JPM Dimon's 10,000 Words

Presented by

CLOSING BELL

Happy Monday

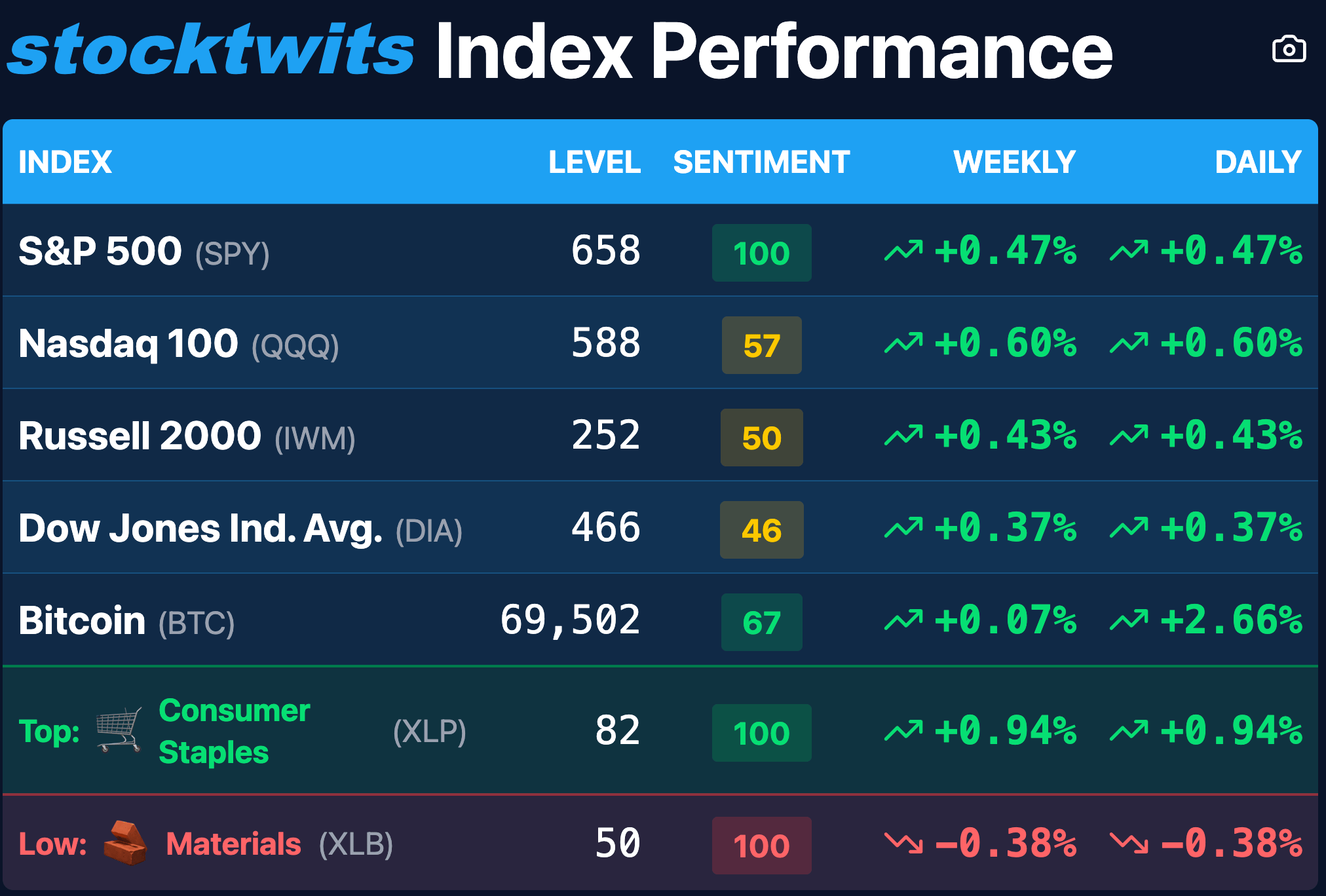

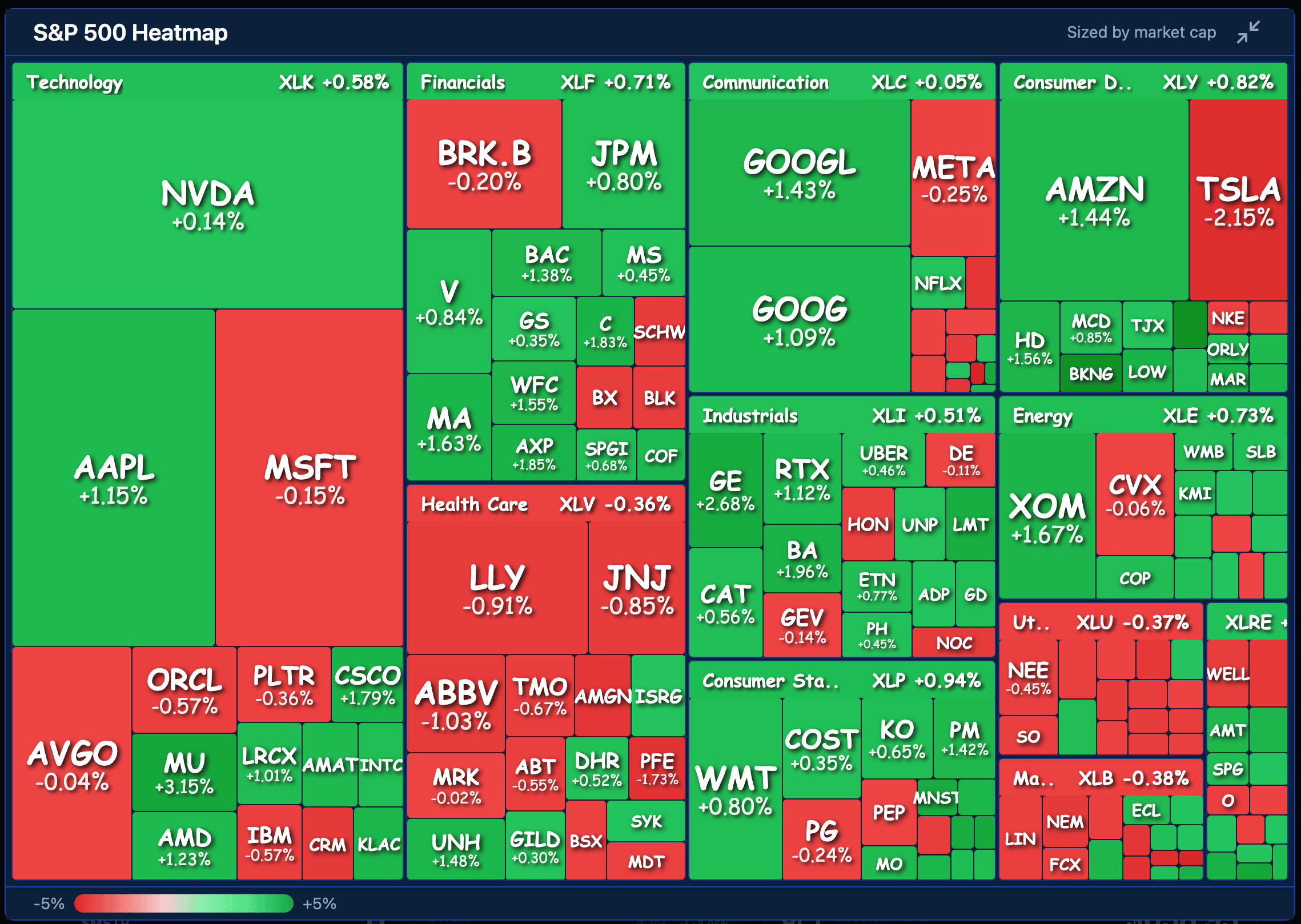

The market climbed Monday, most sectors in the green as the world watched the incoming end of the Iran ceasefire, the moonshot mission reaching its apex tonight, and the incoming start of earnings season. Earnings ‘officially’ start with the largest banks next week, but Wednesday’s Delta report is my personal pick for when the next season starts.

The Artemis II spacecraft will circle the dark side of the moon tonight, already breaking the record for furthest distance away from the earth last set by the Apollo 13 crew, at 248,655 miles from Earth.

The President spoke late in the Monday trading session, talking about Iran at a press conference just past 1pm ET, after posting some insane tweets over the weekend. Trump pledged to destroy Iran in one day if they do not agree to a ceasefire and open the Strait of Hormuz, though he has been back and forth on whether he admits the world needs the strait open.

JPMorgan analysts said in a note that gas prices could hit $5 if the strait does not open by mid-April, which is rapidly approaching time of a week from now.

