The Oil Price Spike and Insider Selling

Here’s a preview of what we’ll cover this week:

-

Macro: Costco Seconds A Healthy Economy

-

Markets: Strategic vs. Tactical; Time To Leave Oilfield Services; No One Left To Sell; Cheap, Cash-Generative, Ignored; Oil and The Geopolitical Spike; THE S&P: Magical or No?

-

Lumida Curations: Software Selloff or Buying Opportunity?; The Energy Race Powering the AI Boom; The $1 Trillion AI Question

Spotlight

This week, I sat down with Alex Wilson for a Lumida Non-consensus investing podcast— serial founder, and co-creator of The Giving Block, which he later sold to Shift4.

We covered the payments category: why it’s been in a bear market, where the value is hiding, and why Stripe’s $130B private valuation doesn’t hold up against public market comps.

We also got into Alex’s new venture Cyclops — a picks-and-shovels infrastructure play helping payment processors close the gap on stable coins and crypto rails.

Watch the full Lumida Non-consensus investing podcast on Youtube here.

We are also on Apple podcast and Spotify.

Strategic vs. Tactical

Over the last few weeks, since our ‘Markets at a Crossroads’ piece we’ve taken a bearish stance on markets.

I did an FSD stream this week, titled ‘tactical vs strategic’, where I laid out the current standing of equity markets from both a strategic and tactical lens.

In short, the strategic view is bearish. The tactical view suggests we are prone to a sharp rally on the whiff of almost any good news.

Let me explain the difference.

The Strategic View: Multiple Bubbles, One Market

The big picture for markets isn’t great.

There isn’t one problem.

It’s several problems stacked on top of each other — each with its own unwind timeline, each connected to the others in ways the market hasn’t fully priced yet.

Here’s the issues list:

-

OpenAI and Anthropic have $1 Tn revenue forecasts, and committed obligations (e.g., debt) across the datacenter ecosystem. They face capital constraints.

-

Private Credit. We’re seeing redemptions and gating. That will continue. Private credit finances, in part, the datacenter expansion

-

Regional Banks are providing back leverage to Private Credit.

-

Industrial stocks are in a bubble, and started breaking down this week. The leading industrial names (e.g,. Caterpillar, GE Vernova, Corning, etc.) are all linked back to the OpenAI theme.

-

Elevated Positioning

and add to this lift the rising inflation concerns from the spike of oil which creates inflation risk. There’s nothing worse for markets than elevated inflation concerns.

We’ve flagged most of these individually over the past few weeks.

1. Private Credit

The pain in private credit isn’t done.

This week, BlackRock told investors it would not redeem more than 5% of their capital. Shares dropped on the news.

That 5% ceiling isn’t a BlackRock-specific policy — it’s the structural limit baked into most 40-Act private credit funds.

Cash flow generation on these vehicles runs 5–7%, enough to service normal outflows. Not a rush to the exit.

More gating events are coming across the category.

The deeper issue is loan quality.

The 2021 vintage is where the stress is concentrated — cheap money met aggressive underwriting, and those loans are now seasoning in a different rate environment.

The tell isn’t non-accrual rates, which can look clean on paper. The tell is loan modifications.

Modifications are the private credit version of pretend and extend — they restructure terms to avoid a technical default without fixing the underlying business. They just delay recognition.

If you have private credit exposure, ask three questions: how much is 2021 vintage, what percentage of the book has been modified, and what’s the non-accrual rate.

The answers will tell you more than any headline return figure.

To be clear — the economy is still fine.

An elevated default picture in private credit doesn’t mean zero returns. It means you make 5% instead of 10 to 12%.

The ripple effect is worth watching though.

Several regional banks have financed these private credit vehicles. If default rates tick up, we might see impacts there.

The valuations are still high for Blackstone and KKR, which add to their vulnerability.

Apollo looks relatively cleaner. But I’ve been burned before finding the right name inside a broken theme.

The theme has issues. You can’t fully outrun that.

2. The Semiconductor and Datacenter Complex

This week, Oracle exited its commitment under the Stargate joint venture, citing free cash flow concerns.

Oracle spent the last several quarters positioning itself as a core infrastructure partner for OpenAI.

They signed large revenue performance obligations, raising $25B in debt, $25B in equity to fund the buildout.

That capital raise was a tell in itself.

You don’t raise that kind of money unless you believe your customer can’t pay your bills. Oracle gets an up-front payment, but then must undertake a multi-year capex build out. They have credit risk on OpenAI.

