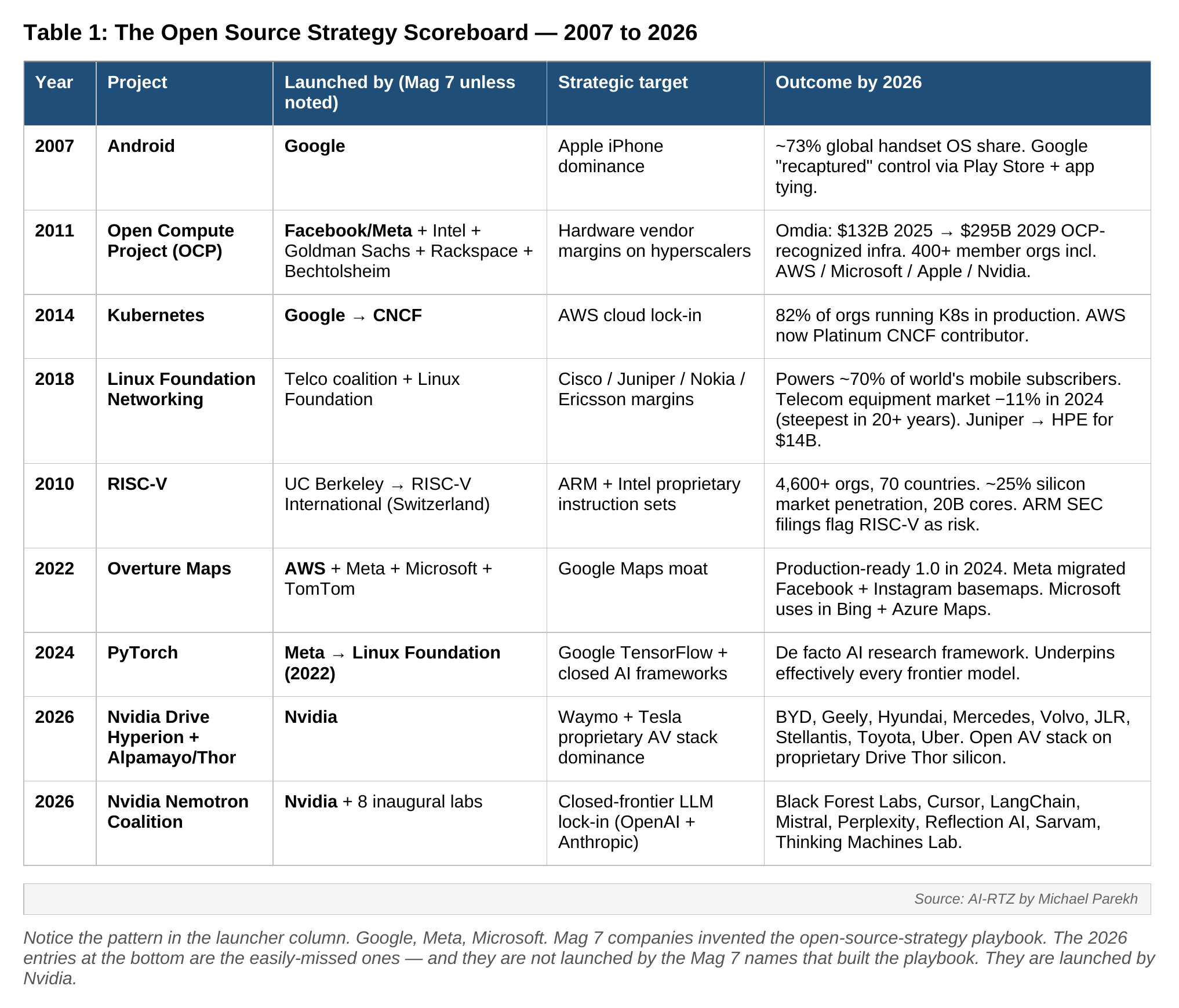

The scoreboard so far is dominated by the Mag 7 companies that have now mostly moved on from using open source in their strategic favor in past technology waves. The table below summarizes the wins to date — it’s not comprehensive, but highlights the big ones.

Table 1: The Open Source Strategy Scoreboard — 2007 to 2026

Notice the pattern in the third launcher column. Google, Meta, Microsoft. Mag 7 companies invented the open-source-strategy playbook. The 2026 entries at the bottom are the easily-missed ones — and they are not launched by the Mag 7 names that built the playbook. They are launched by Nvidia. The company that earned its ‘Mag 7’ status only the last three years of its 33-year overnight success story.

