Election Volatility, Tesla, Google & Microsoft

Tesla Cyber Truck

Due Diligence: My experience with Tesla cyber truck and FSD.

When you drive the car live, you discover ‘Panic Mode’

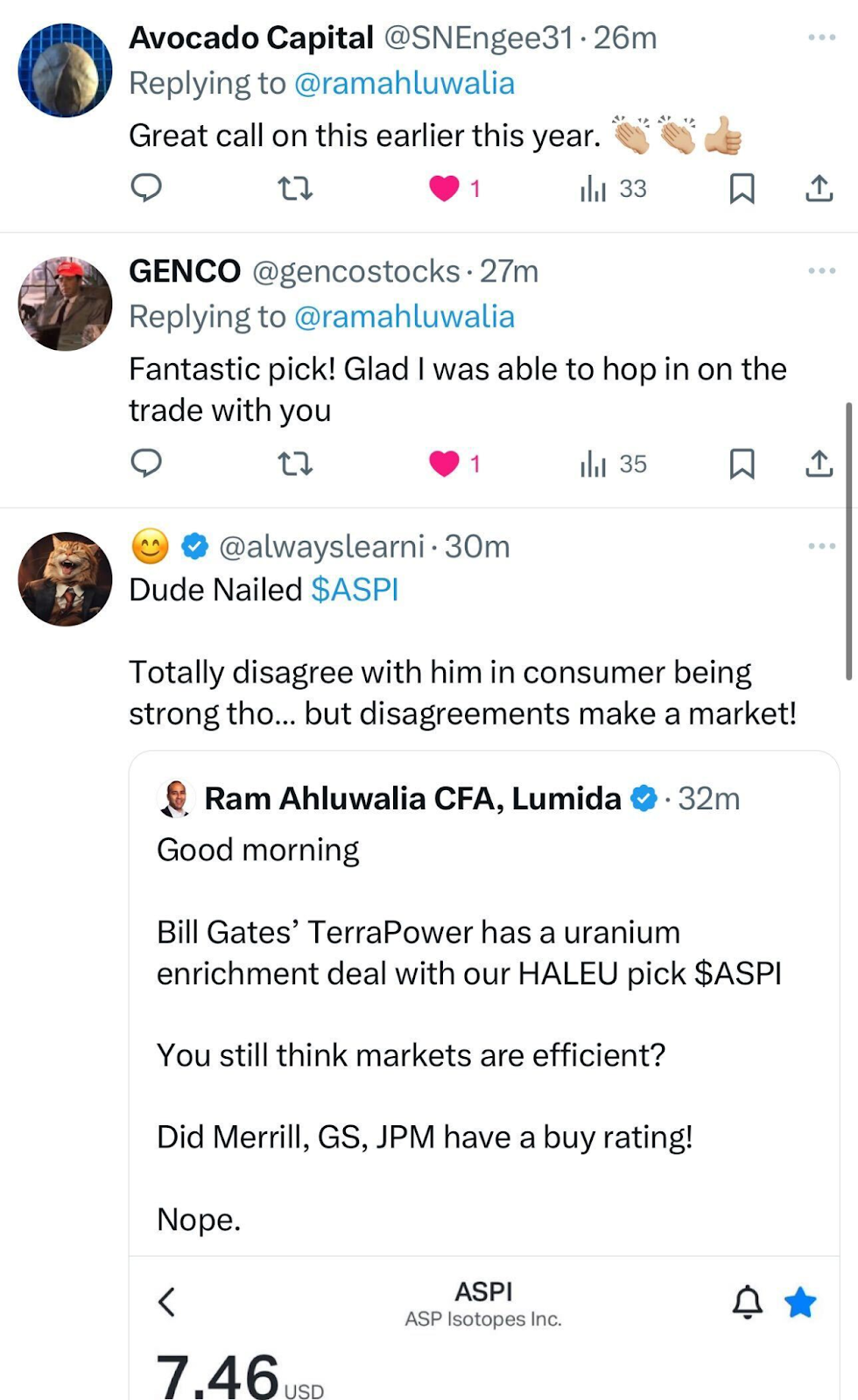

Our take on ASPI

We are getting a lot of recognition on our ASPI call.

Bill Gates small modular reactor play, TerraPower, is apparently executing a commercial agreement with ASPI.

This was a name that none of the wealth managers were covering.

In fact, only 1 no-name company has sell side research on it.

One day, we will do a deep-dive on how we found and diligenced ASPI. Spent more time on this name than anything else this year.

Non-Consensus Investing

There is an annual investing conference in NYC called the IRA Sohn conference.

This past year they picked ASML. That was near the local top for the stock, and the name is below the date of that event. (We used to own ASML, back in the day.)