Now they’re unwinding the Stargate commitment and cutting headcount. Meta assumed that obligation. But, there are over $100 Bn+ in obligations…

The implied reason is simpler: Oracle doesn’t have confidence in OpenAI’s ability to pay, and neither does the market.

We wrote about this months ago in our newsletter on ‘How Sam Altman broke the world?’.

By the way, Oracle senior executives including the Co-CEOs have sold over $4 Bn in stock including in recent months.

OpenAI has roughly $1 trillion in committed spending obligations across its datacenter and semiconductor partners.

Those obligations don’t appear as debt on OpenAI’s balance sheet — they’re structured as contractual arrangements.

But they show up as assets on their suppliers’ books as accounts receivables (asset).

The question markets are now being forced to ask is what those assets are actually worth if OpenAI can’t fund them.

Oracle is in a structurally similar position: assets on the book whose face value depends on a counterparty that is fundamentally short of cash.

Meta assuming the agreement changes the risk profile of that specific contract — Zuckerberg has the cash flow to back it.

But every other provider still holding OpenAI-linked obligations has to run the same math Oracle just ran.

The results won’t be good for earnings, and thus valuations.

Markets are repricing the datacenter complex.

Micron’s chart, for what it’s worth, confirms the pressure. It’s broken below the 50-day moving average. Not something I’m touching here.

That is a very bad open for the Semiconductor complex.

We believe the Micron trade is over.

3. Industrials

This is a bubble that hasn’t finished popping.

Look at Caterpillar’s trailing P/E.

CAT’s core datacenter link is its industrial generators — hyperscale facilities need massive backup (and increasingly primary) power, and grid interconnection delays mean on-site CAT generation runs longer than originally planned. The Energy & Transportation segment (~40% of revenues) is where this shows up, specifically large-bore reciprocating gas and diesel engines with 18–24 month lead times.

It’s a capex-cycle play, not recurring revenue, so the risk is order book deterioration if hyperscaler build rates slow.

Now, if CapEx is slowing due to capital dependancy issues and cancelled contracts, what does that mean for Caterpillar? Not good. (We are short CAT as of this past week – always wait for the “right shoulder”…)

Caterpillar went into bubble territory, and we think it comes down to earth.

Look at Corning (GLW) — where the entire executive team has been selling stock for months.

(Note: You can use the www.lumidainvest.com app to track insider selling and buying for your stocks. We’ll soon be adding AI tech that automatically scans your portfolio to detect hidden risks like this and others. If you want get on the waitlist to to invest in Lumida ahread of our public launch, visit www.lumidatribe.com. )

Look at Teradyne (TER) trading at 70x earnings on the back of an Amazon contract.

So what if you have a robotis contract with Amazon? Intuitive Surgical has a robotic story. It’s down over the past year. People fell in love with their ideas way too much.

What if Amazon pulls back capex? They are also laying off workers and issuing debt to shore up free cashflow.

That’s the question no one in those names is asking.

We’re short Caterpillar.

The broader industrial theme is expensive, and it’s starting to crack. Industrials are a large part of the S&P 500 – this is a major concern point.

4. Oil and the Strait of Hormuz

This is the newest entry on the list.

The market got rattled this week by a Bloomberg piece featuring a retired admiral who laid out Iran’s asymmetric capabilities — thousands of mines and speedboats in the Strait.

The article went viral. Markets felt it immediately.

We believe the U.S. has an overwhelming advantage over Iran.

In Hegseth’s presser last Thursday, there was no Q&A. Minimal messaging from the White House on the SPR or tanker logistics.

Here’s the reality: oil moving through the Strait is the jugular of global energy supply.

You don’t need Iran to “win” a conflict to disrupt it.

Until tankers start moving again, oil prices stay elevated.

Elevated oil is an inflation input, a consumer spending headwind, and a Fed rate cut killer — all at once.

This is what makes the strategic view uncomfortable.

None of these four issues exist in isolation.

Private credit stress links to regional bank exposure.

OpenAI counterparty risk links to the datacenter and semiconductor complex.

Industrials valuations were inflated by the same AI capex narrative.

And oil — the newest entrant — is the macro wildcard that tightens everything simultaneously.

It’s worth drawing the parallel here with 2022.

We had war-related shock, Inflation pressure, Midterm year, Nonsense in private markets, and Crowded valuations in certain categories.

Back then, the bubble was in software and payments. Those categories spent three years decompressing.

Now the bubble has migrated: into industrials, datacenter-linked names, private venture capital, and hot thematics.