The ironic pivots: yesterday’s open champions going closed at the AI frontier

Here is the story easily missed in 2026: three of the most successful open-source champions in Mag 7 history have pivoted toward closed strategies at the frontier of AI.

Meta was the original convener of the Open Compute Project in 2011 and the company that gave the world PyTorch — the framework that now underpins almost every AI lab’s training stack. For four years (2023-2024), Mark Zuckerberg positioned Meta as “the lone, BIG champion of open-source LLMs” via Llama, as I covered in RTZ #619. By July 2025, Zuckerberg confirmed Meta would not release superintelligence-capable models openly. Llama 4 Behemoth — the planned frontier model — was shelved. Muse Spark (April 2026), Meta Superintelligence Labs’ first frontier-class model, shipped with weights withheld.

Google ran the single most successful Open Source Strategy in corporate history with Android (2007) on smartphones, as a defensive move against Apple’s iPhone. And the second-most successful one with Kubernetes (2014). Today, Gemini at the frontier remains closed. Gemma — in Google’s open-weight family — is committed only at the “nano size.” The same company that wrote the open-source playbook twice and benefited from them, is currently running the closed-source playbook on its most strategic AI asset, Google Gemini AI.

Also ironically, Microsoft, the original “embrace, extend, extinguish” Bill Gates-led foe of open source from the 1990s, became one of the largest enterprise patrons of open source over the last decade — buying GitHub for $7.5B in 2018, joining the Linux Foundation, shipping WSL, contributing to PyTorch. Today its frontier-AI bet is OpenAI (closed), Microsoft Inception (a >$1B LLM acquisition target per May 2026 reporting, presumably closed), and a closed Microsoft 365 AI distribution layer. Phi (3.8B parameters), is the only meaningful Microsoft open-weight model — at the Small Language Model (SLM) tier, not the frontier.

OpenAI is the most surprising name on the list, given the name. Sam Altman publicly conceded in February 2025 that OpenAI had been “on the wrong side of history“ on open source. There have been open-weight releases since, and further openness directed at the China developer market. That frontier stays closed for now. Especially going into a mega-AI IPO later this year.

The pattern is clear: the US open-source-AI center of gravity has shifted away from the Mag 7 companies that built the playbook. Which raises the obvious question.

Who picks it up in the US?

In my strategic view, the field is wide open for Nvidia and Apple — for the reasons outlined below. And both companies have already been on my AI “Call Your Shot” list since 2024.

I made this call in August 2024 in RTZ #445, “Nvidia’s formidable Software Moat”, where I argued that Nvidia is fast becoming the OPERATING SYSTEM of the AI industry, led in particular by its long-time sustained investment in its open source CUDA frameworks around its growing family of AI GPUs and chips — and that Nvidia, Google, and Apple were on my “Call your shot” list of companies whose sum-of-the-parts puts them in pole position for the long term of this AI Tech Wave.

Google’s frontier AI has since gone closed. The other two — Nvidia and Apple — are now positioned to lead the US open-source AI counter over the next five years, for the same structural reason: both own the proprietary chokepoint underneath the open layer (silicon), so opening the layer above doesn’t threaten them — it helps them.

THE NVIDIA CASE:

19 years of open-source plumbing, now extending into AI models, Autonomous Vehicle (AV), and Robotics AI stacks