The fact is ASPI would logically have been the best pick of the year. It has returned multiples – what you’d expect from a VC over 8 years.

Except, the fact that it was Non-Consensus is the reason why it did well – and why Ira Sohn judges would never pick the stock.

Do you see the irony?

It’s like that scene from The Matrix where Neo meets the Oracle in the kitchen…

Markets

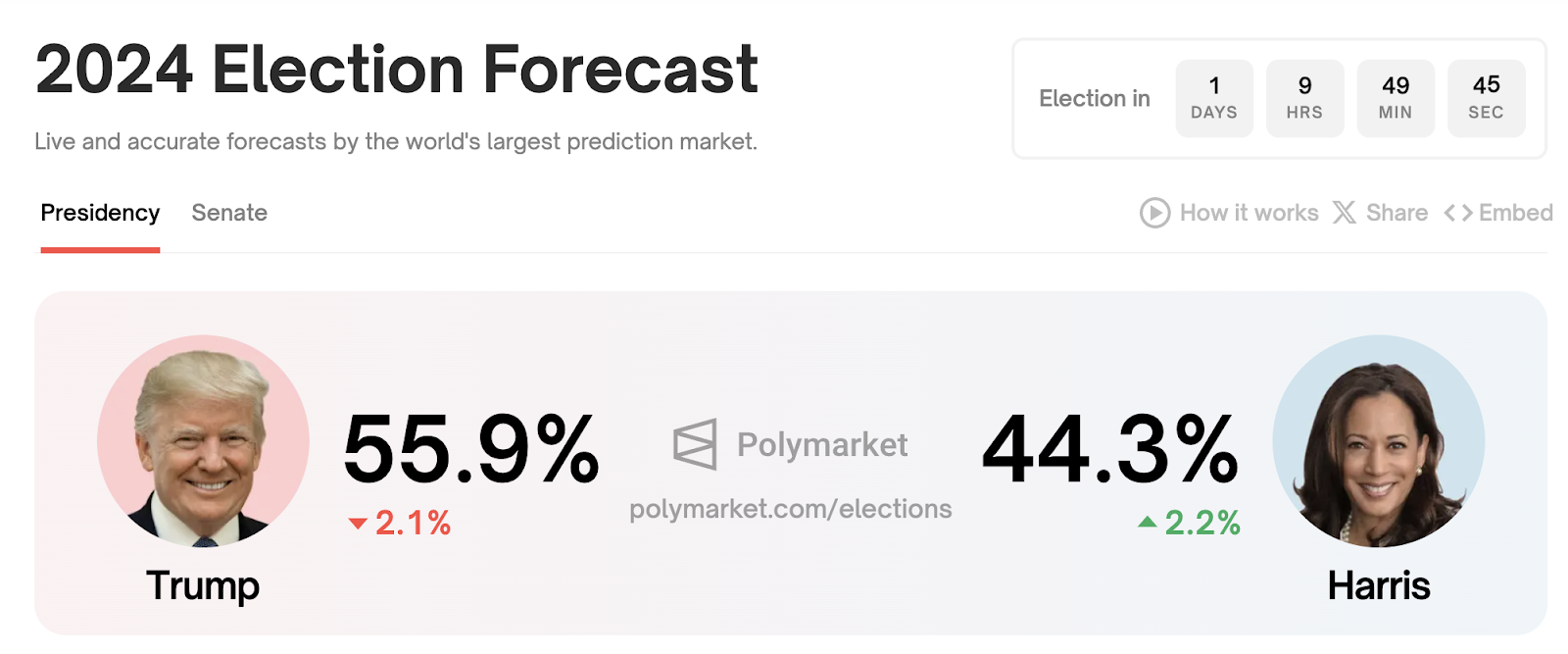

We have a major Presidential election this week. As we noted earlier in the year, there is a ‘Trump Bump’ effect pervading markets.

You can see it in the performance of various industry groups that stand to benefit (e.g., financials) or sectors that are hurt (e.g., clean energy).

You can also see it in the meme coin DJT which is worth $6 Bn despite making less than $4 MM in revenue and losing $370 MM this year.

However, we are seeing a pullback on the Trump Bump on Polymarket, in DJT, and in the equity markets themselves.

In the short-run, markets are driven by positioning and incoming news flow.

If V.P. Harris wins, I would expect a 5 to 10% pullback driven by Mr. Market positioned wrongway plus the prospect of higher expected corporate taxes should create a 5 to 10% swoon in markets.

Speaking of higher taxes, Lumida has launched a Tax Shield product here. Reach out to marc@lumida.com if you’d like to learn more. The strategy is designed to shied investors from short-term and long-term capital gains while keeping them invested in US equities. It’s clever.

Financials would be hurt the most as they have priced in lower capital requirements.

However, that would create a drip worth buying. I would also expect clean energy names like First Solar to do well.

