The Fed Capitulated – Where We Go From Here

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

-

Macro: Interest Rates, The Fed Fund

-

Markets: 13F Effects, Uber The Next City Circuit?

-

Company Earnings: PANW: Beat on earnings, Lowe’s: Revenue down 5.5%

-

AI: Agent-Based Innovation

In our Non-Consensus Episode this week, we discussed finance and investing with Mebane Faber, the Chief Investment Officer at Cambria Investment Management.

Click here for the full podcast, and don’t forget to subscribe.

TIMESTAMPS

01:11 Introduction: Meb Faber on non-consensus investing and ETFs.

02:29 Alpha Cloning: Hedge funds and market outperformance.

07:30 Market Trends: S&P vs. diversification post-GFC.

13:46 Shareholder Yield: Importance of buybacks and dividends.

18:35 Governance: Corporate strategies and leadership.

21:10 Hedge Funds: Buybacks, hedge fund strategies, and Jim Simons.

28:07 Active vs. Passive: Strategy comparison and Vanguard’s role.

33:58 Global Investing: Foreign vs. domestic strategies.

44:17 Retail Investing: Impact of retail investors and meme stocks.

49:08 Education: Teaching young investors fundamentals.

54:46 Strategies: Long-term investing and lessons learned.

Later in the week, we were joined by Michael Terpin, an investor at the forefront of the cryptocurrency revolution for Non-Consensus Investing Episode.

Check it out here on YouTube. Don’t forget to subscribe.

TIMESTAMPS

00:00 Introduction to Non-Consensus Investing

02:42 Michael’s Journey: From PR to Venture Capital

04:47 The Dot-Com Boom and Transition to Crypto

10:05 Understanding Bitcoin Cycles and Investment Strategies

15:19 Technical Aspects of Bitcoin and Market Dynamics

17:41 Current Market Trends and Future Predictions

23:09 Challenges and Opportunities in Bitcoin Investing

24:49 Technical Difficulties and Market Analysis

33:56 Bitcoin Halving Cycles and Market Trends

35:53 Bitcoin’s Parabolic Trends and Key Days

36:54 Bitcoin Winter and Market Cycles

38:04 Impact of New Products and ETFs

42:48 Strategic and Tactical Bitcoin Investments

49:51 Global Adoption and Inflation

54:34 Puerto Rico’s Crypto Community

01:04:03 Future Outlook for Bitcoin, ETH, and Solana

01:05:46 Conclusion

MACRO

The Fed flinched.

Fed Chair Powell, at the annual Jackson Hole event, assured markets that rate cuts are coming:

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

This will complete the Powell Pivot.

As you know, we did accept this. So did the market. The September rate cuts are highly anticipated.

However, rate cuts were also highly anticipated at the end of December, March, and July.

Lumida correctly navigated the ‘higher for longer.’ It was fairly simple – we listened to what the Fed was saying.

I find it amazing that Goldman Sachs and the futures market, consisting of tons of smart investors, were betting on a Fed pivot this year and last.

Our thesis was that the Fed’s primary goal was to restore its credibility. Leaving aside whether they did that or not, that requires the Fed to have a data-driven approach.

It also means the Fed needs to see a sustained shift in trend.

We now have had 3 months of benign CPI reports.

That said, it’s not clear to us at all that the Fed needed to cut rates.

I don’t believe that’s actually necessary.

The Fed is Data Driven.

Here’s what the data show:

-

Record asset prices

-

Record employment. (The unemployment rate is elevated due to immigration in the denominator)

-

Improving leading economic indicators

-

Coincident indicators continue to rise

-

Record energy production

-

Strong ISM services data

-

Weakness in ISM manufacturing – an ever-shrinking part of the U.S. economy

-

Two back-to-back beats on Retail Sales (consumers are spending on services and experiences rather than goods)

-

High yield spreads are tight, suggesting low default risk

The Fed is cutting rates due to a theoretical concern about ‘high real rates.’

This chart shows the real interest rate:

The biggest argument I hear for cutting rates is that the Real Interest Rates are above 2%, and that, ipso facto, is a scary idea.

After all, real rates were elevated going into the 2008 crisis, Dot Com crash, and 1979.

The argument is that these high real rates are ‘Restrictive’ and cause recessions.

This is not a well-tested theory.

