Hollywood Secrets, iPad Killer, Whale Watch & Crypto Miners

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

-

Macro: Economic data, Alexi Navalny dies

-

Markets: SOXX performance, The Retail rally, Apple’s vision pro

-

Company Earnings: Key themes and headlines

-

AI: Nvidia Chat RTX, SaaS Earnings, SMCI

-

Digital Assets: Crypto miners and altcoins

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Click to watch on Youtube

Non-Consensus:

This week Ram had an in-depth conversation with Don Handfield, Hollywood actor, writer, & producer. We found out Hollywood & Silicon Valley are quite similar!

Don produced ‘The Founder’ – Ray Kroc’s biopic about the birth and growth of McDonald’s

Here are a few lessons. But, the stories and insights are priceless – we encourage you to listen on Spotify or watch on Youtube.

What I learned:

– How Netflix has changed movie making

– How AI is changing the creative process

– Producing a movie is no different than building a startup

– Hustle is everything.

Don figured out how to connect with Ray Kroc’s family the same way an entrepreneur figured out an warm intro to a VC

– The best ideas are borne of obsession.

They marinate in the mind of the creator over many years.

– It starts with vision, attracting financing, building a team, and shipping product on a budget

– Purpose = Perseverance. If you do it for the money, you won’t have the staying power

– Mythological stories and drama are at the center of great movies, stories, and founder arcs

– Mental health is a real issue in Hollywood and in startups. It’s not discussed enough.

– Hollywood, and Don specifically, wants to tokenize IP to dis-intermediate the gatekeepers

– Non-Consensus movies are the best. Re-shaping a perception on an old topic

– Building a movie can take a real toll on family life

– The hardest part and the greatest joy in making a movie is in the people

– Luck and chance encounters or introductions plays a role in success.

Pay it forward.

– The producers of today are building on the lessons and mentoring of the prior generation.

– Self deception & self-sabotage limit human potential

– The best creatives travel the dark night of the soul and bear a heavy emotional burden

– The deal waterfall economics of movie making

Have a listen

WSJ: Alexi Navalny, Putin Critic, Dies in Prison

Alexi Navalny made a voluntary decision to return to Russia after being poisoned: “I will not give Putin the gift of not returning to Russia.”

He knew full well he was on the other end of a police state, rigged courts, censorship, and a national security machine.

His cause of Death still being established.

“The cause of his death was still being established. He collapsed after a walk at his prison colony on Friday after which, they said, he lost consciousness and couldn’t be revived.”

Is it really that hard to determine the cause of death?

Excerpt:

“Navalny had become a cautionary tale for others who chose to challenge the Kremlin. Navalny’s Anti-Corruption Foundation, the vehicle for his political activism, was dismantled inside Russia and his allies were either imprisoned or scared into exile.”

“Even behind bars, Navalny continued to criticize Putin and his policies via texts on social media that were passed via his lawyers. Three of those lawyers are now in jail in Russia on charges of participating in an extremist movement. Two of his lawyers who fled abroad have been arrested in absentia.”

There’s your cause of death.

Today is a sad day for an extraordinary champion of human freedom.

You don’t have to be Russian to recognize Navalny was an extraordinary human being.

Putin went to great lengths to avoid saying Navalny’s name.

Today, I’m going to do the opposite.

Navalny. Navalny. Navalny. Navalny. Navalny.

What a Hero.