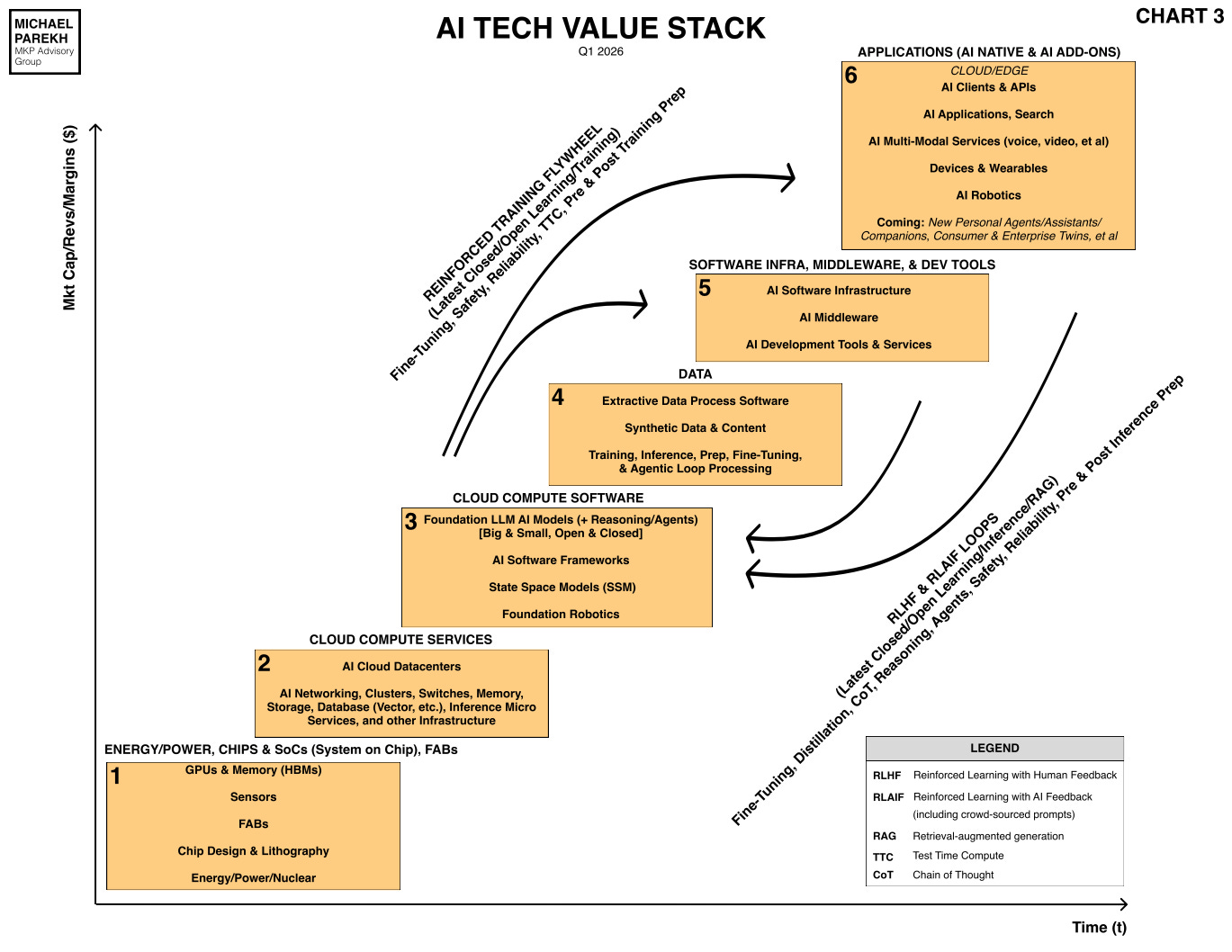

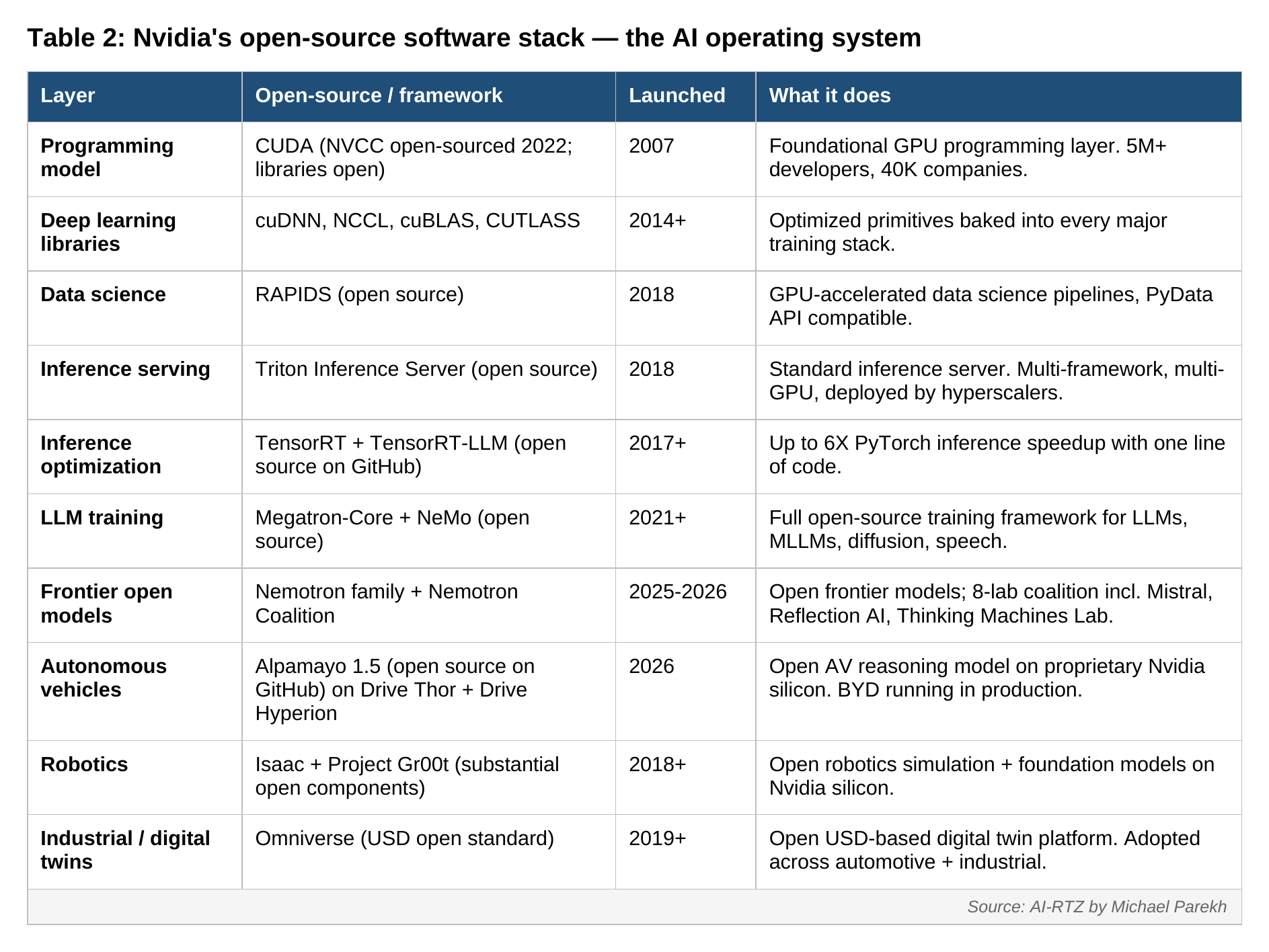

Jensen Huang has been operating the open-source-strategy playbook for years before most analysts noticed. Especially on the hardware side, since it had to do with software. That cost a lot of money for countless developers, and nominal revenue. The full-stack accelerated-computing strategy I described in RTZ #445 is built on a remarkably consistent posture: open at the framework, model, and application layers (Boxes 2-6) — proprietary at the AI accelerator silicon layer (Box 1). As seen in the AI Tech Stack below.

The Nvidia software moat is largely open source. As I noted in AI-RTZ #445, the CUDA platform launched in 2007 and now includes more than 300 code libraries, 600 AI models, 3,700 GPU-accelerated applications, used by more than 5 million developers at roughly 40,000 companies (as of Nvidia June 2024 shareholder meeting). That is the “Wintel of the AI age” — only this time the software is open source, and it’s the invisible key to Nvidia becoming a $5+ trillion market cap, global AI leader. With software margins to boot as a ‘hardware’ company.

Notably, it’s all just getting started into areas beyond LLM AIs.

The table below summarizes Nvidia’s open-source software stack as it stands today. Each layer is open at the framework level, with Nvidia’s proprietary silicon underneath.

Table 2: Nvidia’s open-source software stack — the AI operating system

Three live datapoints from 2026 that show the playbook compounding into AI base models and autonomous vehicle (AV) stacks:

Nvidia Nemotron Coalition (announced March 16, 2026 at GTC). Eight inaugural labs: Black Forest Labs, Cursor, LangChain, Mistral, Perplexity, Reflection AI, Sarvam, Thinking Machines Lab. First project is a base model co-developed by Mistral and Nvidia, trained on Nvidia DGX Cloud, underpinning the Nemotron 4 family. This is the Western open-frontier coalition not yet seen as one, by most observers.

Reflection AI, which I covered in RTZ #923, is now raising $2.5B at a $25B valuation, founded by ex-DeepMind researchers Misha Laskin and Ioannis Antonoglou, explicitly positioned as “America’s open frontier AI lab” against DeepSeek. Nvidia invested ~$800M in the October 2025 round and is a backer of the March 2026 round.