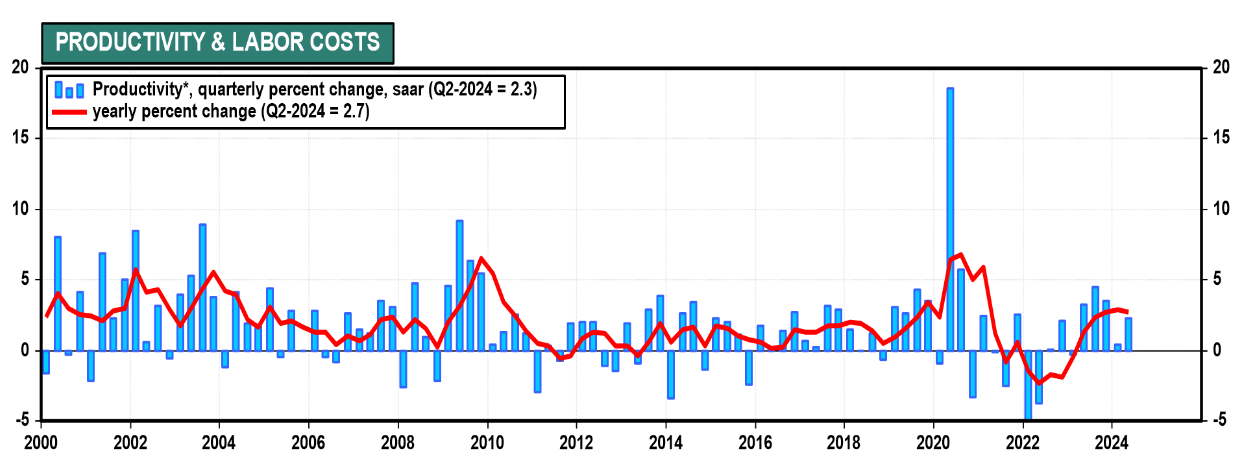

High real interest rates I argued last weekend that high real rates reflect a higher return on capital and higher productivity rates.

Ed Yardeni and Eric Wallenstein made the same point in the WSJ – I’m in broad agreement.

Excerpt:

The way you test a theory is your aim to falsify it.

Real interest rates were high during the mid to late 90s. There was no recession.

What happened in the mid to late 90s, and is happening now, is we are experiencing a productivity boom.

We see that reflected in record profit margins and record corporate earnings, which exceeded analyst estimates in aggregate.

What about the scary long and variable lags?

The argument is that high real rates increase debt service burdens.

Doesn’t higher rates cause a credit crisis?

We already have this – it’s called Commercial Real Estate.

That sector is about 40% through a 4-year clean-up process.

CRE developer-owners who took out floating rate loans before 2021 are in a world of pain.

We don’t see that because the pain is mostly in private markets, not public markets.

So, the long and variable lag impact happened. And it’s increasingly behind us.

Not all parts of the economy are cranking on all cylinders. That’s fine, too – otherwise, the Fed would need to raise rates and call the party off. The last time we had that was in November 2021 when the last wave of $Tn+ Covid “stimmy checks went out.

Back to the 90s.

Back then, the internet was on the rise.

There was a strong economic boom AND a stock market bubble despite ‘restrictive’ rates!

Don’t higher rates cause recessions?

Well, the 10-year went from 1.5% to 5%. The 10-year is used for long-duration borrowings, such as mortgages and corporates.

Longer-term rates are more influential than short-term rates in influencing economic behavior because they drive Consumer and Investment behavior in the GDP equation.

It’s true that higher accurate rates can cause a recession if we are talking about a massive upswing in rates like Paul Volcker in the 80s.

That’s not happening here.

Consider that lenders already credit spread above the risk-free rate is far more significant.

Credit card APRs are 20% to 29.99%. Does a downward shift of 100 bps change behavior on the margin? No.

There are also no credit bubbles today. There are no capex bubbles, either.

The spend hyperscalars have on Nvidia GPU chips is rational. They want to maintain relevance.

So where is the ‘restrictive’ rate punishing?

And the IPO markets are coming back…

Equities – which are forward-looking – have valuations in the top decile.

I believe the Fed has the causality backward.

Higher Net Present Value (NPV) projects and productivity should lead to more income growth.

Higher real interest rates mean the projects businesses are taking on are more productive. That’s great news!

We’ve come a long way from the 2021 era of SPACs.

We will see a lot more froth when the Fed cuts rates and growth, and value stocks could go into bubble mode after the election volatility.

Look around.

We have been living in a Boomer economy in recent years financed by T-Bills.

Is that good or bad? Well, it’s a normative call.

Higher real rates favor lenders and create discipline.

Lower real rates favor borrowers.

In other words, targeting a lower real interest rate just simply because they are above 2% rests on unproven flimsy logic.

It’s not supported by history, theory, or practice.

A normal world, without numerous Fed experiments, should lead to a higher real interest rate.

High real interest rates during an expansion are a marker of economic health.

Why does this matter?

Well, you want a sustainable bull market, not a bubble-then-bust dynamic.

