AGI is Coming (Nvidia Conf); Fed Watch

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

-

Macro: Rate Cuts?, Recession?, AI Proof Assets?

-

Markets: NVDA Bubble, MSFT Co-Pilot, TSLA & Goldman

-

Company Earnings: Bright Spots in E-com, Athletic & Athleisure

-

AI: NVDA GTC, Blackwell & Omniverse

-

Digital Assets: AI Agents On Chain, Crypto Chartbook

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

This week we had an insightful conversation with Dave Lambert on his Non Consensus approach to venture capital.

Dave is the founder of RSCM Capital and has done over 1800 deals.

Their entry valuations are $2 to $3 MM. That’s unheard of in venture.

They do not exercise their pro-rata.

They take full advantage of QSBS and another obscure part of the tax code.

Their typical fund has 600 deals.

And their performance is top-decile. Better than what you would see at the ‘name brand’ VC funds.

Don’t forget to like, share and subscribe – your support helps us keep growing and booking amazing guests each episode.

In case you missed our last episode with Dr. Adel here are the links below:

Dr. Adel has a Ph.D. in AI/ML/Blockchain and is a serial entrepreneur with three successful exits. We discussed non-consensus opportunities in the AI ecosystem, AGI & AI personhood, applications in blockchain and cybersecurity.

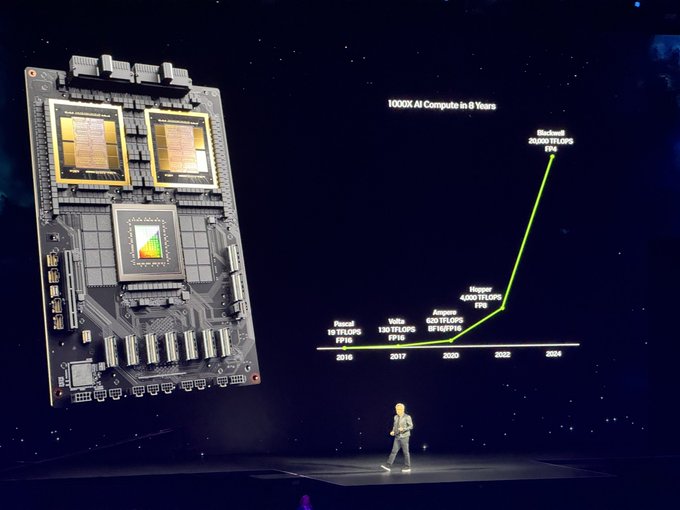

NVIDIA GTC 2024

If Aliens were to descend to earth and and ask for evidence for how far human civilization has advanced, I’m pretty sure we would offer up Nvidia’s new Blackwell platform.

(We might also offer up the US Constitution, the Magna Carta, and a whitepaper called ‘Electronic Peer to Peer Cash’ 🙂)

AI is the dominant theme driving equity markets higher.

AI is the new salvation and it has its prophets – if we stay the course.

We tuned into Nvidia’s GTC Conference earlier this week.

Here are my main takeaways:

-

The “semiconductor cap ex receiver thesis” we advanced last year is still intact.

All technology firms are either ‘cap ex payers’ or ‘cap ex receivers’ in the battle for AI.

The big winners will continue to be the ‘cap ex receivers’.

The Cap Ex receivers are those that receive payment for their services. The CapEx receivers are the classic ‘picks and shovels’ winners in the Gold Rush.

I find AI less than satisfying in day-to-day life. The Application Layer has gaps.

But, that doesn’t really matter for the CapEx Receivers.

That means names like Nvidia.

-

The height of human civilization is the technology and supply chain represented by the latest Nvidia Chip.

Milton Friedman used to joke that the pencil demonstrated the power of specialization.

No one knows how to build a pencil. Each component is the result of specialization and a far flung global supply chain.

That’s especially true of semiconductors.

-

The lead Nvidia has over competitors – including AMD and Intel – is significant.

Markets exhibit a winner-take-most phenomenon. The leader captures the lion’s share of the spoils.

We remain of the view that Nvidia is one of the cleanest ways to bet on AI.

To be sure, there are other names in semiconductors that we expect will do well that we’ve written about: ASML, Broadcom, KLAC, Lam Research, Cadence, Synsopsys, Dell and others.

We do believe betting on Intel and AMD is a mistake… and we’re seeing negative relative strength there.

-

We will see AGI in 5 years.