If Trump wins, I’d expect small caps, financials, and any Mag 5 name subject to Anti-Trust to rally. Worth noting, however, that markets have front-run a Trump win so the upside may be limited here.

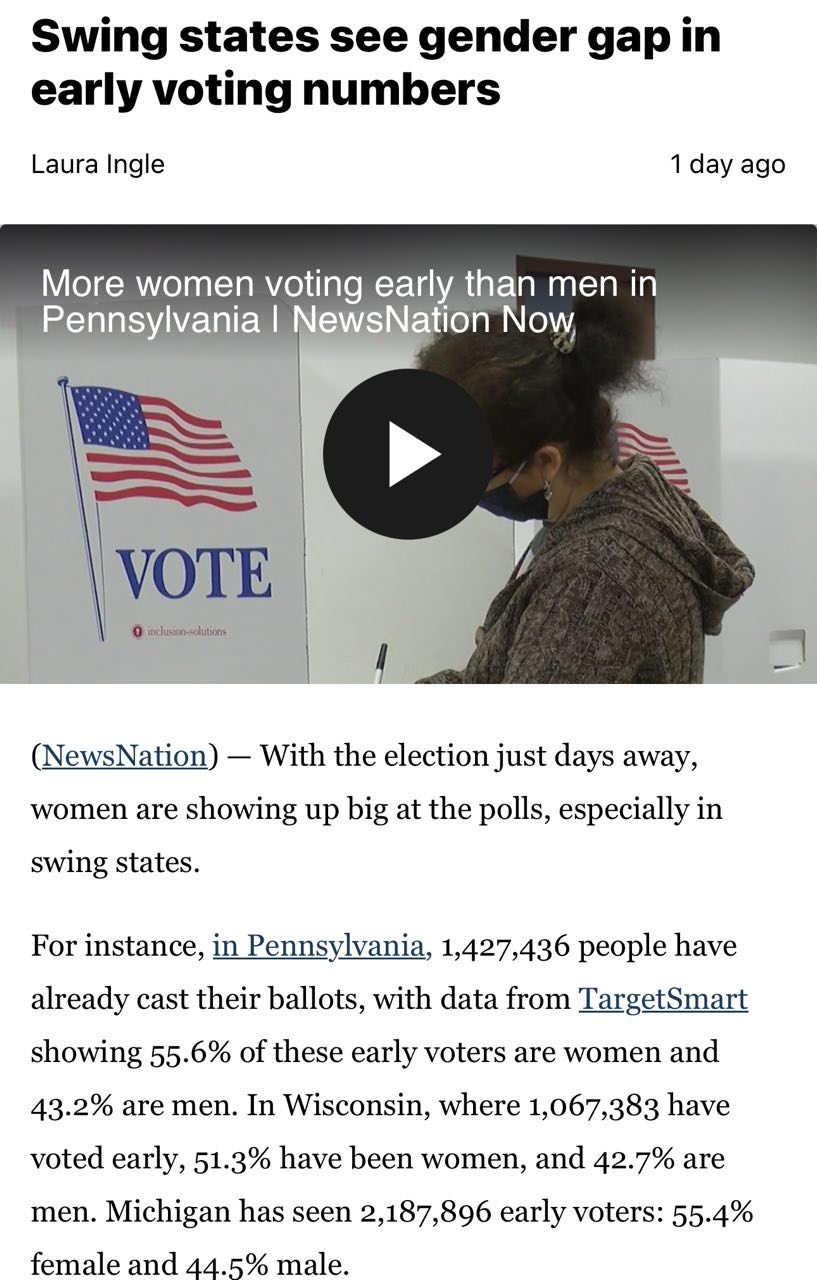

Early voting also shows strong female turnout which presumably favors Harris and creates volatility.

It’s better to reduce risk and react rather than predict on an outcome that is highly studied by people with loads of data. There’s no inefficiency there. Wait for another card to turn.