It’s better to have a steady grind-up in asset prices and real economic variables rather than a swoosh-up.

If rate cuts are pre-mature and asset prices go into blast-off mode.

You get a melt-up.

Melt-ups eventually turn into melt-downs.

We saw that in 2021.

We had a bear market with no recession.

We saw that on July 16th, when the melt-up flipped into a melt-down.

We saw that during Covid.

We see that today in the behavior of securities prices with the hot ball of money sloshing around.

Remember when we bought Dell in January? It ran up 80%; then we sold it because it went from cheap and ignored to expensive and overbought in 4 months!

Since then, Dell has tanked and is back to January prices.

That’s the hot ball of liquidity I am referring to.

At Lumida, we track our baskets of discrete themes.

One is called Animal Spirits. It contains names like Palantir, Tesla, Crowdstrike, and other ‘hot money’ names.

That is one of the best-performing themes recently.

This is bullish for stocks, and we noted a few weeks ago you should remain bullish looking 1 to 3 months out.

We are seeing this play out in hyper-accelerated time.

The reality is that the ‘science’ of central banking if you can call it that, is immature and has a small sample size.

Better to go with the flow regardless.

It is better to make money rather than ‘be right.’

We expect continued breadth expansion.

What Happens To the Market After “Adjustment Cuts”

A full-fledged easing cycle is what occurs when the Fed expects or observes deterioriating employment (e.g., a recession).

The upcoming set of cuts (we expect 2 or 3 25 bps cuts starting in September) are “adjustment cuts”.

The Fed’s question is “How do we keep the show going without triggering inflation?”

We have seen these soft landings in 1995 and 2019. We know how the late 90s played out (bullish).

Let’s focus on 2019.

We discuss this here – recommend taking a look. Headline is we expect a year-end melt-up. After that, we should see returns subdued going into 2025 after rate-cuts are digested.

What happened after the Fed did ‘adjustment cuts’ in July 2019?

(after caving to market pressure)

Markets largely went parabolic in q4 and finished their rally at year-end with a 29% gain

I see a scenario like this as quite possible

Then in 2020, markets drifted steadily… x.com/i/web/status/1…

— Ram Ahluwalia CFA, Lumida (@ramahluwalia)

10:21 PM • Aug 24, 2024

On positioning, we expect small caps will do well and “quality value”.

We will see a junk rally with highly debt-laden firms crank higher, along with biotech. But, that’s a trade not a sustainable investment you can let compound for 10 years.

Weo do expect election-related volatility in the weeks and months ahead.

We are sticking with our view from August 5th that you should remain bullish looking out 1 to 3 months.

However, where we stand right now, the market has pulled forward quite a bit of returns. So, we are reluctant to deploy capital at these levels except for unique dislocations.