Crypto was the first ‘hot thematic’ to crack – immediately after the peak euphoria of the Genius Act.

We’re seeing marginal liquidity markets an thematics under-perform now, and give way to value and international stocks.

We believe that trend will continue. It’s a great time to be a long / short investor.

The Tactical View

Here’s where the picture changes.

VIX at 29 going into a Monday is panic-level fear.

That’s historically unsustainable.

You almost always get a mean reversion — a multi-day, multi-week bounce — when fear reaches this pitch.

Often times you see a Monday gap down open. You will see a lot of volatility, include a large open to high print that can get faded and move to new lows. And possibly a Turnaround Tuesday type rally.

We are seeing large nasty red candles across many chart and sectors selling off in unison. That’s weirdly a good sign to see. Any whiff of good news on tankers would send many stocks soaring.

However, we think such rallies would ultimately be faded.

We see staples rolling over (see XLP) below.

Staples no longer offer a safe haven. Who is buying Walmart or Costco at 40x PE. (We are short Walmart). And the Walmart family is selling their stock en masse.

We saw a similar set of conditions in the dotcom era. There would be punctuated sharp and furious multi-week rallies when the Vix hit 30. Then markets would roll over again.

If capex does pull back, and we think it does due to capital markets forcing the issue – that would have slower growth implications for GDP and corporate earnings that are not priced into stocks. Analysts estimates would be too bullish. Markets are re-discounting those assumptions.

That doesn’t mean you don’t get a sharp rally on Tuesday, let’s say, due to tankers flowing and the release of oil.

Incidentally, if that happens, energy names that have rallied would likely decline. There’s a lot of ‘whipsaw’ risk in the market.

Where I’m Finding Ideas

The chess term for being in an optimal but constrained position — where every move deteriorates your situation — is Zugzwang.

That’s what markets feel like right now in most sectors.

But there are a few pockets that look interesting through that fog.

The best approach is to buy good businesses, priced well, that sold off hard due to present geopolitics that don’t impact the long-term earnings power of the company.

United Airlines.

I put a toe in UAL at the close. It’s a partial position. Half of me thinks we may be 1 day early. But, there’s a chance Trump says something constructive like releasing the SPR, so need to have some exposure.

6.9x forward P/E with FCF yield at ~9%.

When oil prices drop — and they will — the stock recovers.

Airlines also have the chance to hedge their oil prices, which will help produce better results than the market is expecting at current valuations.

And, oil futures prices looking a few months out is still in the low 70s range. Even today, airlines can hedge energy risks. So, the sell-off seems overblow.

The demand is Boomer-driven, who are still going to travel once geopolitics recede.

Overall, UAL is a real business at a dislocated valuation.

Interestingly, going into this week last Sunday evening I noted that the worst thing you can own are airlines and we were short the $JETS ETF (since covered).

Markets require mental flexibility.

China and Emerging Markets.

China imports heavily from the Strait of Hormuz.

So does Japan. So does South Korea, which has already taken an 18% drawdown from peak.

When the oil disruption resolves, these are the beneficiaries.

We noticed South Korea and China went up on Friday despite a rising oil price.

When you see positive news despite negative headlines, that’s constructive.

Still, it could be early or a relief bounce. That’s entirely possible. At the same time, valuations are attractive again. So, taking an initial investor position makes sense.

We added some PDD and already own Tencent, and added EWY.

Here’s a chart of PDD.

China is getting hurt due to stronger dollar. Dollar will weaken as conflict abates. We want to start accumulating at favorable levels and be patient. If we buy businesses priced right, we expect to do well.

The long-term earnings power of these businesses is not determined by the short-term price of a barrel of oil.

One More Indicator to Watch: Insider Activity

When management teams sell, listen.

I’ve found two names this week where the insider selling picture is alarming.

Corning (GLW) was one.

The other I won’t name, but the pattern was worse: not just the CEO or CFO, but the Chief People Officer were selling too.

When everyone from the C-suite to HR is liquidating, that’s not confidence.

Now, how do you check insider activity for all stocks quickly?

This is exactly the kind of edge the Lumida Invest app is built for.

We track Insider activity on all stocks, and help you filter stocks with highest insider sales and buys.

But that’s one piece.

The app also gives you AI-driven bull and bear analysis on individual stocks, insights from hedge fund positioning, and theme and factor analysis for your portfolio.

The goal is simple: give everyday investors the same quality of information that institutional desks get.

If you’d like to try it, sign up at lumidainvest.com.

Lumida is Scaling. Join Us Now and Own the Future of Investing.