AGI is the idea that an AI can achieve a super-intelligent like experience.

We moved up our timetable after the Nvidia demo.

The headline is that hardware capability is no longer the constraint. 1 trillion parameter models are coming.

Longer context windows, compute, hardware-based memory, photonics – the hardware side is delivering.

The gap is on the software side.

-

Our view is that AI needs ‘research breakthroughs’ not merely more engineering

Engineering means throwing more hardware at the problem.

That means longer context windows, hardware based memory, throwing the Library of Congress, all the Youtube videos Google has on file, and the WWW at the LLM.

We believe we need to see a research breakthrough on the order of pagerank or the seminal ‘Transformer’ whitepaper to get to AGI.

Today, LLM foundation models are using the equivalent of duct tape to control hallucinations. The duct tape consists of techniques such as RAGS or having nested AI LLM models.

There are researchers working on these problems. We are optimists, and expect they will figure it out.

-

The power demands of GPUs are insatiable. That is going to create demand for (i) nuclear energy (another Lumida thesis called ‘nuclear renaissance) and (ii) grid electrification (a new Lumida theme we are actively researching).

There are many knock-on effects from the rise of AI.

Studying those trends will help identify less expensive ways to bet on AI.

Lumida curated a highlights reel of the best scenes from Jensen’s nearly 2 hour presentation.

We go deeper into the above themes and more in this 30-minute live annotation of Jensen’s remarks.

Macro

Fed Watch:

Three big takeaways from the Fed meeting.

Overall, bullish.

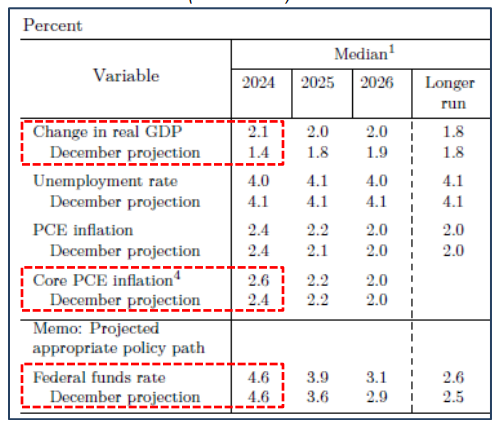

(1) The Fed dot plot shows a higher real GDP projection and higher inflation forecast from December.

And yet, the Fed Funds projection is the same.

So, the Fed expects higher for longer and faster growth – but isn’t willing to raise rates.

(2) Quantitative Tightening is set to taper in May:

Excerpt from Powell:

“We’re talking about going to a lower pace.

I don’t want to give you a specific number because we haven’t made an agreement or a decision, but that’s the idea…

In terms of timing, I would say ‘fairly soon.’ I don’t want to be more specific than that.

You get the idea — this is in our longer-run plans, that we may actually be able to get to a lower level because we would avoid the kind of fictions that can happen. Liquidity is not evenly distributed in the system.

There can be times when, in aggregate, reserves are ample or even abundant, but not in every part.

Those parts where they’re not ample, there can be stress. That can cause you to prematurely stop the process to avoid the stress… Something like that happened in ’19″

(3) 10 members expect 3 rate cuts. 9 expect 2 rate cuts.

I’m in the latter camp.

BAML Global Fund Manager (FM) Survey

Here’s a link to Lumida Wealth’s thread on the monthly BAML Global Fund Manager survey.

I chuckle when I read ‘recession unlikely’. No kidding.

The Economist on America’s Pumped Up Economy

My favorite Consensus indicator says we have a roaring economy.

6 months ago…

The vibe was the exact opposite.

6 months ago was the time to buy aggressively.

Now, we are in ‘buy the dip’ mode.

Will we get a dip?

This is the part of the cycle where the Consensus is mostly right. But, they will screw up the timing of entering anyway and will need to wait a few months for markets to lift their positions.

Markets are overbought. We bought a small cap and a homebuilder this week. I would expect a breather in the next few days based on various indicators we look at.

Note: April is the best month for stock market seasonality. And this is a very strong bull market. I think we are going to blow past Wall Street year-end estimates.

The ‘wall of money’ is mostly offsides. But, it’s worth having a sense of where to focus – where there is value and good entries.

Energy is entering a period of unusually strong seasonality now thru the mid-Summer.

The S&P has a 3% weight on energy. We have closer to an 8% weight. Energy is one of the best sectors this year. We feel good about that.