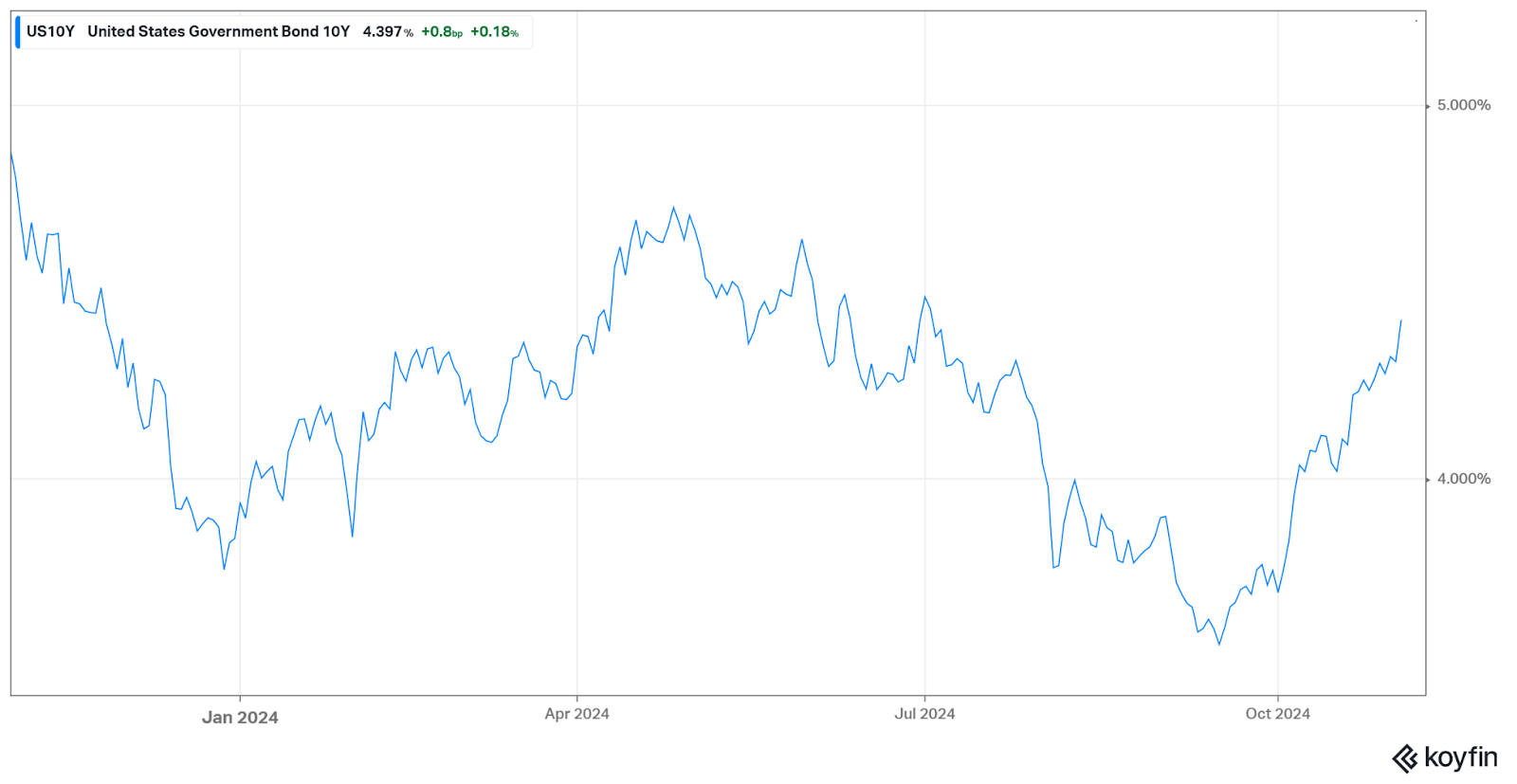

The 10-Year is On the Rise

We noted that after the Fed cut rates 50 bps, the 10-year has been on the rise along with mortgage rates, due to the Fed accidentally tightening.

The ‘bond vigilantes’ like Druckenmiller are out.

When the 10-year is rising, bonds create an attractive alternative to owning equities.

A rising 10-year is a headwind to US equities.

Why? The discount rate on the long-term stream of cashflows is higher as the 10-year goes higher.

We saw the effect of a rising 10-year on mortgage rates which punished homebuilders.

We believe the 10-year is in the final states of making a push higher.

It’s hard to know when it finishes – you just have to wait.

The Trump bump is consistent with a rising 10-year as Trump’s policies are more inflationary.

If Harris wins, you should also expect a tightening on lower nominal growth expectations and an initial risk-off response.

Clarity on election we believe will determine when the 10-year hits its peak.

Thematic Markets Are In Retreat

We noted this year that markets are unusually thematic.

The AI Theme is the primary driver. Initially it was led by Microsoft, now it is led by Nvidia.

Microsoft reported and is below the 200 DMA. The AI theme is softening – and that’s also shown in the semiconductor ETF (‘SMH’)

Microsoft:

Semiconductors are entering their most positive month of seasonality.

They are also not leading the market as they are below their highs.

Notably, semiconductors topped out recently on the day Taiwan Semiconductor reported earnings – that’s called a Peak Sentiment top.

It does look like TSMC is over-owned. And, indeed, that’s the sense we get looking at quite a few sectors.

Taiwan Semiconductor:

The other major theme is GLP1s. Both Novo Nordisk and Eli Lilly are back to levels not seen in several quarters.

Novo Nordisk is below its 200 day moving average, and Lilly is at the 200 DMA.