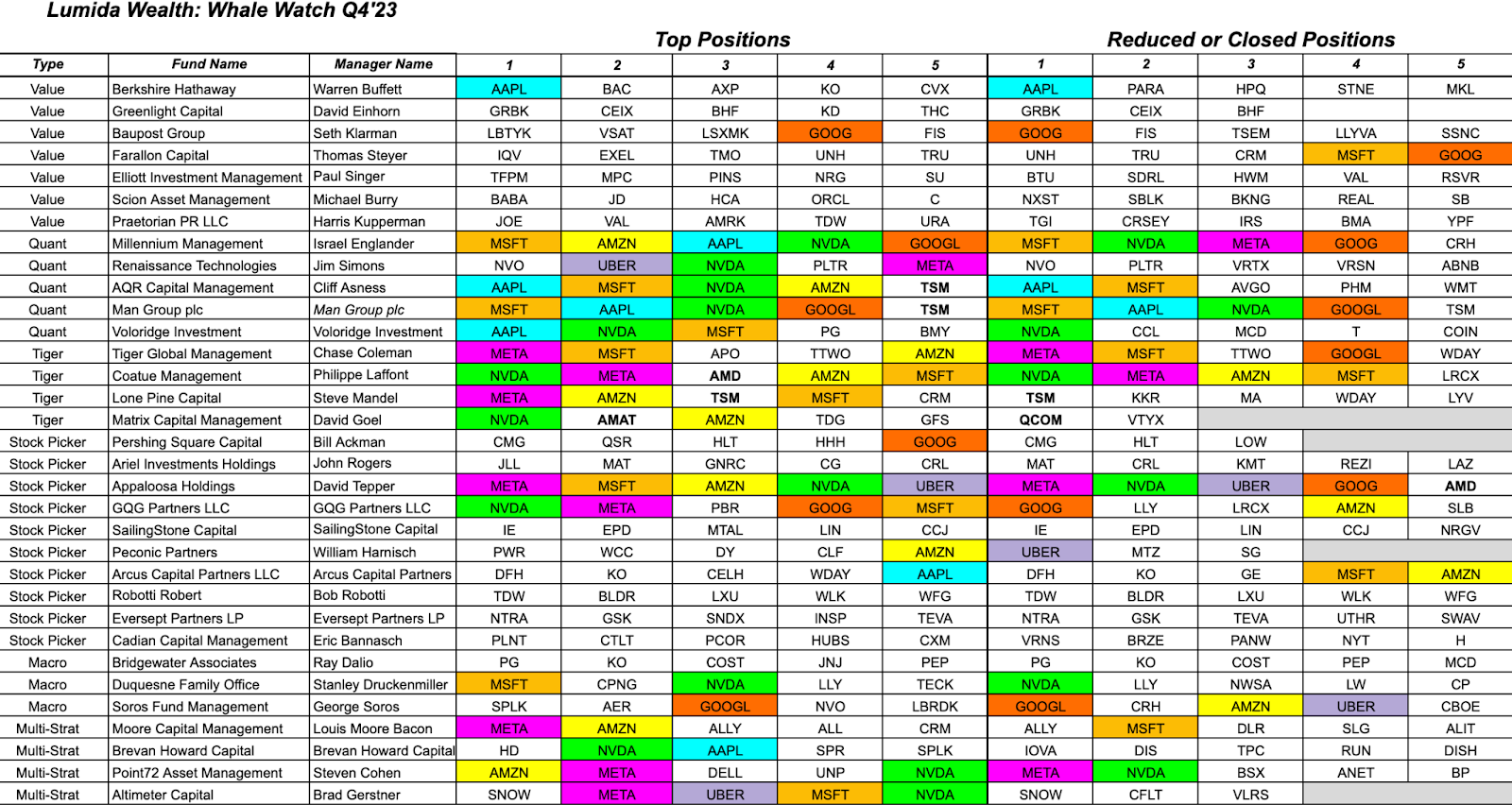

Lumida 13F Hedge Fund Tracker

Q4’23 13F filings are out and that means Lumida Whale Watch is on active duty.

From $90 MM in AUM to $300+Bn, segregated by style & positions, we analyze fund managers to spot non-consensus ideas, new trends, and overcrowding.

Some key insights:

1. Meta is now the most favored top position amongst hedge funds we track for top holding.

> Lumida was already long Meta and shared our thesis on Howard Lindzon’s podcast before earnings

2. Nvidia is still the most favored position across all Top 5 positions

> Lumida is long Nvidia. It’s a great firm, but we intend to start trimming positions and rotate into other semiconductors soon.

3.TSLA, NFLX, not among top holdings among any funds. These are crowded retail stocks in our view.

> We had a short call on Tesla and Apple – both successful.

4. HF favorites in order are Nvidia, MSFT, Amazon, Meta, Apple, and Google.

> Google is Non-Consensus. In Mag 7, Google is the only name not priced for AI. This is a high conviction idea for Lumida. We want to accumulate as much as we can for as long as we can. Don’t get us started on the Youtube story…

6. NVDA had 7 reduced positions. Some HFs are selling into strength.

> We agree with lightening exposure to Nvidia – bring it back to benchmark weights at the very least if you were overweight

7. NVDA, TSM, AMD, AMAT, major players in the semiconductor industry, are among the top holdings, held by ~50% of funds

> We recommended owning AMAT going into earnings. AMAT popped 6%. We believe AMAT may have higher upside than other semiconductor names that have had their run.

8.Oracle is not widely held, and hedge funds reduced their positions

> We shorted Oracle across all client accounts as we shared in last week’s newsletter. We covered this week and profited. Oracle is a great hedge against our software portfolio.

Oracle is in the ‘hype not meeting substance’ AI bucket. I expect Oracle will disappoint during its earnings

9. Amongst semiconductors, TSM has emerged as the top/new position with 4 funds

10. David Einhorn & Thomas Steyer have added multiple positions in pharma & biotech targeting health & wellness themes

> Funny to see value investors moving into pharma & biotech. As you know, we started scooping up biotech names a few months ago.

At Lumida, we find these an excellent source of idea generation. We prefer to focus on names no one is talking about. For example, we identified Tidewater – an energy services firm with a unique position doing buybacks – with this analysis.

We can also identify ‘hedge fund crowding’ (caution) or emerging themes (lean in) ahead of Market Consensus.

We don’t know any publication like this nor any wealth manager that actually does the hard work to prepare and then study these names deeply.

This is one source of input among many that we incorporate into our process.

We do and it shows in our research and results.

Here’s the Link to the Google Spreadsheet Raw data

Here’s the analysis and infographics on our website

Ram’s Demo of The Apple Vision Pro

I went to the Apple Store at Grand Central to try out the Vision Pro.

If you own Apple stock, give it a listen.

We believe Apple is primed to disappoint.

Meta is dialed into the gamer enthusiast segment. Apple is straddling many customer personas.

And Apple has a content library gap. You can’t watch Netflix. You can’t get an immersive experience. They will need 2 to 3 more years to build that out.

I believe the Apple Vision Pro will attract early adopters… but, beyond that, this is a disappointment.

Lumida Call on Apple and Oracle Short

Last week, we wrote: ‘We added shorts on Apple and Oracle to reduce our exposure’

Both Apple and Oracle were down for the week. We closed out those positions, and may look to re-initiate if they bounce.

If you are surprised at the uncanny win-rate on our public calls, so are we. 🙂

Past performance is not indicative of future results. The success of our public calls reflects our commitment to rigorous analysis and market understanding, but it should not be considered a guarantee of future performance or success. Investing in financial markets involves risks, including the risk of loss. We advise every reader to consider their investment objectives and risk tolerance carefully before making any investment decisions.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Macro

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Immigration Wave Delivers Economic Windfall. But There’s a Catch.

Immigration is a controversial topic.

We noted a few months ago that immigration – about 1 MM legal Visa and perhaps ~3 MM illegal immigrants – likely provided a boost to the economy.

Immigration may have confounded economists’ expectations. Very simply, you can break down GDP into the product of two numbers: Labor & Labor Productivity.

This article states that the new influx of immigrants may be less productive (e.g., less income) than prior cohorts.

It’s high time Congress enact immigration reform to increase the quality of legal immigrants.

There’s a shortage of nurses – and the United States is not issuing additional Visas to the Philippines (as one example).

And that’s also why we invested in APEI – a small cap stock training nurses. The stock is up double-digits YTD.

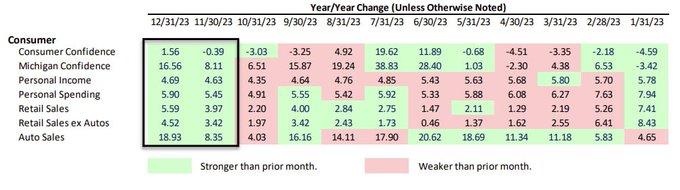

Macro – No Sign of Economic Weakness

Take a look at this summary of economic data.