There will be a pullback at some point – energy should outperform during then. And when that happens we can rotate and pick up semiconductors which are over-extended.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

What asset is AI-Proof and will perform well in an Age of Abundance?

Land.

Land should move up in the years ahead due to 3 factors: (i) AI abundance longer term, (ii) housing shortage, (iii) illegal immigration.

5 MM new immigrants creates a lot of demand for new housing.

The beta on land is higher than you may think. Take a look at our interview with founder of Knight Capital Group, Kenny Pasternak, for more in this clip.

How to get long land? You don’t want to pay property taxes. And how do you get the best land?

Homebuilders.

A homebuilder can easily own $1 Bn+ more in raw land.

And homebuilders make money so you have positive carry instead of property tax bills.

Homebuilders are a cheaper more productive way to own land.

And you can pick homebuilders in your desired market.

I recommend Southeastern United States (NC), FL & TX, maybe AZ.

Seek land near leisure and retirement in low tax states.

Rates are not coming down yet…and homebuilders are growing quickly and spitting out cash.

We bought a homebuilder with a PE ratio that is sub-10x in our desired market.

We are still actively accumulating it, so we’ll share the name in a month or two.

It seems like when we write about an idea here, it gets lifted pretty quickly.

That nuclear utility name is already up 20% in a month or so.

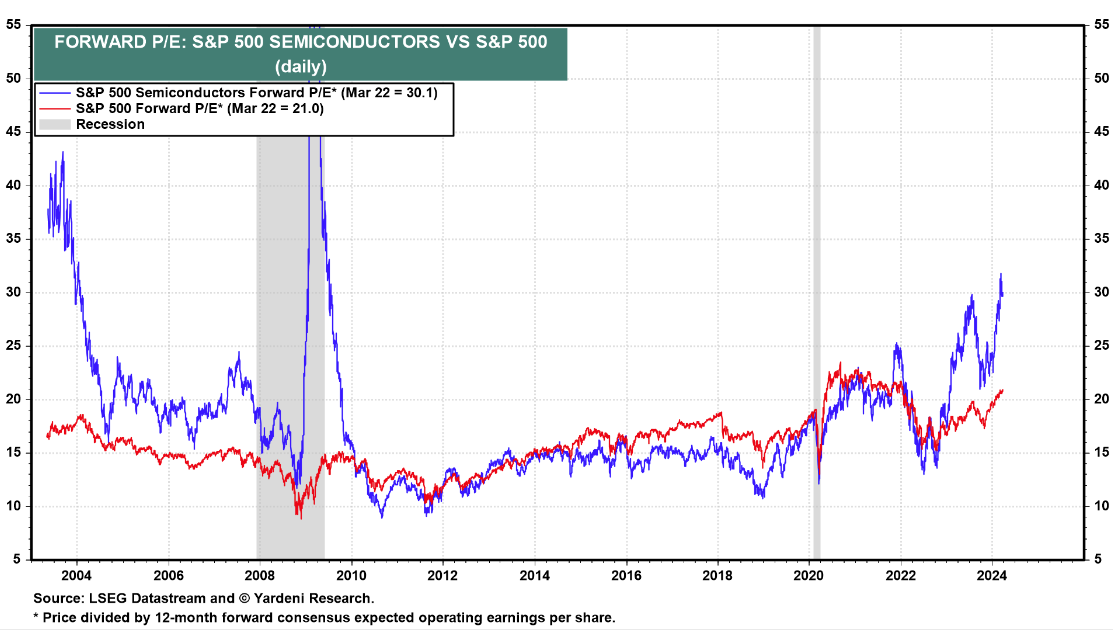

By the way, take a look at semiconductors. The PEs are levitating.

The good news is our portfolio is levitating. The bad news is we can’t deploy new money into that category easily now.

This will mean revert and correct. Names like Intel and AMD we expect will have more downside than the leader Nvidia.

There are still good names out their like Taiwan Semiconductor which have cheaper valuations.

Last summer when we looked at TSMC in this very same newsletter it had a PE ratio of 15x. Now it’s 20x.

It’s still cheap relative to other semi names. You can see the re-rating of semis on the chart below.

Be patient and wait for a good entry – especially on the heels of Nvidia’s feelgood conference.

There will be a red day this week, at least wait for those moments.