Novo Nordisk:

This is the second major theme showing weakness.

The third major theme is Defense stocks. After the tragic events of October 7th, the Defense ETF and its leaders went on a tear.

Now, the ETF has broken below its moving average and failed to bounce.

Homebuilders have pulled back – in our view due to high mortgage rates as we called out this risk 2 weeks ago:

Similarly, interest sensitive REITs have pulled back due to higher interest rates. They have also breached key technical levels and remain well above the 200 day moving average.

XLRE:

You also have names in the REIT index linked to AI that are wildly over-valued.

The momentum ETF (which captures a lof of the above themes) is also pulling back.

An ETF consisting of the most popular widely held retail stocks is pulling back.

Utilities are showing initial softness. You may recall we sold our utility stocks about two weeks ago.

Take a look at XLU breaking thru its moving averages:

There’s also news that the US regulator is not allowing independent power producer Talen Energy to fulfill its deal to Amazon.

That will pour cold water on utilities next week and we believe confirms a local top in this sector which has substantially out-run the S&P.

Incidentally, we called Talen Energy as our first utility pick sometime in February when the stock was in the 60s. Now the stock is $173 (an incredible run).

We recommend non-taxable investors sell Talen energy. US regulators are not permitting a deal between Talen Energy and Amazon to take place.

This should hurt the utilities sector also.

Talen Energy:

What we see is a patter of over-crowded themes retreating.

Markets are over-positioned into popular themes. This concept of over-positioning can seem like a contraditction because for every buyer there is a matching seller.

So, who is selling?

This guy: Warren Buffett. (Well, ‘smart money’ more generally).

We noted in a prior newsletter that Buffett usually leads market tops by a year. He’s been building cash for 6 months or so now.

A lot of conservative investors follow Buffett.

(Investors care more about what Warren Buffett has to say than, say, the All In Pod who has hosts that have been incorrectly calling for a recession for two years.)

What happens at a market bottom is that the investor who have the best insight into the name and most conviction own the stock, at a market top the weakest hands and momentum chasers own the stock.

But, these factors – political, rates, and crowdedness – are weighing on markets.

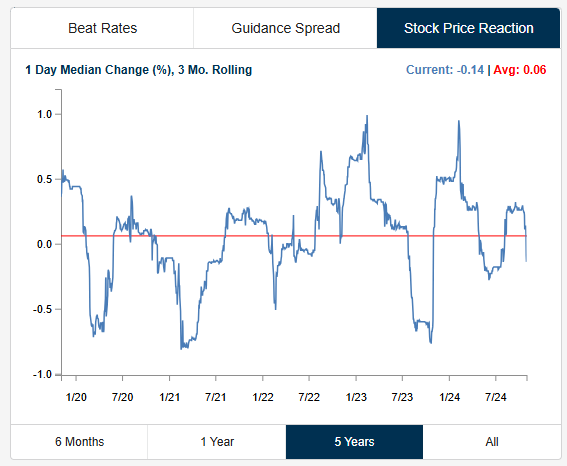

We are seeing negative stock price reactions on earnings as the pace or revenue and earnings beats comes in slower than prior quarters

All of this suggests a continued rotation.

We have talked about the Growth to Value rotation. That is still happening.

Another rotation we expect to see soon is towards international value (more later).

The sector we like the most now is healthcare. Regular readers will know we have been stalking this category for a while.

The sector sold off due to leaders like Lilly and Novo Nordisk (GLP1 theme) facing competiton. Also, Medicare Advantage insurers sold off on higher expenses.

But, the whole category – including healthcare providers, medical devices, and pharma – sold off- which doesn’t make sense.

In fact, these three categories benefit from higher healthcare spend.

Healthcare had a small campfire turn into a forest fire. Now we go pick up bargains.

The category has just bounced off its 200 day moving average. We could get a re-test.

Names we like:

-

DaVita (DVA): kidney dialysis leader with a 13x forward PE

-

Tenet Healthcare (THC) and HCA: healtcare providers with good valuations and earnings growth

-

Cigna Health: an insurer exiting Medicare advantage with ~8% in buybacks and a 10x forward PE. (Cigna is much cheaper than Elevance or United Health and has a shareholder friendly buyback policy.)

-

Bruker: a leading nuclear magnetic diagnostics company trading at the lower-end of its historical multiple

-

Merck: a leading pharma company with 20 drugs at Phase 3, and 10x forward PE

We believe several opportunities will setup nicely in the next week or two. If you’d like to explore Lumida’s services, please reach out to marc@lumida.com to schedule a call.

Healthcare firms have a big trend behind them and secular earnings growth.

When you can get them on-sale it’s worth diving in.

The primary risks are lower payouts from insurers, or GLP1s reducing demand (E.g., people getting healthier), or the correction may be over.