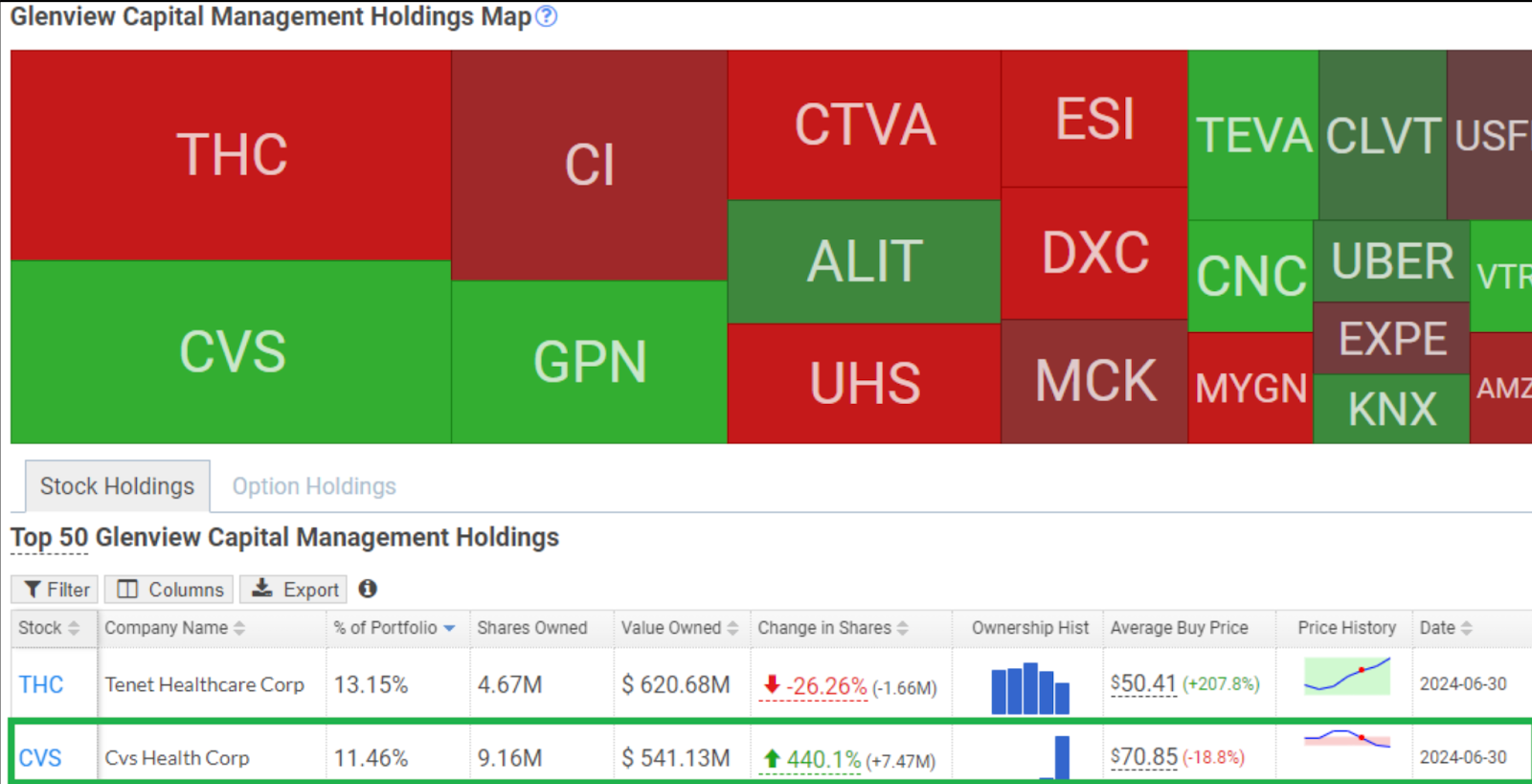

Glenview Capital Buys CVS (aka Aetna)

Larry Robbins has accumulated a sizeable position in $CVS.

At the end of June, the CVS position was 11.5% of his fund.

Glenview is a hedge fund that focuses on the healthcare sector.

They are a sector specialist.

That’s a great sign, as we are generalists.

(However, we do have a nice list of specialists in various categories.)

Scanning through Larry’s 13F, we see that he also owns the other healthcare names we think are high-quality businesses.

They are just too darned expensive.

The market knows demand for healthcare is going up, and that’s all baked into the price.

CVS (aka Aetna) was a ‘high-quality dislocated asset’ that allowed us to gain exposure to healthcare.

Healthcare as a percentage of GDP shows no sign of decreasing.

1) Expects 9 Bn in free cash flow in ‘24, on a 72 Bn market cap

8.1x forward PE and 11% free cash flow to market cap.

Compare that to the UNH multiple at 19.2x and fully valued.

2) The Turnaround is in motion.

Turnarounds are hard.

This is easy – you change your underwriting policy and shut down unprofitable stores.

‘In June, we submitted our bids for the 2025 Medicare Advantage plan.

Our bids underwent a rigorous internal review, and we are confident in our pricing for 2025, which reflects prudent assumptions for utilization trends.

Our actions are expected to drive 100 to 200 basis points of margin recovery in 2025 of our current baseline and start the multi-year pathway to achieving target margins of 4% to 5%.

> Those target margins are the margins of their peer group UNH and ELV

> I am happy if they get to 2 or 3%. With value plays, you can have lower expectations.

3) CVS closed most unprofitable stores; the remaining stores are profitable

> Bank of America went through a similar ‘store closing’ exercise in 2011. I was a young exec at BAML back then. The mood was gloomy. Turns out that was the best time to buy. The branch closures and BAC stock paid off nicely (up 7x a decade later).

> CVS retained 99% of employer clients despite closures

4) ‘Same-store pharmacy sales were up over 9% versus the prior year, and same-store prescription volumes increased by 6.5%.

We continued to increase our script share during the quarter, achieving a 27.2% retail pharmacy share.

Our results continue to demonstrate that we are the best-run national pharmacy chain in the country.’

5) The story for CVS turns on margins:

‘feel good that we’ll achieve the 100 to 200 basis points of margin recovery – that’s what we expect.

6) Bear Case?

The Bear Case is that health utilization remains elevated.

It takes a year or two to churn these older, unprofitable policies.

CVS does see a continued elevation in utilization. The new policies mitigate this (e.g., $0 deductible needs to stop)

Here’s what they say:

‘We had a substantial amount of contingency as we look at our 2024 baseline for those bids, and remember, for 2025, we assumed that the same trend persists for effectively a third year in 2025 at essentially a double-digit rate, very, very high abnormal trends.’