Lumida has about 9 developers feverishly building the wealth manager for the next generation. We aim to take on RobinHood – but with an AI-native, mass affluent focus.

We want to invite our community to be a part of the journey.

$84 trillion is transferring to the next generation. And the wealth management industry isn’t ready for them.

The next generation doesn’t want to attend the US Open with an old-school banker. They’re not watching CNBC.

They live online. They find their news on TikTok, learn on YouTube, and trust personalities over institutions.

Traditional wealth managers have spent decades building businesses for a generation that is handing the keys over.

That’s the opportunity.

Lumida is building the wealth management firm for this generation — digital-native, AI-powered, and built from the ground up to serve investors who think differently.

We envision a world where an AI advisor understands your family’s goals as clearly as you do.

One that speaks your language, operates at your pace, and never stops working. You can talk to your advisor at 2AM in your pajamas. On your terms.

We are already executing on that vision.

The Lumida Invest SuperApp puts institutional-grade research in your pocket — AI bull/bear analysis, hedge fund 13F tracking, insider activity signals, and private market deal access.

Join our investor community and be part of our growth. We will launch an equity crowdfunding soon.

This is the waitlist. We already have 100 sign-ups, and we’ll prioritize allocations as best as we can. We’d rather have as much participation as possible to amp up social media impact and our events strategy.

You’ll see our strong revenue growth (with third party audited financials) and valuation details soon to follow before you need to make your final decision.

The waitlist will get you access to these communications.

Macro

Costco Seconds A Healthy Economy

Costco reported Q2 2026 earnings this week. Net sales grew 9.1% to $68.2B. Net income came in at $2.03B, up nearly 14% year over year.

The transcript provides a clean read on the state of the economy.

Management highlights the consumer is still spending.

CFO Gary Millerchip confirmed that members “are willing to and have the capacity to spend” — and it’s showing up in the data.

Traffic increased 3.1% worldwide. Average transaction was up 4.2%. People are visiting more and spending more per trip.

On inflation, the picture improved.

Millerchip noted overall inflation is “trending towards low single digits” down from the low-to-mid single digit range of prior quarters.

That’s a meaningful tailwind for real purchasing power, and it supports continued spending without requiring the Fed to move.

However, the management flagged inflation risk: “The situation in the Middle East could impact fuel costs and shipping schedules if there is instability in the region for a sustained period of time.”

Gas prices were down mid-single digits in Q2. If that reverses, the inflation picture changes quickly.

Overall, the transcript highlighted a healthy economy with solid customer spending.

We have a short on Costco.

It’s funny how a growing business can sometimes be a terrible investment.

How do you justify a P/E NTM of 47.0x with single digit revenue growth?

Markets

Time To Leave Oilfield Services

Energy was one of our biggest exposures heading into this week.

It had a solid run since the start of the year.

The setup favored it – Venezuela, Iran, defensive positioning, and reasonable valuations.

‘What can go wrong for this category?’- Everyone started to think the same over the last month.

And, when everyone agrees on an idea, it gets crowded, and that is the best time to exit.

That’s what we did this week.

The OIH was up 43% YTD last week, and it feels like it had ran beyond the fundamentals.

We are now seeing the unwind.

FTI, WFRD, and the entire oilfield services complex broke down this week.

We sold FTI. We love the business. But it feels like the recent run is complete. The stock broke down below its trend.

We highlighted FTI back in our newsletter on 11th Jan. SPY traded at ~6950 compared to 6700 today.

This is what active management looks like in action.

The setup that made oilfield services attractive — under-owned, ignored, with a credible energy demand thesis behind it — is no longer the setup.

Everyone got in. The upside is fully priced.

We’re happy with the gains. We’re moving on.

No One Left To Sell

Markets are mean-reverting hard post-Iran.

The worst-performing decile YTD rallied an average of 4.4% this week.

Every other decile finished in the red, with the best-performing stocks actually falling the most, down 6.1%.

The Iran shock forced institutional deleveraging, and the unwind hit the crowded longs hardest.

Software was the primary beneficiary of this mean reversion.

IGV had already fallen over 22% in the first two months of the year, putting its total decline from peak above 30%.

Citrini’s article marked the bottom in IGV. Investors spent the weekend reading about the death of software at the hands of AI.

Monday the 23rd opened into low liquidity and an exaggerated flush.

IGV has rallied 13.9% since the close on 2/23, trading higher in eight of the last nine sessions — the sixth-longest open-to-close winning streak in the ETF’s history.