China Snapshot:

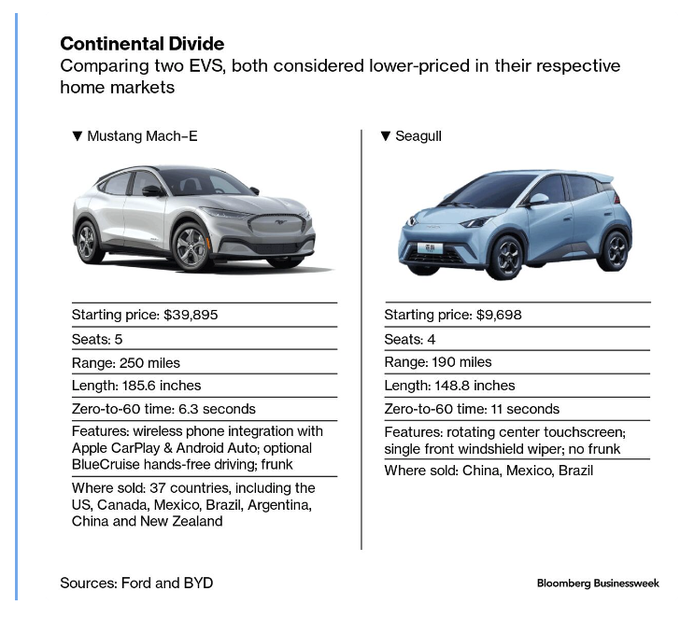

Imagine trying to compete with China in the EV manufacturing game.

Markets:

Is Nvidia a Bubble?

No.

Cathie Woods thinks Nvidia is the next Cisco.

That should tell you all you need to know about why Nvidia is not Consensus.

Most people in their individual accounts do not own even the benchmark weight on Nvidia (4 to 7%).

Is Nvidia short-term overbought? Yes, of course. It’s not an easy stock to get a good entry into.

There are major institutional VWAP orders that explain the steeply sloping line.

Nvidia has a forward PE of 36. It’s cheaper than many other hyped up stocks: Palantir, Tesla, Snowflake, The Trade Desk and many more.

You should ask yourself why do you own any stock that has a forward PE ratio higher than Nvidia.

You have to believe the earnings growth will be higher than Nvidia, or that demand for GPUs will slow.

Nvidia is the ‘pace setter’ in the market.

We only own 1 stock that has a higher forward PE than Nvidia. That’s Cloudflare (NET) which is also indexed to the DataCenter build out theme.

The DataCenter theme is another way to bet on the growth of AI. Many data centers are going online around the world.

Ask yourself which companies are required to execute that vision and you’ll find good names.

We’ve done that exercise and have exposure to what we believe are the best names indexed to the secular trend of datacenters.

Nvidia has good odds of being the most valuable company in the world

It’s happening. Apple and Tesla, two names we are critical of, are descending in value.

Nvidia is now worth more than Amazon.

It’s inevitable that Nvidia will displace Microsoft in our view.

It all comes down to Earnings Growth.

Consider that every Big Tech firm in the Mag 7 is spending money on Nvidia.

The expenses of Big Tech firms are the revenues of Nvidia.

That trend will not change anytime soon because the stakes are too high.

The prize for ‘winning’ the Application Layer is significant.

GPUs are Out-Performing Moore’s Law

Nvidia is out-performing Moore’s Law.

OpenAI’s first Nvidia GPU stack had .17 Petaflops.

We are going from fractions of a Petaflop to Exaflops.

1 Exaflop = 1,000 Petaflops

Today, there are a handful of Exaflop supercomputers globally.

Now Nvidia is selling Exaflop systems.

Two more years and those Exaflop systems will look obsolete.

The main constraint is having enough data to train these massive trillion parameter models.

Imagine an AI trained on all Youtube videos, the library of Congress, and the world wide web.

Who wins that game?

That’s one of the reasons, but not the sole reason, we like Google.

Google has the best odds of birthing AGI and deploying this to consumers.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

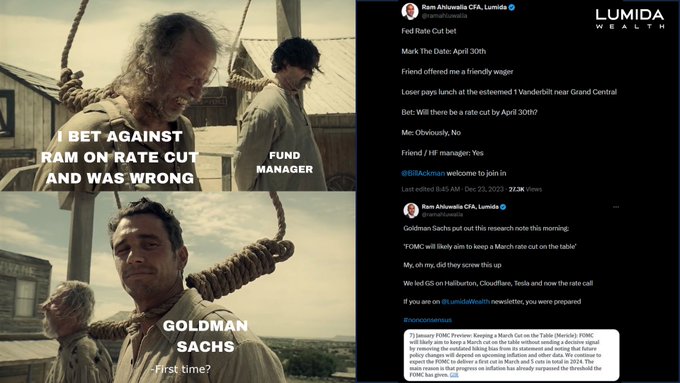

Federal Reserve says no Rate Cuts in March

It feels anti-climactic now, but the Fed has decided not to cut rates in March.