In other words, they are modeling the numbers conservatively.

CVS also dismissed the executive running Aetna. That’s accountability.

Straightforward management talk.

I added to our position here.

This idea will take a year or two to play out.

It’s not a fast idea. It’s a classic investment in a high-quality insurer attached to demographic solid trends that made a mistake in its underwriting.

Buffett bought into American Express after the latter had a significant screw-up called the ‘Salad Oil Scandal.’

All I’m betting on is that margins will get to baseline historical levels and that the multiple will, as well.

This type of position also adds a unique kind of ballast to the portfolio; it’s idiosyncratic and has no factor momentum.

Investing Tip: Own Leaders Gaining Market Share

I like owning dominant market leaders and growing market share while maintaining profitability.

Winners keep on winning.

I also like these at a reasonable valuation, so I don’t have to pay taxes and can simply let them compound.

Easier said than done!

Nvidia is one example of that.

GM is another example.

This chart shows GM’s market share vs. its peer group and TSLA.

GM continues to take share.

And, they are growing market share profitably with $10 Bn in buybacks funded by free cashflow

I can’t say the same for Ford.

Tesla, meanwhile, is losing market share.

Now, overlay the market caps for these businesses in your mind.

Tesla is worth more than the rest combined and then some. Expectations are high.

GM has a PE ratio in the 4s and change.

And it’s up 27% YTD, beating Mag 7 names like TSLA (down -13% YTD for the year) and AAPL.

This approach is easier said than done.

It takes work to spot a leader with a growing market share with a good valuation.

After a temporary news fiasco, Buffett found that in American Express many decades ago.

Bruce Berkowitz found that in BAC after the 2008 crisis.

Bill Ackman found that in Chipotle CMG after the food sanitation issues.

GM will continue outperforming TSLA and the S&P 500 more generally.

Fun Fact:

The Chevrolet Suburban was introduced in 1935. It has iterated over the decades and has set the standard for SUV design.

The Suburban is a brand in its own right.

Fun Fact 2:

Notice names like GM and value stocks like JXN have re-traced significantly or even recovered to near all-time highs.

However, Mag 7 names like Microsoft and Amazon are lagging.

The Growth to Value rotation continues to play out.

Be cautious of expensive growth stocks not posting solid earnings growth.

I love that GM is a boring Boomer stock that no one is talking about…

And it’s up 40% ish YTD.

The quietly ignored rallies with bad news priced in (eg, union negotiations last Nov) are nice.

I will have a new Boomer stock to share later this week, and it looks like a good entry

We are doing a deeper scrub.

The Boomer Theme is a powerful one.

Boomers drive the American economy with the disposable income from Treasury yields, whereas AI theme drives markets.

On Japan:

Japan had a 1987 style crash after recovering to its 1989 highs.

Japan, along with India, were ‘hot markets’ due to the corporate reform story.

We avoided it b/c it was hot.

The froth has dissipated now. So it’s interesting (although it has recovered)

If a trend is durable, you want to get into it after a correction.

Notably, there aren’t too many themes one can be bearish on with the breadth expansion.

Consumer discretionary is back with strong back-to-back retail sales.

EVs are still a dumpster fire, I guess

Regional banks and REITs have rallied strongly on rate citation expectations.

So has biotech

‘Everything not printed is up.’

If you believe, like I do, that a recession was not in the cards (not even close), the. You should also believe that there is no need for Sept rate cuts

If you share my view that the economy is fine, then rate cuts likely cause a year-end melt-up

Although I am tactically cautious after being aggressively bullish on the Monday panic, I see the bigger trend in one word: up.

One irony about markets is this…

The best time to do a yen carry trade is just after a yen carry trade blows up.

Separately, there are still bargains in Japan.

LumidaWealth is studying one name closely.

MARKETS

I know several large investors in T-bills are waiting for rate cuts to drop before they rotate into equities.

Do you think Mr Market will wait for them?

These investors like clipping coupons and have missed an incredible rally for a 5% pre-tax return.

I expect that Q4 rotation into equities will be bullish, and we will see ATH at year-end (with election-related volatility between now and then).

But that T-bill crowd has wholly misplayed this.

The irony is the best time to invest is when rates are high!

The equity market bottomed in 1982.

My friend familyoffice (Angelo Robles) asked me in Oct ‘23 whether it was better to buy t-bills at 5% or equities.

That was a real game-time decision with a correct answer.

Here’s what I said:

https://www.youtube.com/clip/UgkxEYKj4uclzs-x5bKp5_aGXzZ_DXrpuHh-?si=ZPbBf8C3yiCseRVL

Angelo and I will be doing another show in September.