On the autonomous vehicle (AV) AI front, Nvidia Drive Hyperion + open-source Alpamayo 1.5 is running in production with BYD, Geely, Hyundai, Mercedes-Benz, Volvo, JLR, Polestar, Lucid, Stellantis, Toyota, and Uber’s 28-city autonomous fleet by 2028. BYD has integrated Alpamayo into its vehicle software pipeline for city driving in China, running on Drive Thor.

With Toyota and BYD, Nvidia has two of the world’s largest auto companies in its AI infrastructure fold.

Not yet appreciated by observers fixed mostly on Tesla and Google Waymo for AVs and robotaxis.

Worth noting: Nvidia’s open-licensing DNA showed up even in the 2020-2022 attempt to acquire ARM, the chip design company used by Apple and scores of others today for the semiconductors that drives their platforms.

The stated commitment was to maintain ARM’s open-licensing model and customer neutrality. When that deal collapsed under regulatory pressure, Nvidia pivoted to using all three instruction sets — x86, ARM, and RISC-V. RISC-V sits inside Nvidia’s own Bluefield DPUs today. The “any ISA, Nvidia accelerator alongside” posture is the same Open Source Strategy logic at the silicon-architecture layer.

So to summarize, Nvidia has been open source in AI longer and deeper than generally appreciated. In AI markets beyond LLMs.

THE APPLE CASE:

A hardware-first leadership CEO/Chief Hardware Officer pair takes over September 1, 2026

Apple is the under-discussed candidate, with an important transition coming up September 1, 2026. That is when Tim Cook becomes Executive Chairman, John Ternus, Apple hardware chief, becomes Apple CEO, and Johny Srouji, current head of Apple Silicon steps up as Chief Hardware Officer overseeing both Hardware Engineering and Hardware Technologies (i.e., chip design + product hardware combined under one executive).

For the first time in Apple’s modern history, the top two executives will both be hardware-first. Leveraging the global Supply juggernaut that Tim Cook put in place at Scale over the last 15+ years.

Ternus spent 25 years on iPad, AirPods, iPhone, Mac, and Apple Watch hardware engineering. Srouji has been pivotal in Apple’s transition to Apple Silicon — the M-series and A-series chip architecture that powers every Apple device today.

The structural read for AI: Apple does not run a frontier model lab, and is not trying to. It is the buyer of frontier capability — and the owner of the dominant on-device + small language model (SLM)-tier deployment platform via Apple Silicon. Apple Foundation Models (~3B-parameters on-device + mixture-of-experts server-side, shipped September 2025) are proprietary today, but they operate at the SLM tier where Apple Silicon’s on-device performance advantage is structural.

And the multi-vendor AI leveraging step is already visible. iOS 27 Extensions, anticipated at WWDC June 8, 2026 with public release fall 2026, ends OpenAI’s ChatGPT exclusivity by adding Google Gemini and Anthropic Claude as user-selectable Apple Intelligence backends. Bloomberg’s Mark Gurman recently reported OpenAI is weighing legal action against Apple because ChatGPT-Siri integration revenue fell short of “billions per year” expectations. Apple’s moves here are simultaneously breaking OpenAI’s exclusivity and OpenAI’s revenue model.

The two-to-three year potential AI path under Ternus and Srouji is straightforward. Apple opens — or partially opens — Foundation Models at the SLM tier initially, and potentially open source LLMs later, to drive developer ecosystem adoption.

Same “Mac for developers” playbook that worked in the 1980s, applied to on-device AI. Apple Silicon becomes the largest single deployment platform for Western open-weight SLMs — Reflection AI, Mistral, Phi, Gemma and many others, potentially ones from China as well— running on Apple-designed hardware. The proprietary chokepoint and foundation, is Apple Silicon. Everything above it can increasingly be open with nominal economic impact on Apple.

That is a powerful set of AI steps for Apple not generally appreciated.

Two of the largest market caps in the world. Both positioned to operate Open Source Strategy from the silicon-up. The Mag 7 companies that built the open-source playbook have largely vacated the AI frontier. Nvidia and Apple are the biggest potential natural successors with unique opportunities vs US/China players.

At both ends of the AI Compute spectrum, AI Data Center ‘AI Mainframes’, and Local AI Compute on computers, laptops and wearables.

