Have Markets Topped?; The K-Shaped Economy

Here’s a preview of what we’ll cover this week:

Macro: The Economy Is Still Holding; The Consumer Is Resilient — But Bifurcating; Corporate America Is Both Confident and Cautious; Private Credit: The Noise Is Louder Than the Risk; AI Is Moving From Pilot to Plumbing

Markets: IGV didn’t Disappoint; The Bubble In Private Markets

Lumida Curations: America Is Still Ahead in AI; Policy Vs Compute; Buy What Broke Hardest

Lumida Crowdfunding Campaign is Live

We’re building the next RobinHood.

It seems pretty clear that AI agents will disrupt old-school advisors. We’re now at a couple hundred active users on the app.

It will be live for about the next two weeks, so if you’d like to be part of Lumida, now is the time to get on board. You’ll find all the details here.

Our investors include former SEC Chair Arthur Levitt. We also have early and first round investors in Coinbase and Circle.

Those companies started with humble beginnings and went on to deliver public markets outcomes.

The Lumida Tribe – this community – is our most unique competitive advantage. No one else has built what we have built here. And now you can own a piece of it.

Sign up here.

Corrections Create the Fuel for the Next Rally

I did a FSD livestream – ”The Hated Rally” – on Friday evening, running through the setup, the bear case I keep hearing, and why I think the bias here should be to buy dips.

The S&P is up nine percent in roughly nine days. That is an extraordinary rally by any measure.

And, in my opinion, we are still far from the top – markets can rally around 10%+ in the next 6 months.

That said, positioning matters. And, I’ll walk thru that too.

The Physics of a Correction

In a correction — especially one driven by big scary headlines, oil spikes, war breaking out — a lot of real money exits the market.

When real money rushes for the exit, prices reprice lower than fundamentals warrant.

Now, when that money wants back in, it doesn’t need to come back all at once to lift prices — it takes less money to pull the market up than it took to push it down.

Misunderstanding this is a common fallacy.

It only takes one marginal seller and buyet to move prices higher.

Fund managers who went to cash or neutral are now in a performance chase.

They can’t afford to miss a rally.

I mentioned some time ago that BlackRock had shifted their stance on US equities from ‘overweight’ to ‘neutral’ right around the lows.

Their exit influenced enormous outflows across RIAs, model portfolios, and their own managed assets.

They need to re-position and get back.

But, this reversal means all that cash is dry powder waiting to come back in.

Sometimes there is more buyers at higher prices, and this may be one of those times.

Notice how funds exposures is starting to pick back up, but is still way of its highs.

Corrections create the fuel for the next rally. That is a core concept and it is worth sitting with.

What about the Strait of Hormuz Conflict?

There’s a legitimate chance of a 2 to 3% pullback in markets.

That would be normal in a world where we just saw a < 1% outcome take place in the last 3 weeks.

Wars are messy. Conflict resolution will be messy.

The IRGC is not offering the same message as the Foreign minister.

Someone said it best ‘The guys with the guns are calling the shots, not the guys in the suits.’

Many investors are looking at the lows, and they feel regret for not getting back in. Add to that the excessive hedging and short interest which creates a natural buffer.

We have had a remarkable rally, and a pullback would be normal here. Still, dips will be bought as many quality stocks have re-priced and investors are offsides.

Trump’s Utility Function is Now Legible

The WSJ just published a revealing piece on Trump’s decision-making during the Iran crisis.

It confirms the thesis I laid out in my last FSD video.

Trump is pragmatic, not ideological.

There were a few highlights in the article.

First, Netanyahu did a remarkable selling the war to Trump (against the advice of many advisors including the Pentagon).

Second, Advisors did not see the Strait of Hormuz closure coming at this speed. DoD war-gaming was flawed. It turns out Kaiser Soze – the perception of control – is enough to deter movement.

Third, there’s the Venezuela hangover.

Trump gained overconfidence from that episode.

He believed decapitation strikes and maximum pressure would produce compliance.

They didn’t.

Iran is not Venezuela. Maduro folded because he had nowhere to go.

The IRGC has everywhere to go — Yemen, Iraq, Lebanon, the Gulf shipping lanes, cyber. Iran has a 40-year doctrine of strategic patience and asymmetric retaliation.