They cover so many topics and are always fun.

GOLDMAN: “.. The volatile macro backdrop .. has distracted many investors from appreciating the widespread strength of the 2Q earnings season. 56% of S&P 500 companies beat consensus .. well above the long-term average of 48%.

“We maintain our 2024 S&P 500 EPS estimate of $241” SPX.

Explore becoming a Lumida Wealth client: learn more about our Crypto White Glove Service or Click here to explore our Wealth & Family Office Services.

Do people buy what HF managers bought 45 days earlier?

Yes, I am convinced there is a 13F effect.

Three managers bought into China, specifically BABA.

And the name is up immediately after

Larry Robbins buys CVS, and the name outperforms its benchmark immediately after

China remains in a bull market after our capitulation call back in early Feb, despite generally weak data coming out of China.

It is, however, OB. And there are great businesses in the U.S. small-cap market that are still attractively priced.

And same for Mexico and Brazil

There are a number of opportunities out there, and the breadth continues to expand.

George Soros’s Soros Fund Management Releases its 13F #LumidaWhaleWatch

Here’s what changed from last Quarter.

Top 5 Holdings

Q2 2024: AER, GOOGL, WRK, AZN, SPY

vs Q1 2024: CERE, NVO, AEL, AER, GOOGL

Shift towards materials and healthcare with WRK and AZN.

Top 5 New Additions

Q2 2024: NEE+S, SRCL, BABA, CHX, SPY

vs Q1 2024: RUN, PCG, WRK, OKTA, CERE

Q2 emphasizes renewable energy and Chinese e-commerce.

Top 5 Reduced Positions

Q2 2024: CRH, AMZN, BKNG, AER, GOOGL

vs Q1 2024: J, CEH, AMZN, NVO, AER

Consistent reduction in AER and AMZN.