A Bigger AI Pie: The next five years will not be only LLM AIs. As big as they seem to be today, they’re likely only the appetizer in the long-term AI opportunity.

Here is the broader point that gets lost in most US open-vs-closed AI discussions and debates.

The next five years of the AI Tech Wave is not just LLM AIs. I’ve written extensively about this branching out — most recently in RTZ #909, “Beyond LLM AIs to ‘World Models’”, and in the weekly summaries that track these adjacencies.

The AI Tech Wave today branches across at least seven distinct AI flavors, each with its own open-source dynamics. The table below maps where each flavor sits on the open-vs-closed spectrum, and where Nvidia and Apple are positioned within each.

Table 3: Seven AI flavors over the next five years — and where Nvidia and Apple sit

The pattern is striking. Across six of seven AI flavors, Nvidia is operating an Open Source Strategy play right now in 2026. Across the seventh (AI Devices), Apple operates a proprietary-but-multi-vendor-hedged variant that is structurally the same logic at a different layer. No other US company spans this breadth. Google has retreated to closed Gemini + Gemma-nano. Meta has retreated from Llama frontier. Microsoft has Phi + GitHub + Inception (closed). OpenAI is closed. Anthropic is closed. Elon’s xAI/Grok is closed.

Amazon AWS is tied to the ones above while offering open source options as customers ask for them.

The remaining open-source-AI ground in the US is dominated by Nvidia at the framework + AV + robotics + industrial + LLM-coalition tiers, and by Apple at the SLM + on-device + hedged-frontier tier. Together they cover the entire AI Tech Stack above.

The follower lanes — Gemma, Phi, and the Musk question

Two other US-side dynamics worth watching over the next 24 months.

Google Gemma and Microsoft Phi will likely ramp open-source efforts at the SLM tier over the next two to three years, driven by compute economics. The 100x inference cost compression of the last 18 months is forcing every hyperscaler to compete at the “good enough” SLM tier even while their frontier models stay closed. Gemma is currently committed at “nano size.” Phi (3.8B params) is already meaningful. Expect more from both — not because they want to, but because the cost curve makes closed-only economics indefensible at the on-device + edge tier where 6 billion people increasingly live.

Elon Musk and Grok/xAI, part of the upcoming mega SpaceXai IPO. Musk’s public rhetoric — including the ongoing lawsuit against OpenAI — positions xAI as the open-source champion against Altman.

The actual execution is a lag-and-open pattern. Grok-1 went open in March 2024 (four months after launch). Grok-2.5 in August 2025. Musk publicly promised Grok-3 would be open-sourced within six months of Grok-4 stability, with a likely February 2026 deadline. As of May 2026, that deadline has slipped and Grok-3 remains proprietary. Don’t expect frontier-Grok to go open on rhetoric alone. Watch the actual Grok-3 release. xAI’s commercial pressure — 50+ researcher departures post-SpaceX acquisition, co-founder Igor Babuschkin reportedly raising $1B for a new lab — may force a strategic pivot to true open-frontier as a follower’s weapon. But promises do not equal weights on Hugging Face.

A reality check from the Android-OS-fork on the smartphone front

Worth pausing on a smartphone topic easily missed in the open-vs-closed AI framework: open AI models spread globally; open smartphone OSes from China have not yet.

It’s worth discussing since the global smartphone market is measured in hundreds of millions of units annually, and is a market as large as AI today.

Huawei’s HarmonyOS Next — the clean break from Android, fully Huawei-proprietary kernel and ecosystem — sits at roughly 5% global market share, almost all of it China-domestic. The 2026 international rollout begins with Hong Kong, Southeast Asia, and the Middle East. India is a question mark here for now — Chinese smartphone OEMs (Vivo, OPPO, Xiaomi, Realme) collectively hold roughly 60% of India’s smartphone market, but they all ship Android, not HarmonyOS Next. Huawei itself has effectively no India presence. Europe and the US are not in the initial priority list. Xiaomi HyperOS is still Android-based underneath — a skin, not a fork.

The reason for discussing this hardware surface: open AI models are content, deployable on any cloud or local device, no controlled distribution channel required. Open mobile operating systems require carrier deals, OEM partnerships, app store ecosystems, and regulatory clearance — and HarmonyOS Next lacks Google Mobile Services and the top global apps natively. The distribution physics are completely different.