Fourth, Trump uses extreme language to negotiate.

The “end civilization” comment rattled markets and drew global condemnation.

But understand the function, not the content.

WSJ confirms Trump said it to “scare the Iranians”.

That is his negotiating style — throw an extreme anchor, manufacture fear, extract concessions from a destabilized counterparty.

It is the Art of the Deal applied to geopolitics, with nuclear-adjacent stakes.

The same day that comment hit, stocks sold off hard. That was two Tuesday ago, and we started buying stocks on that day. That call is looking right.

Fifth, Trump is watching the tape in real time.

He is consciously calibrating his rhetoric against market reaction.

His advisors view this conflict as a political albatross heading into the midterms.

He doesn’t want American casualties because body bags kill presidencies. He chose not to go into Kharg Island because of fears of casualties. That’s not a warmonger, that’s pragmatic.

Trump wants a TACO because a recession kills presidencies faster.

There is a Trump Put is real.

It sits somewhere around a seven to ten percent drawdown in the S&P.

Below that level, the rhetoric softens and the off-ramps appear.

Above it, the anchors get more extreme. The market is teaching him where his line is, and he is teaching the market where the floor is. That’s the feedback loop.

The open question is ‘what is the utility function for the IRGC?’

A ceasefire requires both factions to agree. A tanker attack requires only one rogue commander.

The IRGC is not a monolithic character. I don’t believe anyone really understands that.

That said, we are seeing tankers move to other outlets, including U.S. ports, for energy.

Markets adapt.

If we see destruction of GCC energy facilities, that would cause us to grow concerned.

If oil can stay below $100, that’s something the resilient American economy can digest.

He has a set of lanes he operates in, and they’re narrower than people think.

What You Should Actually Be Doing Right Now

The bias should be to buy dips.

The distinction I’d draw is mean reversion ideas versus high momentum ideas.

The momentum names — semis, industrials — bounced back the fastest. But it’s a short sugar fix. They’re going to cap out. The capital has largely moved back there already.

The valuations for Industrials are back to 2021 peak levels.

And, the executive teams of companies like Caterpillar and Corning are selling their shares, and sleeping well!

The mean reversion names are where the staying power is. Names that went down 20 to 30% when the market dropped only 9% — that gap wants to close.

Those are the names I want to own, hold for long-term capital gains, and just let the price discovery do the work.

Take Microsoft for example.

It was trading at 20 times earnings. The dip in P/E was even worse than in 2022. The fundamental business is solid.

Claude AI Apocalypse is flipping on its head now. Compute is scarce. Cloud providers like Microsoft, Google, and others are poised to do well.

Here’s our read on their last earnings.

Berkshire is another example. At P/TBV, the stock valuation was at multi-year lows.

I’ve not owned either business in years. They were too expensive! Now, they’re too cheap.

This correction is funny in that we have the gift of buying quality businesses at great prices. That’s why the bottom is in. Investors will look thru to the other side and purchase names based on normalized earnings.

Similarly, consumer discretionary names in XLY are at oversold levels, and present good opportunities.

If oil rips one day, and consumer stocks sell-off – in airlines, or cruise lines, or recreational vehicles – consider buying the dip their.

Investment Philosophy: Invest As If You Were In A Garden

I think this gardening framework actually captures the right investing mindset for this moment.

-

Pull the weeds (unprofitable animal spirits). Water the flowers (high quality businesses at discount).

-

Start early. Follow the seasons. The investors who planted during the correction are already seeing returns. The ones waiting for certainty are going to buy higher.

-

Preparation and patience. You plant the seeds and then you tend to them. Right position sizing — not too much, not too little. Good diversification. And then you wait, patiently, while the market does the work of price discovery.

-

Rotate. This correction is not the same as the April correction last year, which rewarded a different set of categories. You have to rotate the crops. The soil that grew semis and growth in 2024 is not the soil that will grow the next leg. Consumer discretionary, financials, certain quality tech at reasonable multiples — that is where the capital might rotate.

-

And prune. Trim the things that are not working. Hold the things that are compounding. That is how you build a garden that lasts.