Each security and investment could be the subject of its own write-up, and we may change our views as we continue to dig in. We own all of the securities noted above.

Broadly speaking, we like Healthcare, Energy, Technology (Meta, Amazon, Google, Nvidia), select retail stocks and homebuilders.

We will like financials and insurance but see risk due to election volatility.

We have concerns around Utilities, REITs, and over-valued growth stocks.

Small caps will languish with a rising 10-year. Best to wait for the turn in the corner there.

Both semis and small caps best month of the year is November. However, the election and rates will weigh on these categories.

Big picture, we see a continued bull market ahead driven by a rotation.

MACRO: US CONSUMER

One of my favorite tells for the health of the US consumer is Visa

-

12% Revenue growth

-

16% EPS growth

-

56% Net Income Margin

Year over year card spend is around ~5% in the US and internationally.

There’s no recession folks.

The Consumer has shifted their behaviors as they are adapting.

They are going shopping on Black Friday. I have already made my list. (Includes my third set of airpods which inevitably will be lost in my kids closet like the other two…)

Don’t bet against the US consumer.

Speaking of Visa, we noted a few months ago the stock was around its 200 day moving average. That doesn’t happen often.

We hope you profited from that.

Visa:

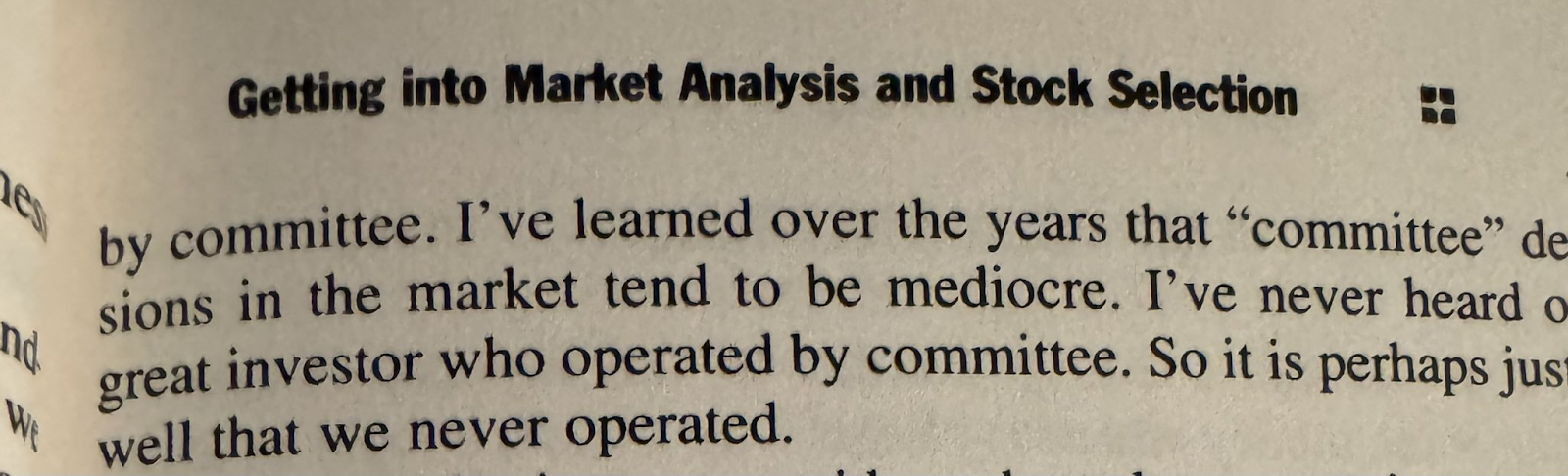

Committees Are Terrible at Investing

Something I have said many times…

Committees lead to inferior investment decision making.

I’m reading the legend Martin Zweig’s book this weekend.

He makes the same point: ‘Committee decisions in the market tens to be mediocre’

The best investors have a Scout mentality.

It’s an exploratory mindset, and often solitary (eg, Templeton, Peter Lynch, etc).

Or, at best, you have one other partner. Think Lewis and Clarke’s expedition. Or Buffett and Munger.

You will notice the US1 list – the high conviction names from Bank of America Merrill – have lagged the S&P…

Committees are terrible.

They require Consensus.

Consensus will get you IBM.

U.S. Stocks now account for 49% of the World’s Market Cap!

Part of this is explained by the fact that international markets have been whacked – see Brazil, Mexico, and India.

Note: All three of those markets were ‘hot’ last year.

We believe just as the 10-year and US Dollar peaks out, at the same time, we will see a rotation into these emerging markets.

Here’s Brazil (EWZ):

If you squint, you can see accelerated selling the last day.