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

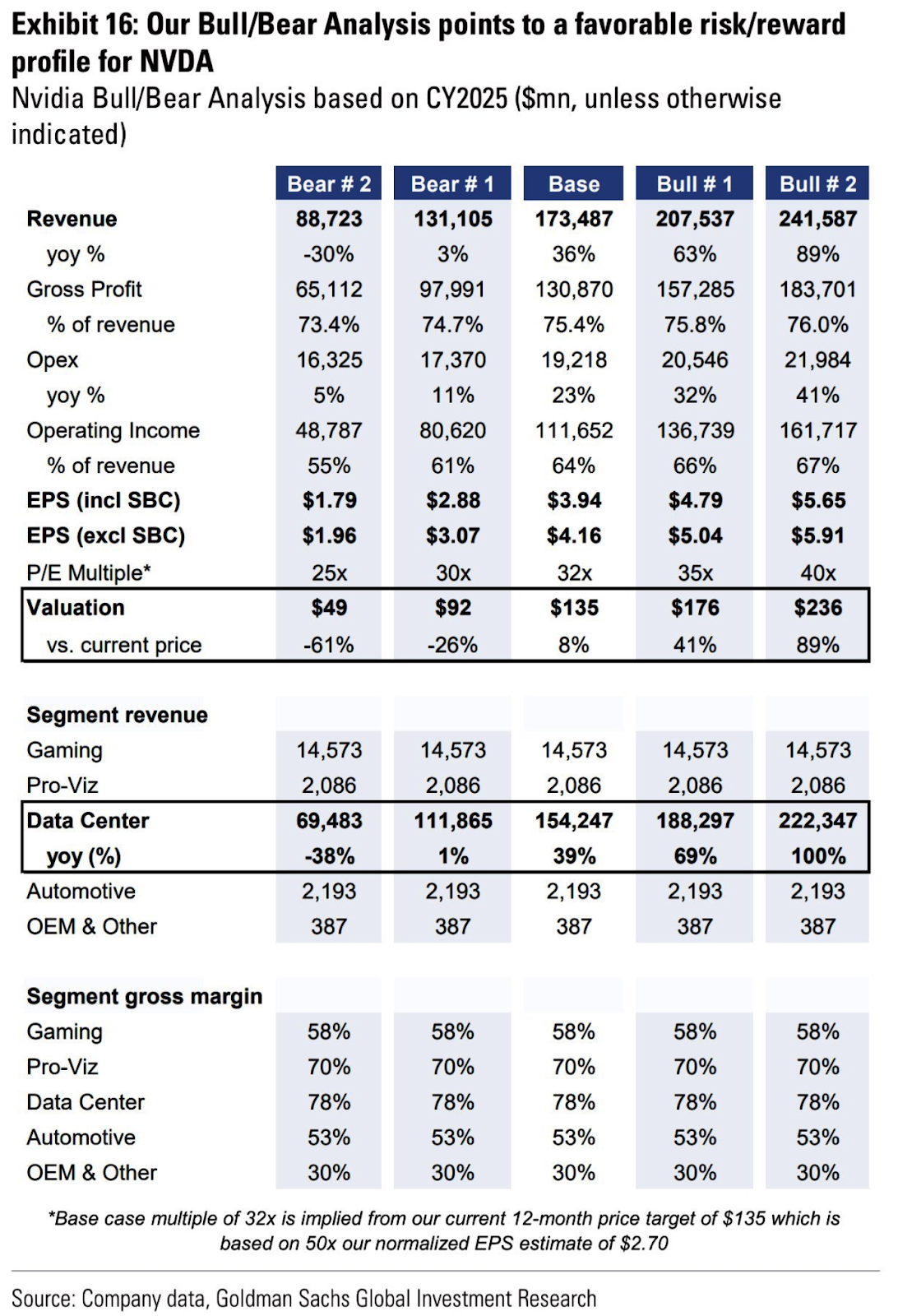

NVDA – Goldman Sachs Bull #2 at $234 a share, ~89% from the current level.

The data center would be at $222Bn, double Y/Y again.

Is it realistic ?

IS UBER THE NEXT CIRCUIT CITY?

In what world do we see driverless cars proliferate and $UBER survive?

Today, Uber is capital light.

The driver brings the car. The driver maintains the car.

If driverless cars are a reality, Uber would need to acquire a fleet.

This is capex-heavy and would kill the beautiful economics of the app model.

And, in a driverless car world, the world needs less cars.

So, we don’t need Uber to acquire a fleet.

Maybe Uber can pivot the app.

They could match owners of autonomous cars with passengers instead of matching drivers with passengers.

(In a great twist of fate, Uber would then be the Airbnb of cars; no longer would startups be the Uber of )

More likely, however, people will expect standards.

Passengers will want expectations of safety, cleanliness, and reliability that only specialized fleet operators can deliver.

In the late 90s, I kid you not, there was a great debate about whether Amazon or eBay would be the winner of online retail.

Of course, Amazon won because of standards like express shipping and TRUST in the Amazon brand.

An assorted mix of vehicles from homeowners, in this analogy, would the be the modern analogy of eBay getting into ride-sharing.

I don’t see that working.

It doesn’t work for the car owner, either.

Owning a car will tie up too much capital, insurance costs, and, crucially – liability.

What happens when your car runs over your neighbor’s pet, and your sensors are faulty?

More likely, we see large regulated fleet pool operators that have a low cost of capital and more efficient maintenance, repair, and service.

What does that business resemble today?

That is finance & logistics heavy business.

You need low-cost capital to finance the capex.

The business is closer to XPO Logistics and UPS than Uber.

The other takeaway…

The internet disrupted the old world:

…brick and mortar, vinyl, cable TV, newspapers, discount brokerage, classified ads, etc.

AI is disrupting tech.

It’s tech-on-tech violence.

And it will happen at a faster pace.

There are richly valued tech companies that look similarly vulnerable.

Will share more in the @LumidaWealth Lumida Ledger.

Nietzsche should have said, ‘SaaS is dead.’

Snowflake is down 7% after earnings.

Fmr CEO Slootman top ticked his exit

How will Altimeter exit this holding gracefully?

The market sees the selling in the 13F

COMPANY EARNINGS

Technology, Media, Telecom

-

Palo Alto Networks (PANW): Beat on earnings and revenue. Revenue up 12.8% YoY. Strong growth outlook with positive Q1 FY2025 guidance.

-

Zoom (ZM): Beat on earnings and revenue. Revenue up 1.8% YoY. Slightly above consensus FY2025 revenue projection.

-

Snowflake (SNOW): Beat on earnings and revenue. Revenue up 28.9% YoY. Share price declined despite strong revenue growth.

-

Synopsys (SNPS): Beat on earnings and revenue. Revenue up 13.3% YoY. Positive market reaction with a share price increase.

-

Intuit (INTU): Beat on earnings and revenue. Revenue up 17.3% YoY. Strong performance in Small Business and Self-Employed Groups.

-

Workday (WDAY): Beat on earnings and revenue. Revenue up 16.2% YoY. Encouraging subscription revenue guidance for fiscal 2025.

-

Baidu (BIDU): Beat on earnings, revenue miss. Revenue flat YoY. Solid adjusted EBITDA margin despite flat revenue.

Consumer Discretionary

-

Lowe’s (LOW): Beat on earnings, revenue miss. Revenue down 5.5% YoY. Revised downward full-year sales outlook.