There are a lot of risks that got priced in over the last few weeks.

That is an unusual opportunity. Don’t talk yourself out of it.

Macro

Earnings Highlights: Large Banks

Earnings season kicked off with the five largest U.S. banks — Goldman Sachs, JPMorgan, Bank of America, Wells Fargo, and Citi — all reporting Q1 2026 results this week.

The stocks had mixed reaction to earnings despite reporting good numbers across the board.

We keep a close eye on these transcripts as they tell you exactly what CEOs and CFOs are actually seeing on the ground.

The insights this quarter were in line with what you’d expect from the current economy.

The Economy Is Still Holding

The headline read from all five calls is the same: the economy remains resilient, but the environment is getting more complex.

Bank of America CEO Brian Moynihan opened his macro commentary with a positive outlook on GDP, global growth, and the inflation:

“The economy is resilient…the core activities of the economy continue to push along even with all the uncertainty.”

“We see the forward look of GDP growth rates in the U.S. in the 2% range, and we see a faster growth rate around the world.”

“When you look at inflation, the projection is for it to remain elevated in ’26 and into ’27, both on a U.S. basis and a global basis.”

That combination — 2% growth with sticky inflation — is the base case. It is not a recession. But it is also not the clean soft landing the market had been pricing at the start of the year.

The geopolitical wildcard is the Middle East conflict.

Energy prices have spiked — Brent crude saw a record monthly move in March, European gas prices surged 60%.

Every CEO acknowledged this as the primary risk to the outlook.

Citi’s Jane Fraser was the most direct on the geography of pain:

“And inflation is now a greater risk to growth and will likely cause central banks to lean towards more restrictive monetary policies.”

The K-Shaped Economy

Across bank transcripts, we saw consumer spending is up, credit is clean, and tax refunds came in above seasonal norms.

But the aggregate headline is masking a growing divide between income cohorts that every bank flagged this quarter.

Wells Fargo’s Charlie Scharf (CEO) gave the most precise description of where the consumer actually stands:

“The U.S. consumer remains resilient in the aggregate, but increasingly bifurcated beneath the surface.”

“Spending has held up into early 2026 despite slower job growth, supported by higher income households, steady wage growth for incumbent workers and continued access to credit.”

“However, confidence indicators and underlying balance sheet trends point to rising stress with less-affluent consumers.”

“Upper income consumers continue to benefit from elevated equity prices, home equity and cash buffers accumulated earlier in the cycle, allowing discretionary spending to remain firm.”

“By contrast, lower income households are more exposed to higher interest rates and energy prices.”

The energy price spike adds a specific, quantifiable wrinkle. Scharf ran the numbers on what it means for spending behaviour:

“Gas represented 6% of our total debit card spend and 4% of our total credit card spend before the rise in oil prices. They now represent 7% and 5% of debit and credit card spend. Note that these numbers are higher for low-income households.”

“We have seen historically that it often takes consumers several months to reduce their spend levels on other categories to adjust for higher oil prices. And while we don’t know the exact timing, we would expect to see the same in the second half of the year.”

On the credit side, the data remains clean. JPMorgan’s Jeremy Barnum explained why — and what changes that:

“The biggest single reason that the consumer credit performance is healthy is that the labor market is strong.”

“And if you get bad outcomes in the Middle East, much higher energy prices or other problems that eventually track through to the labor market, then you will see that come through clearly.”

“But right now, the story remains the same — resilient consumers doing fine despite higher gas prices.”

The labor market is the single most important variable to watch. Until jobless claims start moving, the consumer holds.

Corporate America Is Both Confident and Cautious

Dimon took the longer view on where the real capital requirements of the economy are heading:

“When I look at the world today — the remilitarization of the world, the infrastructure that people need — I think there’ll be huge capital needs of companies, a huge M&A cycle.”

Moreover, the investment banking and trading environment is as constructive as it has been in years.

Goldman’s David Solomon: “The environment for investment banking activity continues to be incredibly robust, particularly M&A activity.”

“CEOs see an opportunity during this period of time to drive scale in businesses with significant technological change — and that candidly trumps some of the geopolitical risk.”