The Citrini report, depite its dim intellectual merits, was the sentiment clearing event the category needed.

Maximum bearish narrative plus forced selling plus low liquidity. That’s what bottoms look like.

The AI Apocalypse thesis was always overblown.

Enterprise software doesn’t get disrupted overnight. Workflows are already embedded with SAAS, and switching costs are high.

Management finds a way to integrate AI within their platforms, which turns AI from a disruption threat into a new opportunity.

HubSpot’s earnings proved it. They saw an increase in customers, retention, and average revenue per user by integrating AI within existing products.

We added Hubspot(HUBS), Godaddy (GDDY), and Adobe (ADBE) in the prior weeks.

The thesis was simple: high-quality businesses with durable earnings, trading at valuations that had fully priced in an apocalypse that wasn’t coming.

The markets seems to be realizing the thesis.

HUBS was up double digits. The broader cohort followed.

We’re staying in our positions.

The earnings are there. The valuations are near all-time lows.

And the crowd is only now starting to return to a category it abandoned too aggressively.

That’s usually a good place to be.

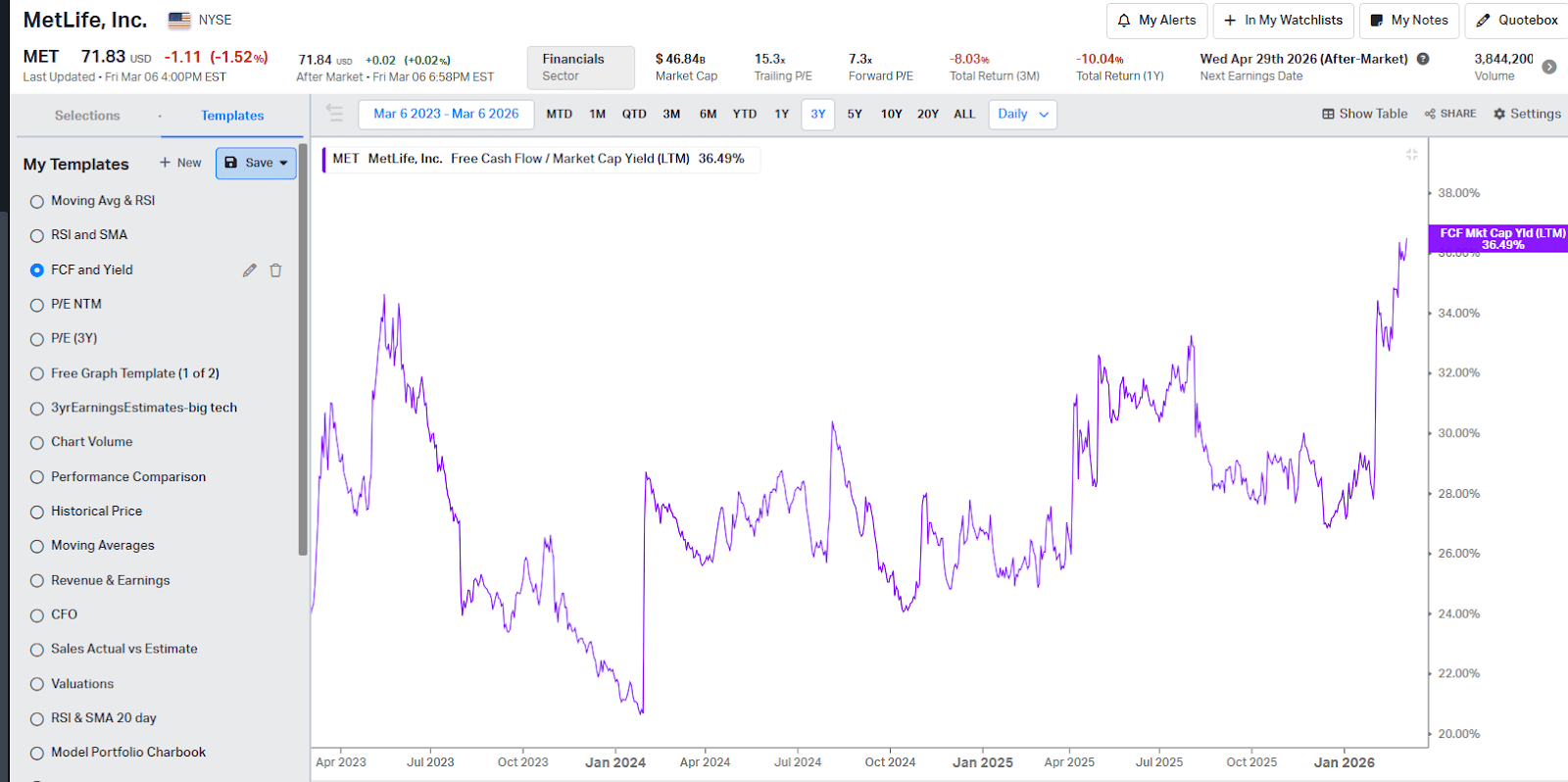

MetLife — Cheap, Cash-Generative, Ignored

MetLife is the anti-theme stock we’re considering this weekend.