We picked up our old friend Pag Seguero (PAGS) recetly ahead of their earnings coming soon. We believe Morgan Stanley’s bear take on the name is incorrect.

Take a look at Mexico (EWW):

There’s a strong correlation to Brazil.

We are seeing a re-test take place, and high selling on high volume. That’s often a sign of capitulation underway.

There are a number of quality businesses here accessible via ADRs.

In one year’s time, hard to see how these aren’t up 20%ish.

Markets

Money 2020: FinTech

I was at Vegas this past week for the annual Money 2020 conference.

I also had a chance to see ‘Tears for Fears’ in concert with a client who is a music producer from Vegas.

He’s an incredible guy and I hope to interview him on our podcast soon about tokenizing music royalty rights (think Bowie Bonds) on-chain.

In this video, I share thoughts on Las Vegas Sphere, Best Buy, Tesla / Uber, Money2020, Qualcomm…

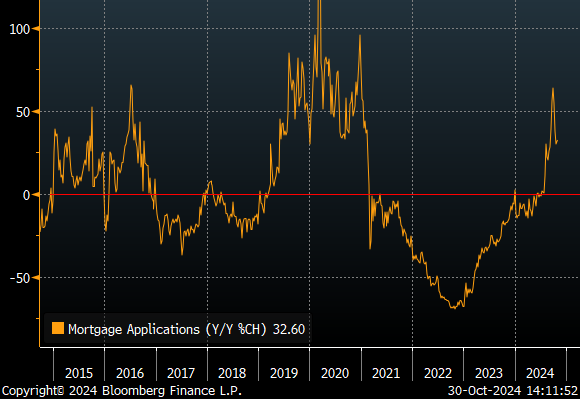

Macro: Housing Market

Our friends at RBA point out that mortgage application growth is up this month to 33%.

That creates more cash in consumers pockets.

More sign that there is no recession folks.

If we get a dip in equity markets, buy the dip. In the long-run, equity prices are driven by earnings growth.

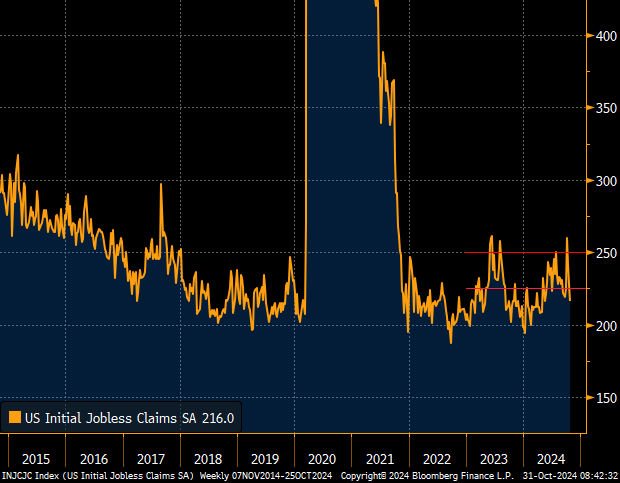

Jobless claims are below 250K as well.

Company Earnings

Nvidia and Google

9/11: ‘Nvidia and Google look mispriced’.

Google reports margins up 4.5%. The stock is up 7% on beat.

Amazon was also up 6%.

Microsoft was down on earnings due to high capex spend.

Within Mag 5, Google and Amazon appear to have room to move higher.

Alphabet CEO Sundar Pichai: “Today, more than a quarter of all new code at Google is generated by AI, then reviewed and accepted by engineers. This helps our engineers do more and move faster.”