There’s no sign of economic weakness anywhere.

Markets are patterning similar to 1986 and 2017.

Those two years had record overbought levels.

They were followed by more overbought conditions.

The main conclusion was there are dips, and the dips should be bought.

That certainly is playing out now.

The last time economic data came in this strong was 2013.

That was also bullish.

Stick to ‘Quality Momentum at a Reasonable Price’.

The flip side is we are likely to see ‘higher for longer’ interest rates.

Larry Summers this Friday evening suggested there is a 15% chance of rate hikes. That’s a new narrative that could cause equity markets to have an allergic reaction.

The long-run looks bright, the short-run for equity markets looks vulnerable to a correction.

Last week we said markets were primed for a correction.

The S&P and QQQ finished lower for the week.

Still think markets are perfect discounting mechanisms?

Markets

Market Compass

Let’s cycle through our three-prong market compass as we look to the week ahead.

1. The 10 year bond yield increased over the week at 4.28%, up 11 bps WoW.

When this increases, that hurts valuations for long duration stocks.

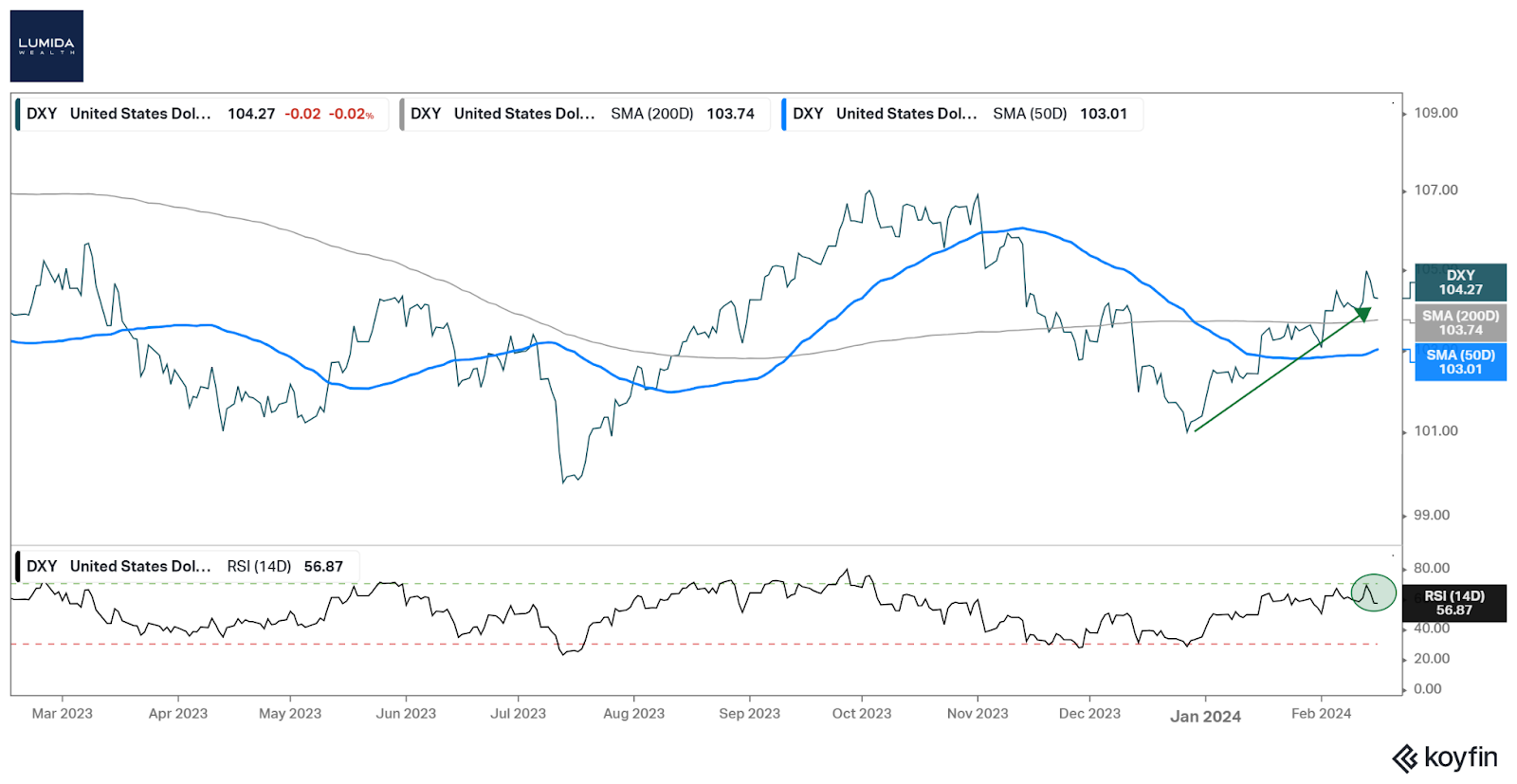

2. The US Dollar is turning up, currently at 104.27 (Up by 2.86% YTD)

When the USD increases in values, US equities decrease in value.