Remember in December when Bill Ackman, Goldman Sachs and others after the December FOMC meeting concluded we’ll see March rate cuts?

CME futures priced in a whopping 80% probability.

We were on the FOMC call and concluded markets had hallucinated. We were very public on Twitter and in our newsletter.

The point is – markets hallucinate just as much as AI. People hear what they want to hear.

And Goldman Sachs is just not as good as they used to be in the late 90s.

We have a funny meme on this below and another video which is a victory lap.

Here’s a link to the FOMC video:

The interest rates futures market is highly liquid. Generally, we prefer over-looked securities where there are discernible inefficiencies.

The rates markets is not that.

Betting against rates would allow you to scale wealth in size without moving markets.

It goes to show that Mr. Market is driven by psychology and story telling first and foremost.

Fundamentals do play a role of course. There’s a reason we shun owning securities that have skyhigh valuations or declining revenue like Apple…

But, psychology is the primary force driving multiple expansion and multiple compression in markets.

And multiple expansion is the primary driver of equity returns.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Tech Exec Testing Microsoft Co-Pilot story

I met with a friend who is a technology executive at a top 3 bank. This is a major, major bank you would recognize. He previously was a Cloud Leader at AI.

He’s one of the best CTOs I know.

Here’s what he said about Microsoft Co-Pilot.

The bank is testing Microsoft Co-Pilot for software development use-cases. Microsoft purports a 50% increase in productivity. The bank sees a 15% increase in productivity

Co-Pilot costs $30 / month. Engineers are expensive. Even a 15% bump in productivity seems like a no-brainer.

The issue is the bank needs representations & warranties from Microsoft that the code generated does not violate IP laws. They want Microsoft to indemnify the bank from accidental use of code that may have originated elsewhere.

The other issue is that Co-Pilot hallucinates. So the bank will not use Co-Pilot on applications related to information security or mission critical applications. Customer service devs are more likely to benefit.

The bank is also buying a bunch of Nvidia H100s themselves. They are going to ‘tune’ existing LLM models offered by open-source providers such as Meta Llama 2 and Hugging Face.

I thought it was insightful. A couple takeaways:

-

Startups are the disproportionate beneficiary of AI

-

Regulated industries are adopting AI at a faster rate than they adopted Cloud

-

However, the up-take and the benefits are not as strong as advertised. There is a real risk of AI Disillusionment, or at the very least lukewarm benefits. We still have a ways to go.

Goldman: ‘Momentum is Working’

Goldman wrote this on Tuesday:

‘…since the dovish pivot at the end of last year, the US momentum factor has generated a 3-month Sharpe ratio of almost 8x — nearly double the risk-adjusted returns for the S&P 500’

That’s outstanding performance from a simple factor.

Momentum is the statistical factor in plain english that translates to ‘What’s winning, keeps winning, what’s losing keeps losing’

A crude but effective way to test whether you have exposure to momentum is whether your asset is above the 200 day MA.

A better way is to look for assets that have relative strength.

We have written a lot about the Momentum factor if you want to search for more on my twitter feed.

The ‘holy grail’ is owning asset that are long momentum, value, and quality all at the same.

Over long periods of time, simply put, these factors perform.

They do experience drawdowns from time to time though. No factor strategy is perfect.

Those three factors are working in this market and it is exactly why Lumida Wealth is outperforming.

The security selection matters…

but the high level factor tilts put the wind behind our back.

The highest level lens is Theme selection (e.g., semis, biotech, aging & longevity, digital assets, etc)

We believe the venn diagram of wealth managers that actually try to do this together has an intersection set of one member.

Why does momentum work?

(1) People under-estimate trend duration (cognitive error)

> Nvidia is a good example right?

(2) Bandwagon effect (human psychology)

Source: Goldman Sachs

Source: Goldman Sachs

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Longer-Term Technicals Remain Bullish

‘Goldman: Downgrades Tesla Today’

That’s little solace for investors that trusted Goldman.