The implication for the five-year framework: China can win the rest of the world at the open-weight AI model tier without winning the device-OS layer. Google Android still rules the global Android smartphone marketplace outside China; iOS still rules the premium tier. Open AI travels on top of Android and iOS, not as a replacement for them. That is precisely why Apple Silicon + iOS 27 Extensions + on-device Foundation Models matter so much for the US open-source AI position — Apple owns the deployment layer that open AI travels on for billions of users worldwide.

A US/China framework for the next five years

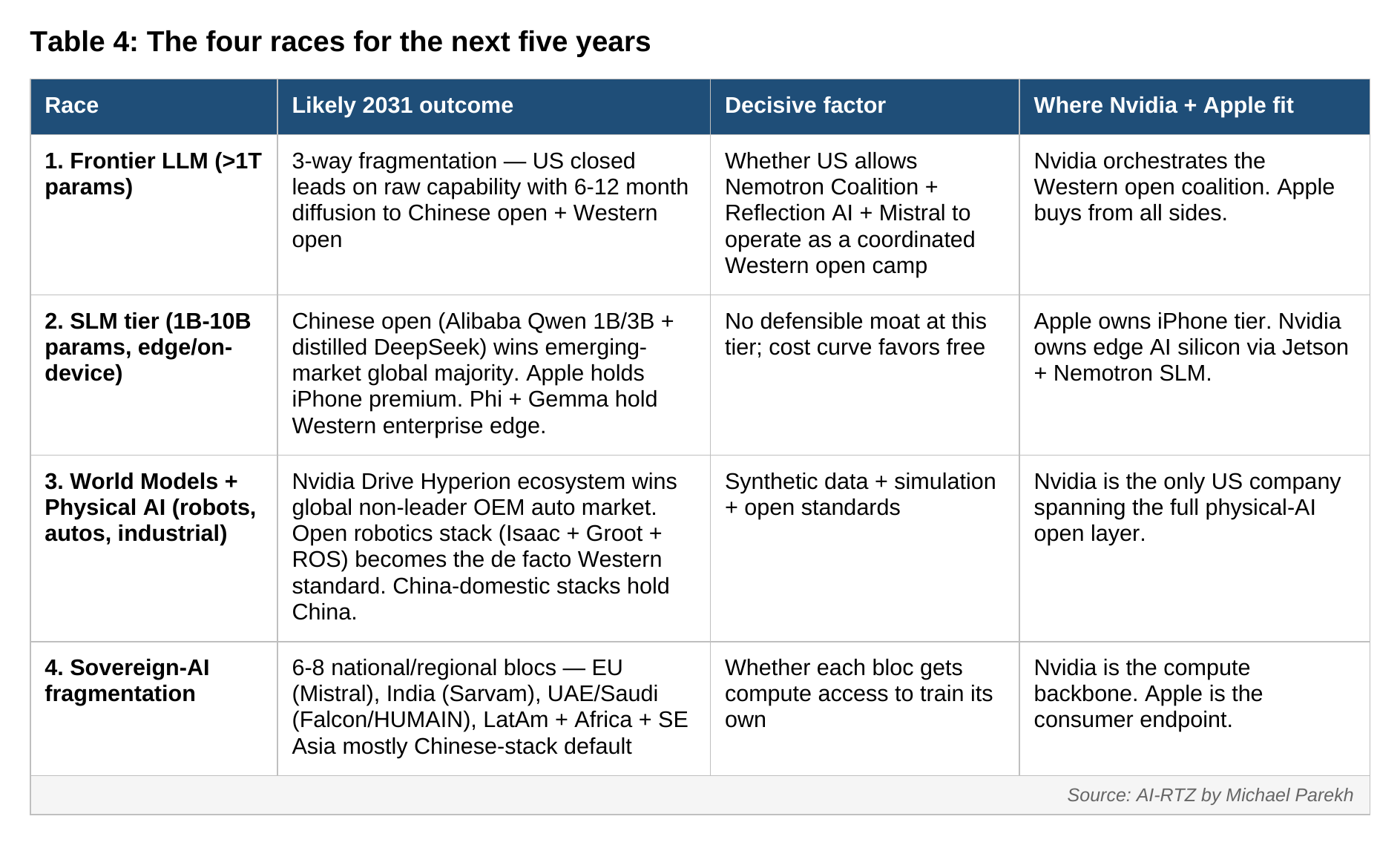

Pulling the threads together, the next five years (2026-2031) of the AI Space Race is not a binary of US-closed vs China-open. It splits into four parallel races, each going differently across the tech stacks for LLMs and beyond.