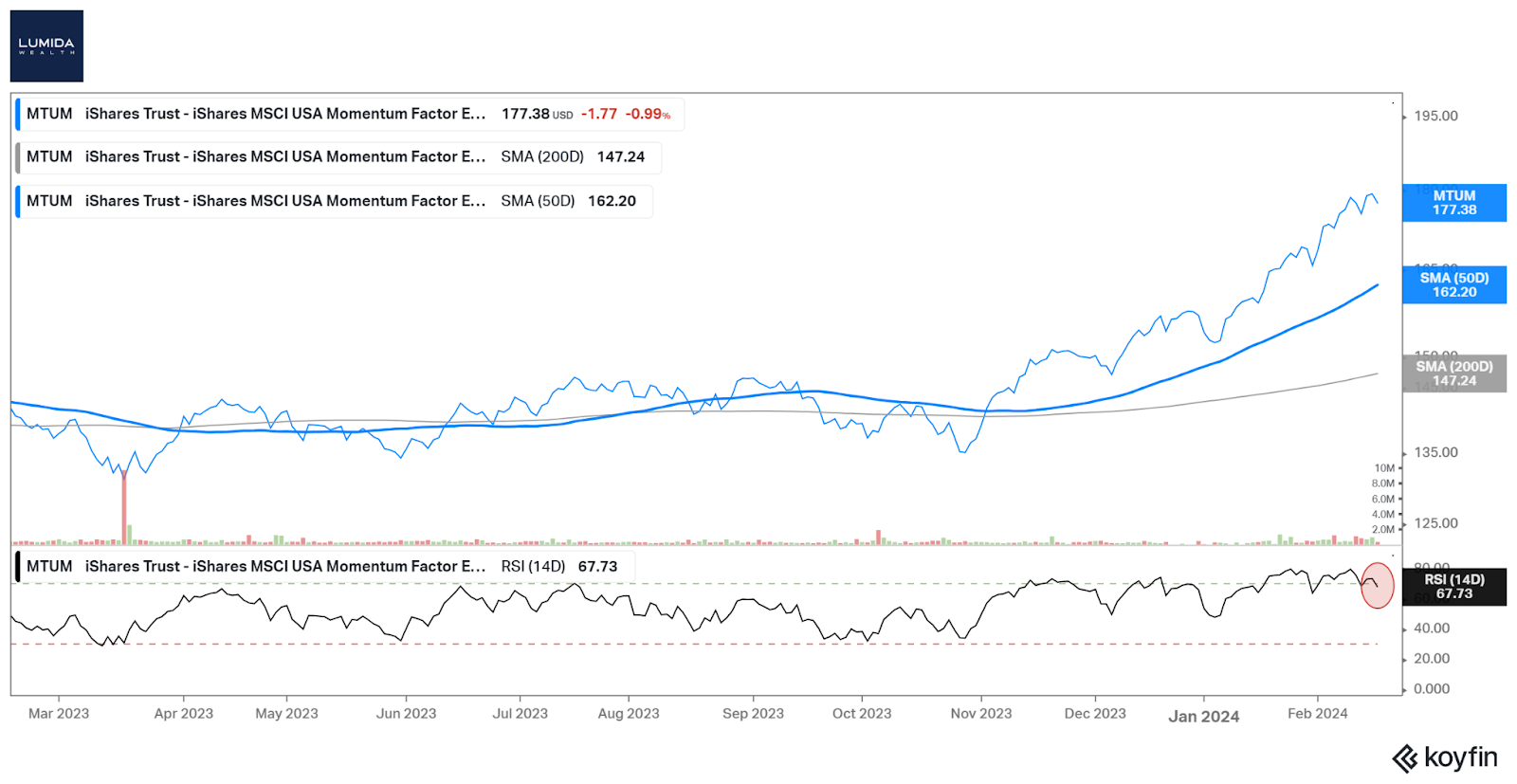

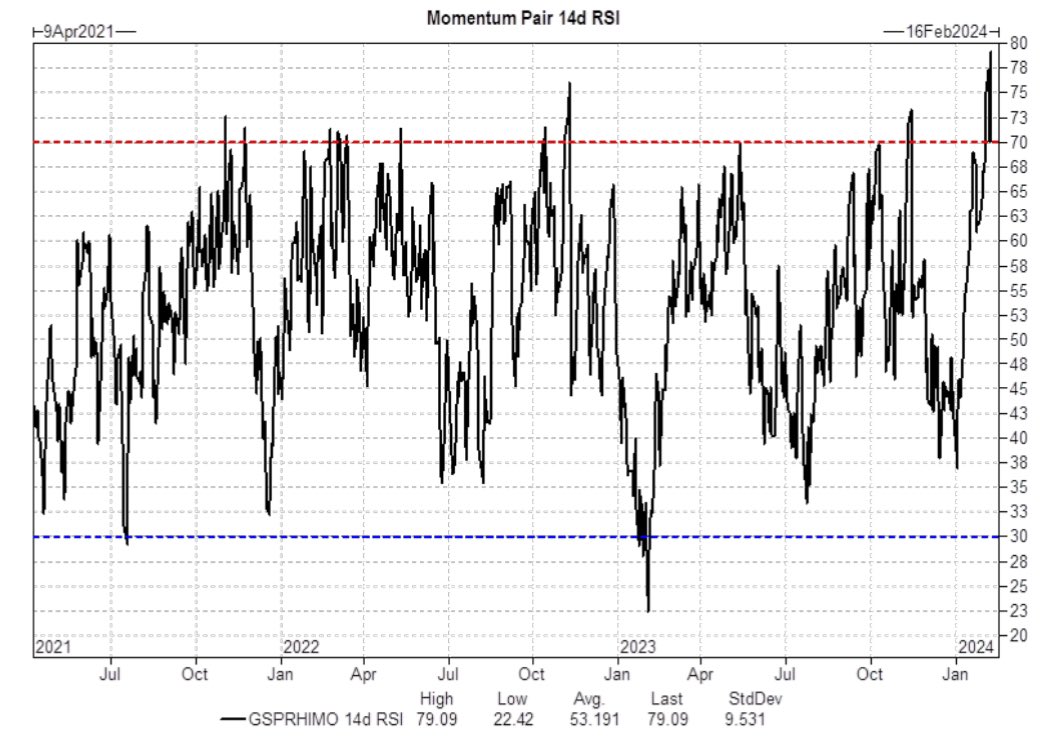

3. Momentum Factor ETF

Take a look at the ETF – MTUM. It contains quality momentum technology firms:

MTUM is also experiencing a parabolic surge.

Within MTUM, notice the leaders are starting to roll-over. Microsoft’s stock is heading below its 20-day moving averages.

When the leaders are tired, the weaker names start to follow.

Relatedly, look at the blow-off top in SMCI – a semiconductor that went up dramatically.

Retail investors are starting to get their hands burned chasing into semis. The time to buy was back in October folks…

Other data points: Bitcoin equities such as MSTR and MARA are down. These highly speculative ‘marginal liquidity’ markets are a measure of retail sentiment.