The structural driver is boards using this period of AI-era disruption to make consolidating moves they could not execute under the previous regulatory environment.

The one gap flagged was sponsor and PE exits.

David Solomon said “IPO activity slowed a little bit, particularly in March” due to valuation uncertainty. But, the pipeline is full and banks expect that to open once volatility settles.

Private Credit: The Noise Is Louder Than the Risk

Private credit dominated Q&A time on every call this quarter.

The banks’ collective answer is that the systemic narrative is outrunning the actual risk.

Dimon laid out the scale question:

“Private credit leverage lending is like $1.7 trillion, high-yield bonds are something like $1.7 trillion, bank syndicated leveraged loans are like $1.7 trillion, investment-grade debt is $13 trillion, mortgage debt is like $13 trillion. I don’t think it’s systemic. It almost can’t be systemic at that size relative to anything else.”

He also flagged banks’ loans to private borrowers are senior and secured with conservative advance rates, borrowing base mechanisms, and cash flow traps in place.

Goldman’s David Solomon took it a step further and did the math on what private credit losses would be in a stress scenario:

“If you take a very tough cycle — the global financial crisis — the cumulative default rates across the entire leverage lending space was 10%, recoveries were about 50%, so the cumulative loss was 5% to 6% against coupons of 9% to 10%. That is the business model of this.”

And rather than viewing a cycle as a threat, Goldman sees it as an opportunity:

“Spreads are becoming more lender-friendly. We’re seeing institutional investors — many of them first-time investors on our platforms, including insurance companies, banks, pension funds — entering the space.”