Table 4: The four races for the next five years

The five-year conclusion. China champions open across LLMs + SLMs + EVs + AVs + robotics for the emerging-market global majority. We’re talking Asia, Africa, South America, and Europe where there are openings and opportunities.

The possible constraint on a Chinese-only-wins scenario is the regulatory possibility that the US allows Nvidia + Nemotron Coalition + Reflection AI + Mistral to operate as a coordinated Western open camp, and whether Apple is allowed to open up Apple Silicon’s SLM tier to AI models from China.

If US regulatory politics — visible already in the April 2026 House Foreign Affairs + Select Committee on the CCP letters to Anysphere (makers of the hit AI Coding app Cursor), and Airbnb over their use of Chinese open-weight models — close the US market to both Chinese open and Western open, then the US loses the rest of the world by 2031.

If the Western open coalition is allowed to operate with Nvidia and Apple as the silicon-up anchors, 2031 ends with the US premium tier closed, a Western open coalition holding Western enterprise + local SLM edge, and Chinese open holding the emerging-market global majority.

The real question is not whether China will champion open source AI. It already is doing that in spades. The real question is whether the US will allow itself a coherent open-source counter — and whether Nvidia and Apple will take the opportunity to lead it. Unhindered by US regulators acting on lobbying from closed-source champions on geopolitical and AI security grounds.

Open source software has been proven to be at least as secure as alternatives if not more so over the last few decades. And the operating and financial efficiencies to end users, be they businesses and end consumers, are massive. Important enough for open source AI to be a lever that really expands global AI opportunities.

And in my view, Nvidia and Apple are best positioned amongst the US companies to run with this opportunity. Both for the US globally, and compete fair and square with China along the way.

That is the ‘Bigger Picture‘ to keep in mind in the coming months of this AI Tech Wave. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here)

Appendix: Sources and further reading

MP prior AI-RTZ posts cited or echoed in this piece

-

AI: Nvidia’s formidable Software Moat — RTZ #445 (Aug 11, 2024) — the original “Wintel of the AI age” + Call Your Shot list framing

-

AI: Beyond LLM AIs to ‘World Models’ — RTZ #909 (Nov 18, 2025) — the seven-flavor AI Tech Wave framing

-

AI: DeepSeek recharges Open Source AI debate — RTZ #619 (Feb 2, 2025) — Altman’s “wrong side of history” + Meta as lone BIG champion

-

AI: US companies building on Chinese open source LLM AI models — RTZ #923 (Dec 2, 2025) — Reflection AI debut, Alibaba Qwen, Fireworks AI

-

AI: OpenAI’s open source OpenClaw causing AI developer frenzy in China — RTZ #1016

Nvidia open source — software stack and AI moves

-

NVIDIA Launches Nemotron Coalition — NVIDIA newsroom March 16, 2026

-

Nvidia’s Nemotron coalition brings eight AI labs together — Tom’s Hardware

-

BYD, Geely, Isuzu, Nissan Adopt NVIDIA DRIVE Hyperion — NVIDIA newsroom March 2026

-

What is Alpamayo? Inside Nvidia’s plan to give autonomous cars a brain — Business News Today

-

Reflection AI raises $2B to be America’s open frontier AI lab — TechCrunch October 2025

-

Nvidia-backed Reflection eyes $2.5B at $25B valuation — Tech Startups March 2026

Apple — leadership change + AI posture

-

Johny Srouji named Apple’s Chief Hardware Officer — Apple Newsroom April 20, 2026

-

iOS 27 Will Let You Pick Claude or Gemini Instead of ChatGPT — MacRumors May 5, 2026

-

Apple Intelligence Foundation Language Models — Apple ML Research

Strategic context — open source as strategy

-

Bill Gurley, “From Open Source Software to Open Source Strategy,” P3 Institute, May 9, 2026

-

Two Loops: How China’s Open AI Strategy Reinforces Its Industrial Dominance — USCC, March 2026

-

The Global Implications of China’s 5-Year Plan AI Ambitions — The Diplomat, March 2026

Musk / Grok track record

Chinese Android forks

Red Hat IPO + IBM acquisition history

-

IBM closes its $34 billion acquisition of Red Hat — CNBC July 2019

-

Record IBM, Red Hat software deal — S&P Global Market Intelligence on advisor lineup