Carvana, a battleground stock between hedge funds and retail investors, was down 8% this past Friday.

Apple and Oracle are down. Remember last week we said we should short those? That worked out marvelously. We have since covered both and will look to rotate to other names as there’s less meat on the bone now.

Take a look at Apple. It’s back to its trendline. Could it drop further? Yes. But, we’d rather focus on higher probability opportunities.

Recent data increases our conviction that we are due for a pullback or correction.

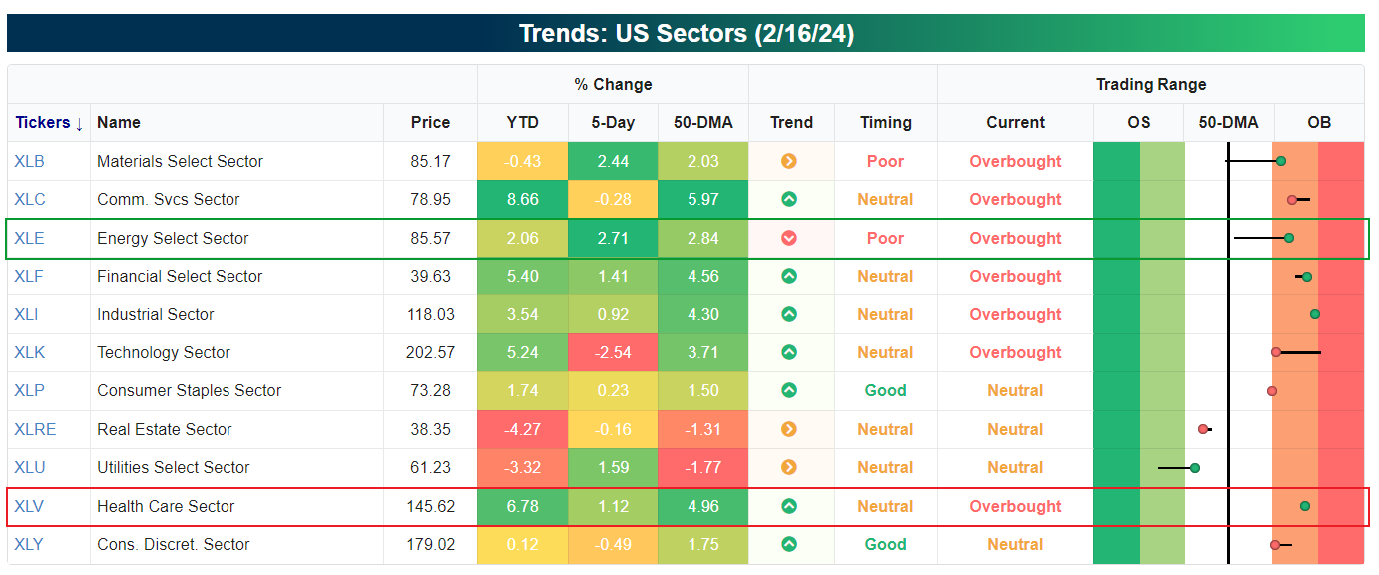

4. US Sector Trends

Energy and Healthcare are up 2.71% and 1.12% respectively, since last week.

Remember we bought Haliburton a few weeks ago? That’s adding valuable diversification against our tech names.

Both energy and healthcare are good sectors to allocate new money to – especially if there is a pullback.

From a revenue and earnings perspective, these two categories delivered the best non-consensus performance.

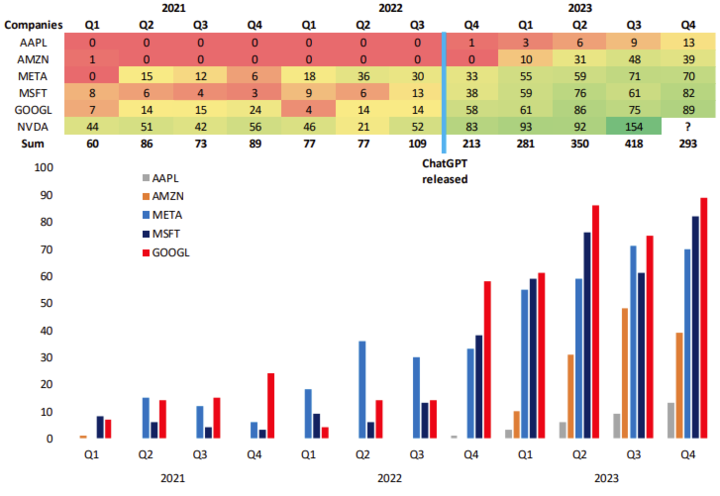

AI is the Primary Theme Carrying Markets

We’ve been discussing narratives and themes. There are 3 primary themes:

-

AI & Semiconductors (see the chart below showing how Chat GPT helped to fuel markets)

-

The ‘Trump Bump’ (scroll down for more)

-

Fed & Inflation. Larry Summers added cold water to this (see above)

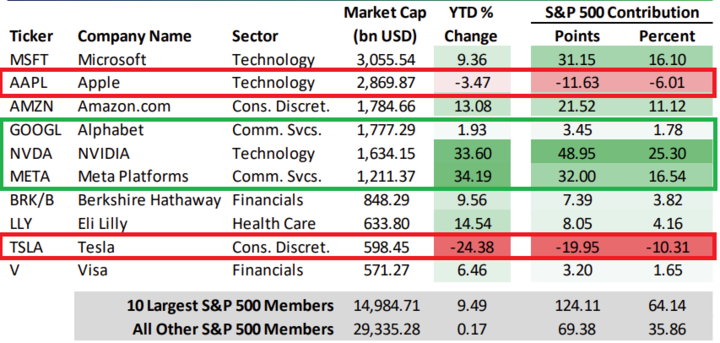

Here’s a quick view into our favorite Mag 7 names, and the names we don’t like.

Notice, once again Apples and Tesla are lagging YTD. Simply not owning these names means you are outperforming.