Remember Goldman’s conviction buy on Apple?

Investors rode Tesla stock down based on GS guidance.

Tesla is down 30% YTD and has gone nowhere in 3 years but down.

Goldman and Morgan Stanley are conflicted tech M&A bankers.

Tesla has a forward PE higher than Nvidia and has competition from all sides.

Lumida Wealth has been consistent on this name, I have the receipts for our short call.

We no longer have a position here.

Let’s count now all the times we have been on the other side of Goldman or led Goldman:

1. March Rate cuts

> We said no in Dec. Goldman capitulated in Feb

2. Apple

> Goldman had it as a Conviction Buy

We had it as a Conviction ‘Don’t Own’ then ‘Short’ (no position now)

3. Tesla

> Ditto

4. Cloudflare

> We got in first. GS upgrades a week later.

5. Haliburton.

> We got in first. GS upgrades a week later.

There is zero cherry picking in this list.

This is every heads up match with Goldman full stop, and you can search for those tweets.

Fun Fact: Many Lumida Wealth clients are former GS Private Wealth clients

We do portfolio reviews of new prospect holdings, so I know some of their strategies

In short, they put their clients in ETFs issued by their own sister company (another conflict)

And the ETFs are another layer of fees.

You also can’t tax loss harvest.

The sales pitch is ‘we will charge you excessive fees to have the privilege of investing alongside Goldman partners’

It’s a brand arbitrage.

And across the wealth management space it is generally known that of all the private wealth firms, Goldman is the worst at investment performance.

‘No conflict, no interest’ is a phrase that originated at Goldman.

Ask around.

I have no sympathy for Goldman Sachs, Morgan Stanley, and JP Morgan.

Break thru the Matrix.

Equity Factor Rotation: What’s Working?

Take a look at the sharp number of factors that worked in 2023 and flipped this year (Volatility, Size, Momentum, Growth).

One factor worked well in both regimes: Value.

The factor combo we see this year is actually more sustainable longer-term.

Last year, heavily shorted and highly volatile stocks outperformed.

That’s not happening anymore on average.

This is a value, momentum, quality regime.

On the first week of January I shared that tech stocks were at a 99%-ile valuations

S&P is beating tech

Midcaps are beating tech

Energy is beating tech

How are you positioned?

We still own tech to be sure…

The themes within tech matter.

And security selection matters.

Snowflake, Palantir, and scores of others have a higher forward PE than Nvidia.

Does that make sense to you?