Trump also said he would jail journalists that reported the rescue mission of two downed airmen in Iran that took place successfully over the weekend. Citrini Research, a bear call firm, claimed they sent an analyst to the strait with a smuggled high-zoom camera to capture about 15 ships moving through the waterway a day. You can’t believe everything you read online.

In big-picture market news, JPMorgan Chase’ CEO Jamie Dimon released his annual report on the last year of the market. It is a preview of the themes he will describe in the bank’s most recent quarter next week, and a top notch report of overall market conditions the world faces today. He said there might be a skunk at the party. 🦨

Refer a Friend:

Does this newsletter help you? Want to return the Fave? The best way to help the Daily Rip is to tell your friends and family about us! Share with a simple click below, and receive a free copy of our first quarterly edition of the Daily Rip Equity Forecast! This is sell-side research on how the Daily Rip audience is positioning themselves in the market this quarter. Look out for a questionnaire on your thoughts as we enter Q2!

MACRO

Jamie Dimon Sees the Tectonic Plates Shifting and Wrote 10,000 Words About It

The JPMorgan Chase chairman dropped his annual letter to shareholders on Sunday, April 5, and while the headlines are genuinely impressive, the real story is Dimon using the platform to warn that the risks facing the global economy in 2026 is unlike anything he has seen in years.

The RIP: JPMorgan Chase generated record revenue of $185.6B in 2025, its eighth consecutive year of record revenue; net income $57B; quarterly dividend was raised twice in 2025, now $1.50 per share; extended $3.3T in credit and capital to clients; the bank moves nearly $12T daily across 120+ currencies; Dimon sees hyperscaler AI capex estimated at $725B in 2026, up from $450B in 2025.

Dimon’s core warning is stagflation, framed as the “skunk at the party.”

“The skunk at the party — and it could happen in 2026 — would be inflation slowly going up, as opposed to slowly going down,” Dimon wrote. “This alone could cause interest rates to rise and asset prices to drop. Interest rates are like gravity to almost all asset prices. And falling asset prices at one point can change sentiment rapidly and cause a flight to cash.”

Inflation is one of many major themes, most notably armed conflicts in Ukraine and Iran, Dimon wrote.

He said that household net worth as a percentage of GDP at 560% is well above the 460% peak during the housing bubble of 2006, meaning a sentiment shift could be particularly violent.

On private credit he said actual losses are already running slightly higher than the environment warrants and that not everyone who entered the space late will be good at credit underwriting. Holders of $BX, $APO, $KKR, and $OWL should read that section carefully given the themes behind the Blue Owl redemption crisis. Dimon’s letter is the single best annual macro briefing available for free and the section on AI, banking regulation, and European economic decline alone is worth the read. 📋

SPONSORED BY MOBIX LABS

Mobix Labs Secures 5x Order Surge for F-22 Raptor Program

Mobix Labs (Nasdaq: MOBX) is hitting a new altitude in defense tech. The company just announced a massive expansion of its role in the F-22 Raptor program, securing new and increased orders that represent a five-fold jump over previous activity.

As modern fighter jets become more electronically complex, Mobix Labs provides the specialized filtered connectors essential for shielding sensitive onboard systems from electromagnetic interference. With production already underway and shipments slated for 2026, Mobix is proving its tech is the backbone of U.S. air dominance. From stealth fighters to anti-drone systems, they are the high-reliability partner of choice.

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

INDUSTRY NEWS

Medicare Just Gave Managed Care a $13 Billion Surprise 🤕

The Centers for Medicare and Medicaid Services finalized a +2.48% Medicare Advantage rate increase for 2027 on Sunday, a number that came in well above the near-flat rates proposed in January. The good news sent the managed care sector surging after hours as investors who had been bracing for pain got relief instead.

The RIP: CMS final 2027 Medicare Advantage rate increase +2.48%; expected to generate $13B in additional payments to Medicare plans; Stocks like $UNH ( ▲ 1.48% ) $HUM ( ▲ 2.71% ) $CVS ( ▼ 0.29% ) all climbed after hours. JPMorgan analysts wrote March 23 that investors expected at least +1 percentage point improvement over the January proposal; TD Cowen wrote March 30 that +1 to +1.5 percentage points would be “good enough”.

The January proposal had spooked the entire managed care sector by holding rates near flat while medical costs kept rising, essentially threatening to squeeze margins industrywide. Insurers lobbied aggressively for a bigger increase and they must have won out. The practical implication for retail holders of $UNH, $HUM, and $CVS is that the single biggest uncertainty hanging over earnings for 2027 just got resolved in the sector’s favor.