And, Google, Nvidia, and Meta are strong. Microsoft is Consensus as we have noted, and the stock is weakening now. We have yet to see hard data on Co-Pilot subscriptions.

We could see a disappointment in their earnings next quarter. The reality is Co-Pilot is hallucinating making it semi-productive – it’s not a killer app – at least not yet.

Both Microsoft and Chat GPT have AI disillusionment narrative risk.

Google is priced for obsolescence – that means more upside as they execute.

Nvidia is now more valuable than the entire Energy sector.

That means Nvidia is worth more than Haliburton, XOM, Chevron, Shell and scores of other companies producing valuable energy.

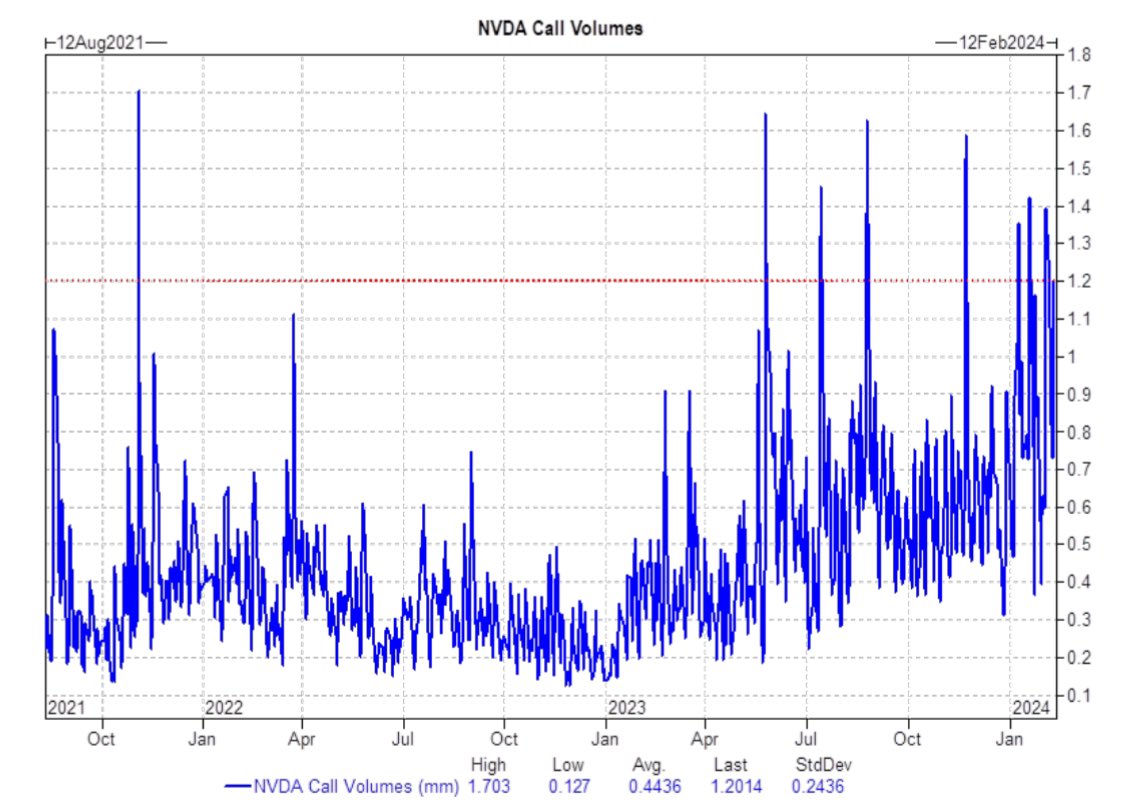

We believe Nvidia is the real deal… but YTD Nvidia is up~46% YTD. We’re going to reduce our position soon.

When? When we finally see red bars. Nvidia has high ‘serial auto-correlation’.

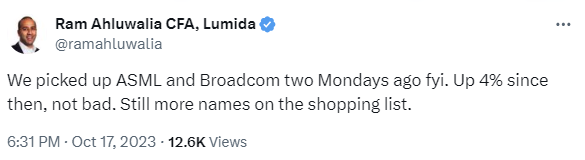

On ASML

ASML took over as the world’s No. 1 chip equipment maker by Revenue in 2023, beating Applied Materials, the leader for decades.

Our view today is that ASML is overbought. We’d rather own AMAT here.

At some point, when we inevitably get oversold conditions, we will then buy ASML.

Now is not the time to add to one of our favorite semiconductor names.

Remember, we bought ASML in the 500s in October and now it is in the 900s.

Here’s the timestamp of our call to buy ASML and Broadcom:

SaaS Software

We continue to like software.

Trimming exposure to overbought Mag 7 names – like Nvidia and Microsoft – and increasing exposure to software is a great idea.

We have a Conviction Buy list of a dozen names we like. We wait for those names to go on sale, then we buy them.

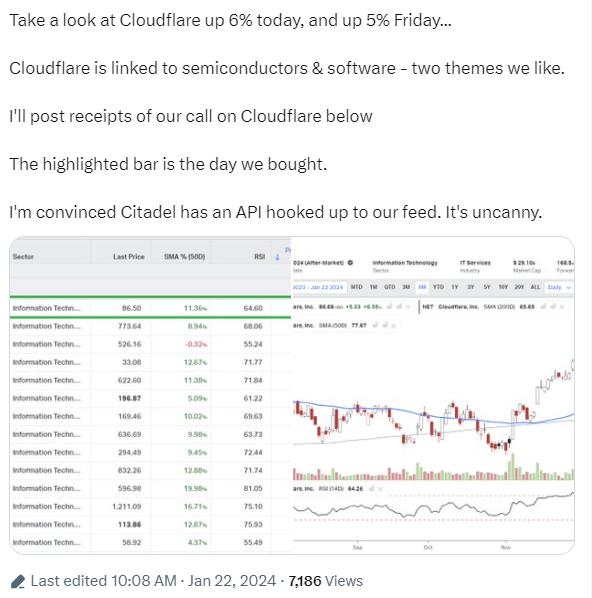

We bought Cloudflare and MongoDB a few weeks ago when software was oversold.