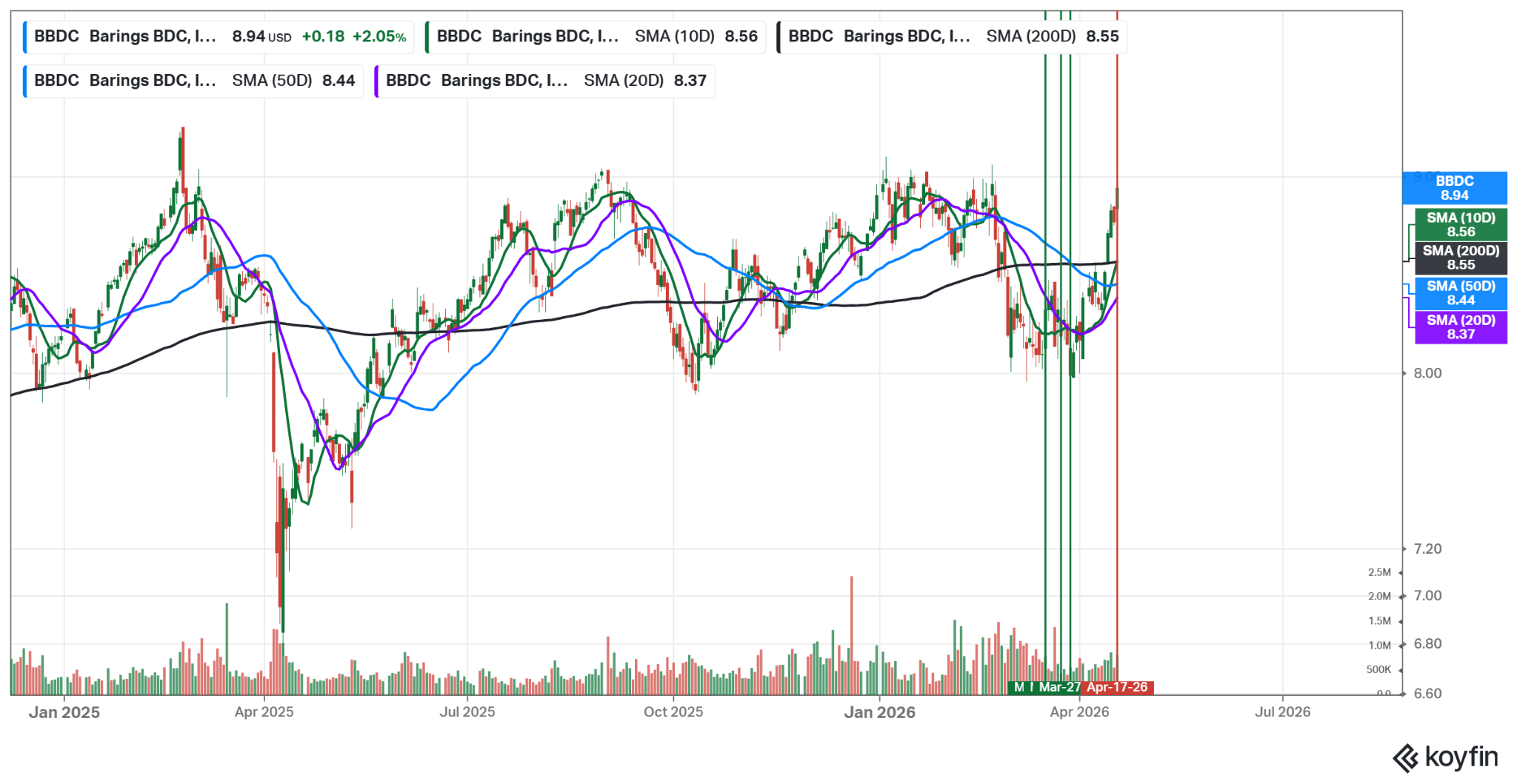

On a side note, these private credit risks had caused serious drawdowns in most BDCs with most trading at over 25% discount to their NAVs.

If we were to take and double Solomon’s math, these BDCs will still be trading at a bargain.

We picked Barings BDC (BBDC) in late March, given their high buybacks and discounted valuations. We exited our position this Friday.

The green lines highlight our entry, and the red one is where we started to trim. (Lesson: It pays to be non-consensus)

AI Is Moving From Pilot to Plumbing

The AI conversation on these calls has matured considerably from a year ago.

Banks are describing a permanent shift in how the business operates, where productivity gains are showing up in headcount and process costs.

We believe Financials are one of the greatest sectors to benefit from AI. Think about all the call centers, loan officers, compliance and service functions that AI can transform.

Bank of America’s Brian Moynihan captured the scale of deployment:

“We’ve got 90 installations working, all 200,000 teammates have access to AI or can use it every day. We’re still in the early stages of what all this will do, but we’re seeing real benefits out of it today.”

Citi’s Jane Fraser described it as infrastructure-level transformation:

“We are methodically deploying AI at scale across the firm to drive revenues and process improvements, enhance client experiences and strengthen our defensive capabilities.”

Goldman is also investing heavily in AI infrastructure. Denis Coleman explained the reasoning:

“We are accelerating our investments in cloud migration, and in the accuracy, completeness and timeliness of our data. These investments are critical to optimizing the deployment of AI solutions across the firm.”

One important caveat came from Dimon. The efficiency gains are real, but the competitive moat from AI may be narrower than investors assume:

“I think it’s a bad idea to think you’re going to deploy AI and improve your efficiency ratio — because in the competitive world, I’m going to do it, everyone else is going to do it, and the benefits will be passed on to the marketplace.”

That is the correct long-run equilibrium.

Relatedly, remember we wrote about Nvidia being cheaper than Exxon on April 5th. The stock was beaten down due to narrative pressure, and we flagged it was worth getting it at those valuations.

The stock is now back at $201, nearing all time highs, and up 17% since that call.

In light of being fair, the hazy crystal ball led to an early entry on FTDR — the stock was down 5% immediately after our call. But, this is the good thing about non-consensus decisions, market eventually reprices them. The stock rallied and is now up 19% since its low.

Markets

IGV didn’t Disappoint

Last week, we noted that the volume picture on IGV was worth a close look. Heavy selling had pushed the ETF down nearly 40% from its highs, with April registering some of the heaviest volume in the fund’s recent history.

We flagged that kind of volume on a selloff is often what seller exhaustion looks like.

And, markets showed the inference was correct.

This week, IGV put in five consecutive green days, gaining ~16%, and moving ahead of its short-term moving averages.

It’s still too early to say whether this is enough escape velocity for software.

A lot of software names report this week and next: ServiceNow, Intuit, Microsoft – and also Amazon.