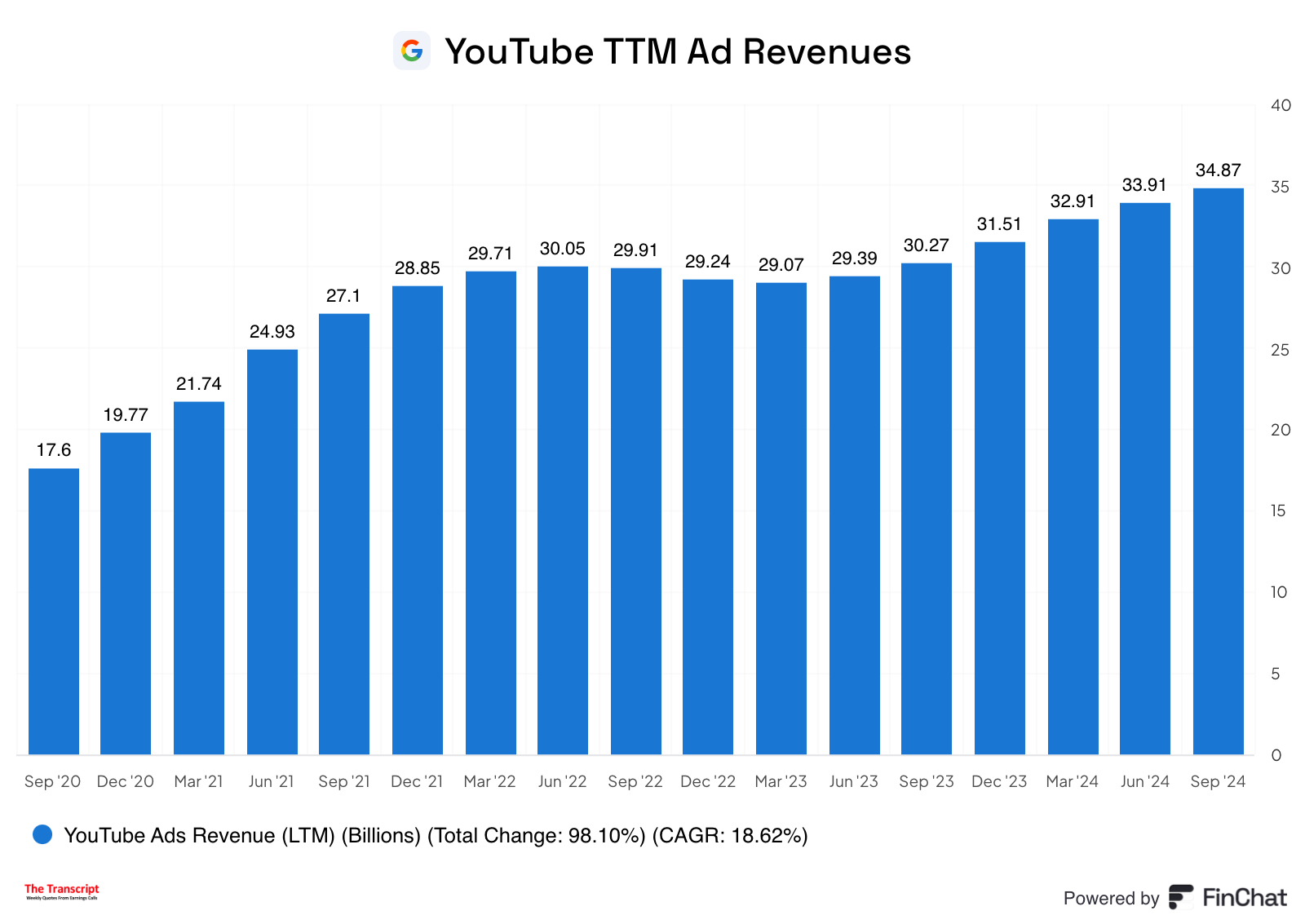

Alphabet CEO Sundar Pichai: “For the first time ever, YouTube’s combined ad and subscription revenue over the past four quarters has surpassed $50B”

Google is an incredible business and monpoly, and its is cheaper than many alternatives due to anti-trust risks. We view those risks as priced in and overblown.

(Should Trump win, expect Google to re-price higher quickly — although our investment doesn’t rely on that.)

Microsoft’s AI business

Here’s commentary from Microsoft:

“We’re excited that only 2.5 years in, our AI business is on track to surpass $10 billion of annual revenue run rate in Q2.”

From $0 to $10B in just 2.5 years.

Within Mag 5, we prefer capex receivers or capex payers.

But, clearly the enterprise and startup demand for AI cloud is here.

AI

Market Demand

Bloomberg reports soaring demand for data centers to support artificial intelligence and cloud-computing will boost global spending in the sector to $250 billion a year, according to KKR.

This should bode well for our investment in leading GPU neo-cloud provider: CoreWeave.

We are up 3x on our investment from last year at this time. We closed another investment in September.

If you want to see more of our private deals, go to www.lumidadeals.com and fill out the form.

Investor Tip: Humility and Limits to Analysis

Sometimes investors or traders have a belief that, if they study it enough, they can define a view on a security or asset class.

Sometimes there is no edge. There are limits to analysis.

The equivalent would be passing on a pair of 6s in poker. You have a pair, but the pair sucks.

This, for example, is how we feel about both utilities and China now.

If there’s no discernible edge why take risk?

These are both categories we owned earlier this year snd then sold into the parabola.

I have a lot more conviction in Mag 5 earnings, semiconductors, retailers and select small caps by contrast where we stand today.

My Son Has a Crush on Blake Lively

My almost 6 year old son has his first crush.

He asked me to send her a message.

I thought this video was hillarious and hope it brightens your day.

Make it a great week, and spend time and call your loved ones and family.

My son wants to marry @blakelively

Parenting is complicated

😂

— Ram Ahluwalia CFA, Lumida (@ramahluwalia)

1:53 PM • Nov 2, 2024

Meme of the Week:

As Featured In