The main headline in software is revenue growth is set to accelerate. Analysts are behind the ball.

Here’s a link to our Cloudflare call. We would not buy Cloudflare here. ‘You make your money on the buy.’

Goldman Sees Speculative Activity

We wrote this on Twitter last Monday saying we expect to see a pullback in 1 to 3 days.

That happened:

Goldman: ‘We’ve seen a large increase in retail call options, short covering in anti-momentum factors, and buying in low quality, all new and accelerating.’

The Quality Momentum Rally has given way to the Retail FOMO Rally.

Take a look at these charts…

As you flip thru them, overlay July ‘23 and Dec ‘21 in your mind’s eye.

Those were local market tops.

Note the biggest winners in QQQ today lack thematic unity. The AI theme had several names on the losers list.

Crowded retail investors are generally late to the party.

That’s when you get out of the pool.

You’re going to see something floating in the pool soon.

Nvidia is still green so until the leader rolls over we wait.

My best guess is we have 1 to 3 days to go, you really need to re-assess each day.

This is the opposite of ‘capitulation stalking’.

Zooming out however, the bid for US equities is tremendous.

The wall of money is trying to find a home.

And it is looking to small caps & biotech.

There’s better value there.

Rotate, rotate, rotate.

We bought a small cap growth stock INSP today.

They provide minimally invasive care solutions for those that suffer from sleep apnea.

80% margins, 50%+ revenue growth, cashflow positive, and growing TAM

The fastest growing demographic is the ‘oldest of the oldest’.

Let’s see how this does in 12 months.

Chart 1: Momentum Stocks are Overbought

Chart 2: Retail investors, last to the party, are crowding into Nvidia

Chart 3: Retail investors are buying loads of Nvidia call options

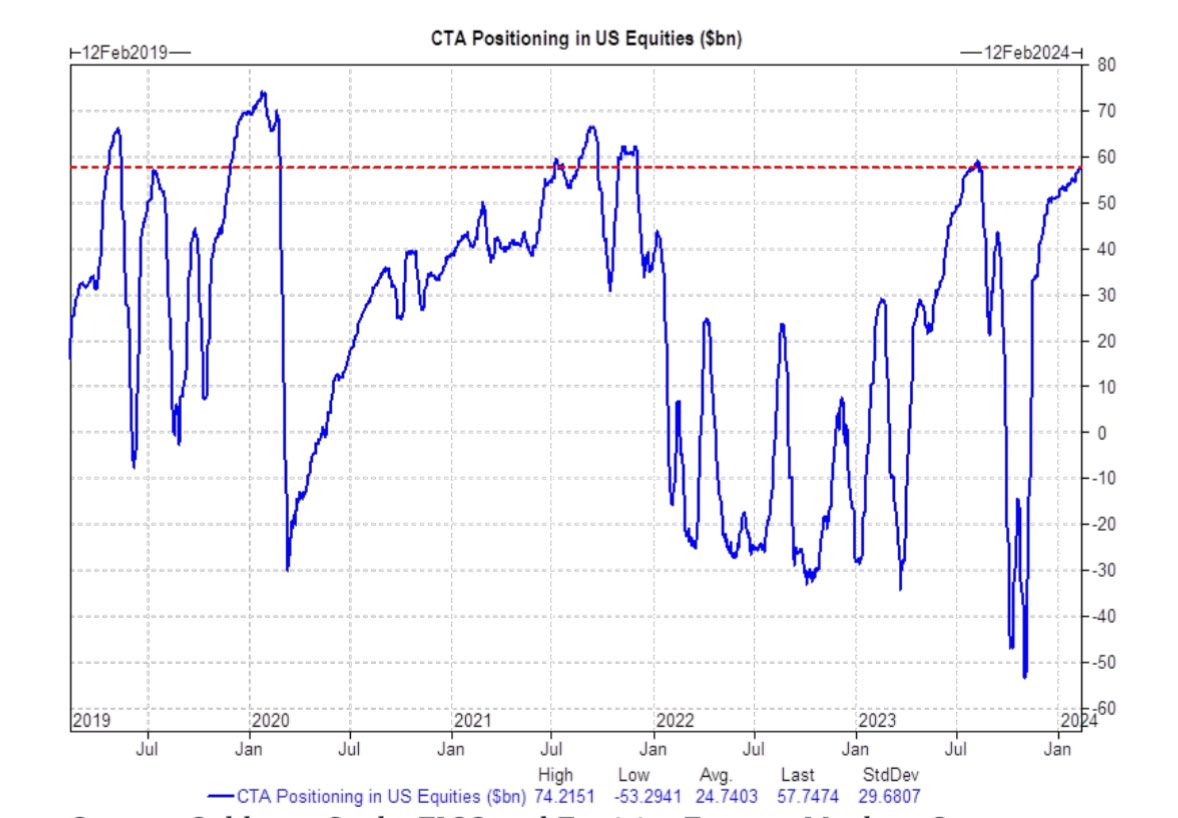

Chart 4: Commodity Trading Advisors (CTAs) are near max long

You can’t get more long than max long folks.

Bloomberg: ‘Apple’s Vision Pro is an iPad Killer’

Apple is disrupting…itself?

‘There’s been a lot of talk that the headset could be the future of the Mac or a replacement for the iPhone.

I don’t think either is true.

After using the $3,499 device for about a week, I believe the Vision Pro could instead cannibalize the iPad. It has the potential to provide a far better experience for the main jobs that Apple’s tablet was designed to handle.

But don’t get me wrong, it’s still very early days.’

Disclosure: I am short Apple as of this Friday as a hedge against our tech gains.

Also short another firm we shall simply codeword ‘MAUI’. Will share more later… Need to build position.