I don’t want to own QQQ. Can do better…

Company Earnings

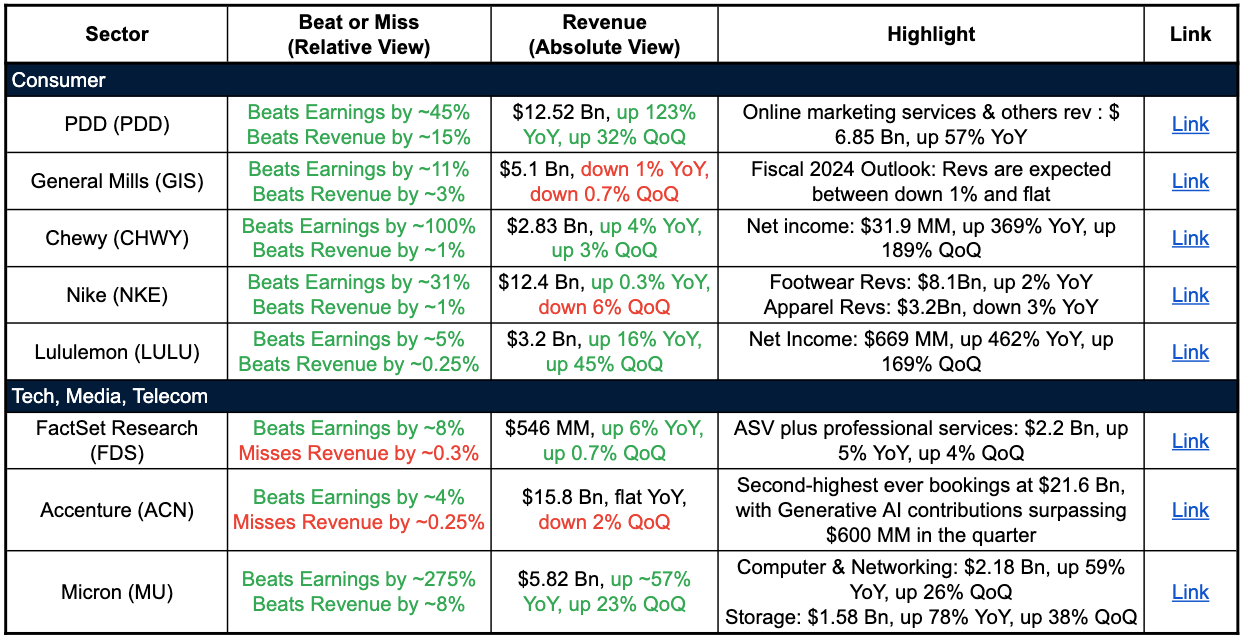

Consumer:

-

E-commerce platforms like Pinduoduo (PDD) in China continuing to see explosive revenue growth driven by online marketing services

-

Consumer packaged goods companies like General Mills facing topline pressure as higher prices impact volumes, guiding for flattish revenue outlook in 2024

-

Pet e-commerce player Chewy delivering modest revenue gains but regaining profitability as cost discipline improves

-

Nike navigating demand shifts across product categories, apparel growth declines

-

Athleisure brand Lululemon maintaining strong double-digit revenue growth and margin expansion from pricing power

TMT:

-

Financial data/analytics providers like FactSet posting steady growth in annual subscription value (ASV)

-

Accenture benefitting from robust enterprise demand for digital/cloud transformation in Gen AI world

-

Semiconductor companies like Micron seeing cyclical upswing driven by memory & storage demand across data center & networking

Overall, the consumer landscape is mixed with e-commerce, athletic & athleisure being relative bright spots while CPG faces pricing & volume challenges. In tech, digital transformation demand remains healthy, Semiconductor upcycle continues gaining steam.

AI

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

5 things you need to know from NVIDIA GTC:

– $1T Data centers revamp

– Blackwell: AI Superchip, 200 B transistors

– NIMs: RAG for your data on any LLM

– NIMs, NeMo & DGx Cloud : $NVDA AI Foundry

– Omniverse – Robotics Digital Twin Platform

Digital Assets

Crypto x AI: AI Agents On-Chain

How do we tokenize robots on chain?!

More seriously, there is an opportunity to tokenize AI agent as a service on-chain.

There’s a variety of protocols that offer decentralized compute on demand.

And discussion of machine-to-machine transactions on-chain.

AI Agents that compute m, and store data on-chain, and are compensated via a utility token makes a lot of sense.

The Agent AIs would be backed by stakers who commit to providing energy and compute resources in exchange for sharing in the proceeds.

These AI agents would be highly specialized.

AI microservice agents.

An AI that manages a liquidity pool on Uniswap-v[x] is one example.

An AI that manages the borrow / lend rate is another.

Those are the more prosaic examples.

Trader AI bots are another.

What other niche AI use application layer use-cases should we expect?

The desire for privacy and security should create a market here.

Which chains are best positioned for it?

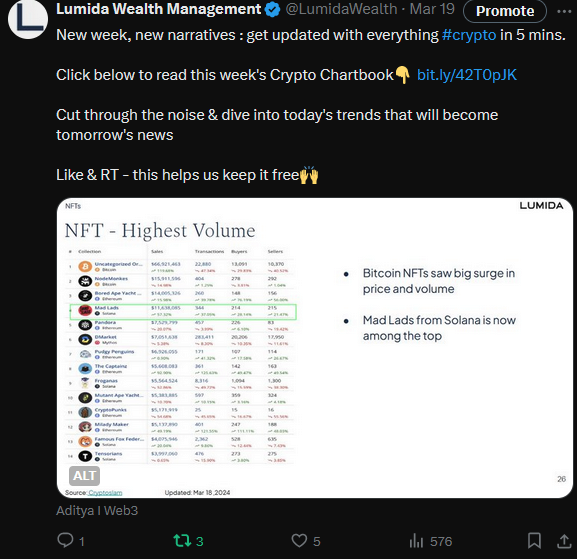

Latest from Lumida Crypto Chartbook

If you missed our Crypto chartbook updates on the social media check out this link.

Every week we update the commentary to cut through the noise and provide the market overview in 5 minutes or less.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Quote of the Week

“Go for a business that any idiot can run – because sooner or later any idiot probably is going to be running it.”

― Peter Lynch

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.