We’ll learn a lot from the reactions.

On tech, the sector picture is solid as well. Technology is the top performing S&P 500 sector since March 30th, up 18.4% in 12 trading days.

To find a bigger 12-day rally in tech, you have to go back to April 2020 coming out of COVID, and before that, March 2009 coming out of the Financial Crisis.

Historically, after XLK’s move of 15%+ gain in 12D, the sector has a median of 12.8% in 3M and 23% in 6M.

Here is the important distinction though.

Not all software names are the same.

The sector ripped with even low-quality names doing good, but for long term gains, it’s important to position in high quality names.

MongoDB and Datadog at 45x forward earnings is not the same bet as Adobe at 11x.

This is a stock picker’s market inside a mean-reverting sector.

The Bubble In Private Markets

Anthony Scaramucci posted this on why SpaceX’s $1T valuation might make sense.

His argument is the Elon Musk premium and Starlink’s potential justify the high valuation.

He says the rationale behind the investment is you don’t want to miss the next Amazon IPO.

It’s a seductive argument. But, it’s wrong.

Amazon went public at a $500 million market cap. SpaceX is being valued in the trillions.

Price is what you pay, value is what you get. The two are not comparable.

The Amazon FOMO trade works when you are buying at the beginning of the story.

When you are buying at a trillion-dollar private valuation, you are not repeating the Amazon trade. You are paying for the privilege of having been right about the thesis — which the market already priced in before you arrived.

The SpaceX Trillion dollar valuation won’t hold in public markets.

We saw a demo of it with Figma – it’s down 84% since its IPO, and is still trading at 81x P/E NTM. Think about the investors, who got this at IPO. SpaceX might be similar.

And to add to it, SpaceX is moving up the vesting schedule of employee shares before IPO. This might lead to the biggest exit dumping ever.

SpaceX’s valuation is the private market bubble in its most visible form.

The Alpha In Private Deals

The key to success in private deals is opting for what’s non-consensus – that is where the alpha lives.

We recently closed a round of investment in a Defense Technology firm –Shield AI.

The more consensus name in defense tech was Anduril – we looked at it, and liked Palmer Luckey’s tenacity, but it was valued at $60B.

Shield AI was 6x cheaper at $10B, and with autonomous AI drone technology that was used worldwide including the United States and Taiwan

After we closed this, the Iran conflict broke out and the name went up in valuation 30%.

Kind of a funny hedge.

If you are accredited and want access to exciting private deals, sign up here.

Lumida Curations

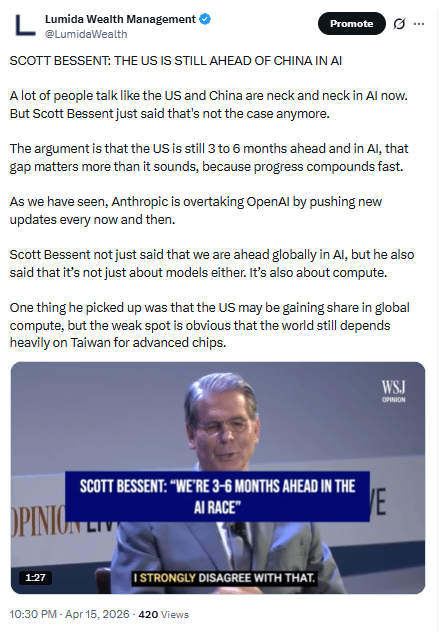

Scott Bessent: America Is Still Ahead in AI

Bessent’s point is that the U.S. still holds a real lead in AI, and the bigger story is not just models, but the compute advantage underneath them.

Policy Vs Compute

Jensen’s warning is simple: the U.S. has built a massive lead in AI compute, but bad policy could hand that advantage to the rest of the world.

Buy What Broke Hardest

The market’s message is shifting: when the most battered sectors stop falling on bad news, it usually means the bottom is being built and the next move is higher.

Meme

Not Subscribed Yet? Don’t miss out on future insights—subscribe to the newsletter now!

For real-time updates, follow us on:

X | Telegram | Youtube | TikTok | News | Ram’s X | Lumida Health | Lumida Tax

As Featured In

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.