-

Target (TGT): Beat on earnings and revenue. Revenue up 2.7% YoY. Strong consumer traffic driving Q2 comparable sales.

-

Ross Stores (ROST): Beat on earnings and revenue. Revenue up 7.3% YoY. Positive market response with share price increase.

|

Sector |

Company ticker |

Beat or Miss (Relative View) |

Revenue (Absolute View) |

Highlight |

|

Technology, Media, Telecom |

Palo Alto Networks (PANW) |

Earnings beat by 6.95%, Revenue beat by 1.21% |

$2.19B, up 12.8% YoY |

Q1 FY2025 revenue guidance set at $2.10-$2.13 billion, reflecting 12-13% YoY growth. |

|

Consumer Discretionary |

Lowe’s (LOW) |

Earnings beat by 2.5%, Revenue miss by 1.5% |

$23.59B, down 5.5% YoY |

Full-year 2024 sales outlook revised down to $82.7-$83.2 billion. |

|

Technology, Media, Telecom |

Zoom (ZM) |

Earnings beat by 13.9%, Revenue beat by 0.9% |

$1.16B, up 1.8% YoY |

Full FY2025 revenue projected at $4.630-$4.640 billion, slightly above consensus. |

|

Technology, Media, Telecom |

Snowflake (SNOW) |

Earnings beat by 12.5%, Revenue beat by 2.2% |

$868.82M, up 28.9% YoY |

Shares decreased by 8.51% after results. |

|

Consumer Discretionary |

Target (TGT) |

Earnings beat by 17.9%, Revenue beat by 0.95% |

$25.45B, up 2.7% YoY |

Target’s Q2 comparable sales increased by 2.0%, driven by strong consumer traffic. |

|

Technology, Media, Telecom |

Synopsys (SNPS) |

Earnings beat by 4.3%, Revenue beat by 0.66% |

$1.53B, up 13.3% YoY |

Shares increased by 1.3% following the results. |

|

Technology, Media, Telecom |

Intuit (INTU) |

Earnings beat by 7.6%, Revenue beat by 2.9% |

$3.18B, up 17.3% YoY |

Small Business and Self-Employed Group revenue increased by 20% to $2.6 billion. |

|

Technology, Media, Telecom |

Workday (WDAY) |

Earnings beat by 6.1%, Revenue beat by 0.48% |

$2.08B, up 16.2% YoY |

Subscription revenue guidance for fiscal 2025 is set between $7.700 billion to $7.725 billion. |

|

Technology, Media, Telecom |

Baidu (BIDU) |

Earnings beat by 11.2%, Revenue miss by 1.48% |

$4.67B, flat YoY |

Adjusted EBITDA was $1.26 billion with a margin of 27%. |

|

Consumer Discretionary |

Ross Stores (ROST) |

Earnings beat by 6.7%, Revenue beat by 0.76% |

$5.29B, up 7.3% YoY |

Shares increased by 5.14% following the results. |

Explore becoming a Lumida Wealth client: learn more about our Crypto White Glove Service or Click here to explore our Wealth & Family Office Services.

Click here to explore becoming a Lumida Wealth client

AI

We see this happening now at YC. The next two years will happen very fast.

Eric Schmidt is right about this.

CYBERSECURITY: HOW TO PLAY IT?

Our view is that the best way to bet on cybersecurity is at the early-stage or Series A venture level.

In public markets, cybersecurity is expensive.

I don’t want to name names… but yes, the one you are thinking about is pricey.

The cybersecurity firms in public markets have strong differentiation (e.g., platform approach vs. identity solutions vs. data security, etc.).

The pressure to grow earnings and acquire to have holistic offerings is growing – creating more competiton.

At the same time, Big Tech firms like Google are encroaching on cyber security as they seek to ‘bolt-on’ to their extant data warehouse offerings

See Google’s thwarted $20 Bn+ acquisition bid for Wiz as one example.

Big Tech firms have done an incredible job of maintaining relevance and earnings growth — and cybersecurity + cloud analytics are the two areas various firms are focused on (see MSFT AMZN GOOG)

Further, multiple private cybersecurity firms are fetching significant amounts due to the competition to acquire in public markets.

Although I believe that Venture Capital is an extremely difficult category (“Show me the DPI”), this and a few other niches within VC are interesting…

Personally, I am happy to report my younger brother is engaged! He is the “last Ahluwalia” to get engaged.

We’re thrilled and happy to spend time with him.

On that note, I’ll keep this newsletter brief, and we’ll see you next week.

By the way, check out www.lumida.com when you get a chance. It’s a Drudge Report for news we are testing.

Quote of the Week

“The stock market is a device for transferring money from the impatient to the patient.”– Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.