$OSCR ( ▲ 7.05% ) and $MOH ( ▲ 2.86% ) also carry the same Medicare Advantage tailwind with smaller floats and saw more volatile reactions, making them the names most likely to see outsized retail momentum Monday morning. 🏥

TRENDING STOCKS

Pops & Drops

-

$MSTR ( ▲ 6.56% ) Strategy: surged +7% after Bitcoin climbed above $69,000 on ceasefire optimism

-

$ENVX ( ▲ 13.64% ) Enovix: ripped +14% after next-gen silicon battery momentum caught the AI device trade

-

$CAR ( ▲ 11.65% ) Avis Budget: surged +12% after oil pullback on Iran ceasefire signals lifted travel names

-

$WEN ( ▲ 3.05% ) Wendy’s: climbed +3% after Trian Fund filed a 13D amendment signaling possible acquisition

-

$PGY ( ▲ 3.14% ) Pagaya: climbed +3% after AI lending fintech names caught a broad relief bid

-

$VRSN ( ▲ 5.64% ) Verisign: popped +6% after Citi raised price target to $295 ahead of April 23 earnings

-

$STX ( ▲ 5.58% ) Seagate: popped +6% after memory reversal extended into storage names

-

$MPWR ( ▲ 5.5% ) Monolithic Power: gained +6% after AI power delivery demand kept chip names bid

-

$BKNG ( ▲ 5.02% ) Booking: climbed +5% after oil pullback and ceasefire optimism lifted travel names

-

$TSLA ( ▼ 2.16% ) Tesla: fell -2% as Q1 delivery miss hangover continued into Monday

WHAT’S ON DECK

Tomorrow’s Top Things 📋

Macro: ADP Employment Change Weekly (8:15 AM ET), Durable Goods Orders (MoM) (Feb) + Core (8:30 AM ET), Atlanta Fed GDPNow (Q1) (10:00 AM ET), 3-Year Note Auction (1:00 PM ET), API Weekly Crude Oil Stock (4:30 PM ET), +1 more. 📊

Pre-Market Earnings: $NNOX, $SPCB, $IQST iQSTEL. ☀️

After-Market Earnings: $PACB Pacific Biosciences Of California, $AEHR Aehr Test Systems, $DBGI Digital Brands Group Inc, $IMTE Integrated Media Technology Limited, $LEVI Levi Strauss, +2 more. 🌙

P.S. You can listen to all of these earnings calls on Stocktwits.

Links That Don’t Suck 🌐

📈 Join IBD Live to watch and discuss the market action with top market analysts*

🤑 FDA approves weight loss pill from Eli Lilly

💰️ Treasury taps BNY and Robinhood to run Trump Accounts for kids

📺️ Trump’s many threats of possible war crimes reach a crescendo in Iran

👀 Epstein files: Commerce Secretary Howard Lutnick set for May 6 interview by House Oversight

*3rd Party Ad. Not an offer or recommendation by Stocktwits. See disclosure here.

Get In Touch 📬

Want to see some change? Email Kevin Travers feedback, follow him on Stocktwits. Refer a friend for this quarter’s edition of The RIP Forecast!

Terms & Conditions 📝

Securities Disclaimer: STOCKTWITS IS NOT A TAX ADVISOR, BROKER, FINANCIAL ADVISOR OR INVESTMENT ADVISOR. THE SERVICE IS NOT INTENDED TO PROVIDE TAX, LEGAL, FINANCIAL OR INVESTMENT ADVICE, AND NOTHING ON THE SERVICE SHOULD BE CONSTRUED AS AN OFFER TO SELL, A SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION FOR ANY SECURITY. Trading in such securities can result in immediate and substantial losses of the capital invested. You should only invest risk capital and not capital required for other purposes. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should also consult an attorney or tax professional regarding your specific legal or tax situation. The content is to be used for informational and entertainment purposes only and the service does not provide investment advice for any individual. Stocktwits, its affiliates and partners specifically disclaim any and all liability or loss arising out of any action taken in reliance on content, including but not limited to market value or other loss on the sale or purchase of any company, property, product, service, security, instrument, or any other matter. You understand that an investment in any security is subject to a number of risks and that discussions of any security published on the Service will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which content is published on the service have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information. Read the full terms & conditions here. 🔍

Author Disclosure: The author of this newsletter does not hold positions in any of the securities or assets mentioned. 📋