It is one of the largest insurers in the world, providing services across the US, Asia, Latin America, and EMEA.

MetLife trades at a FCF yield of 36.5%, at highest levels of 3Y history, and leading peers.

Forward P/E is 7.3x, which has compressed from its usual 8.5x level.

We believe buying real businesses like this is what you want to do in an environment like this.

Q4 earnings were solid. Adjusted EPS came in at $2.58, up 24% year over year — the strongest single quarter in recent history.

The business is executing. Revenue growth, expense control, and higher variable investment income all contributed.

Across geographies, EMEA earnings grew 64% YoY. Latin America was up 13%.

The capital return picture is equally compelling.

MetLife repurchased $2.9B of stock in 2025 and paid $1.5B in dividends — a combined shareholder yield of roughly 11%.

The dividend alone yields 3.16% with a sustainable 50% payout ratio and a 5-year CAGR of 4.3%.

The stock is down 10% over the last year despite decent fundamental performance.

That disconnect — between earnings delivery and price action — is the setup.

The risk?

Insurance earnings are sensitive to interest rates, equity market volatility, and derivative mark-to-market swings.

Q4 net income was clipped by derivative losses from rising rates, even as the adjusted earnings picture was clean.

But at 7.3x forward earnings and a 36% free cash flow yield, the market is pricing in a lot of bad outcomes that haven’t materialized.

We still plan on researching it further – especially the balance sheet and how sensitive it is to rates.

But, we like it here from a ‘buy and research further’ perspective.

Oil and The Geopolitical Spike

Oil is trading four standard deviations above its 50-day moving average — the most overbought reading since 1985.

These levels suggest we are closer to a mean reversion today than we were yesterday.

Every prior instance of this extreme move in oil has been followed by weakness over the next six months, with an average six month drop of 15%.

Any drop in oil here would be good news for markets.

We are now trading in a deep fear territory. The VIX spread confirms the panic.

It is in the same territory as the tariff crash in early 2025 and the AI worries spike last fall.

Both resolved into rallies within days.

But, with geopolitical conflicts, we have a lot more moving parts.

An extension in the conflict can mean the market’s bottom is still some time ahead.

Here’s how markets have performed previously with geopolitical tensions.

The recent mentions on this list suggest we are close to a bottom here.

THE S&P: Magical or No?

A lot of discussion on how the S&P is only down a few points from ATHs despite violent rotations under the surface.

Here’s the thing…

The Materials and Staples categories moved into bubble territory to achieve that outcome.

And that support is no longer there as their safe haven status was lost on Friday.

The point is if you think the S&P is a magical index you are mistaken.

What you had was the ‘hot ball of money’ – a term I see increasingly used on X along with Non-Consensus – flood into Staples and Materials.

That’s a temporary phenomenon.

Take a look at the attached valuation multiples for the XLP ETF and XLB ETF.

See how they are trading in their all-time high range.

The trade is crowded, and we might see an unwinding here. This will reflect in the index’s performance.

Lumida Curations

Software Selloff or Buying Opportunity?

Wedbush’s Dan Ives argues the recent market selloff has indiscriminately punished software stocks, creating potential long-term buying opportunities in names like Microsoft, CrowdStrike, and Salesforce for investors with a multi-year horizon.

The Energy Race Powering the AI Boom

The surge in data centers and AI infrastructure is igniting a massive energy demand cycle, where even small breakthroughs in batteries, geothermal, or nuclear efficiency could create billion-dollar opportunities.

The $1 Trillion AI Question

While AI narratives dominate headlines, the discussion highlights a contrast between real capital flows in private credit and the still-speculative assumptions behind trillion-dollar AI forecasts.

Meme

Not Subscribed Yet? Don’t miss out on future insights—subscribe to the newsletter now!

For real-time updates, follow us on:

X | Telegram | Youtube | TikTok | News | Ram’s X | Lumida Health | Lumida Tax

As Featured In

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.

1

2