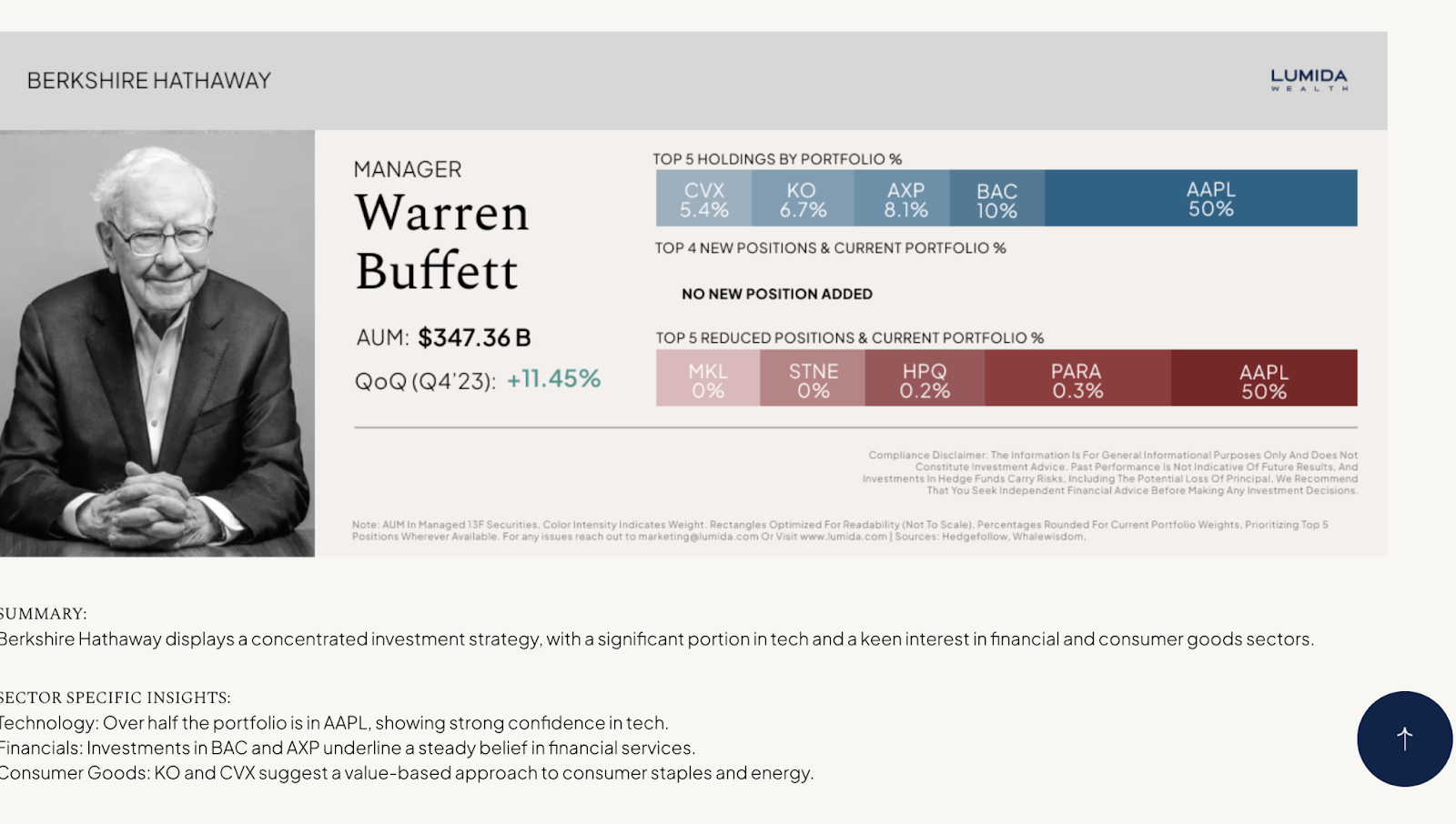

Berkshire Trims Apple Position

I have studied Buffett and Munger with admiration over many years.

I can’t tell you how satisfying it is to know that we beat Buffett to the punch on Apple.

The passive index flows are providing Buffett with exit liquidity now.

To my knowledge, Lumida Wealth was the first to stake out a critical and vocal stance on Apple over the summer.

Since then there have been ~6 analyst downgrades.

Take a look at how our Apple short is doing since we initiated it Friday and documented in our last Sunday newsletter.

The Apple Vision Pro is a science experiment that lacks Product Market Fit.

Mr. Market is expecting weakness and selling the stock.

Investing Tip

Something I say often:

‘You make your money on the buy’

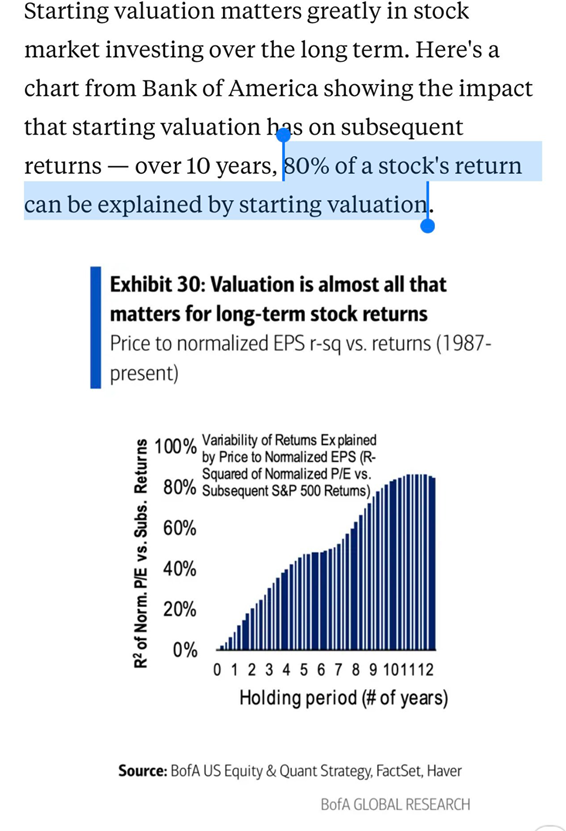

The drivers of stock price returns, in order:

1. Multiple expansion (by cheap!)

> Explains a whopping 50% of the cross-section of returns

2. Earnings growth

3. Buybacks

Are there stocks where you can find all 3? Yes.

You should notice that we never buy stocks at all-time highs – we are always looking for pull-backs or more favorable entry points…

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Company Earnings

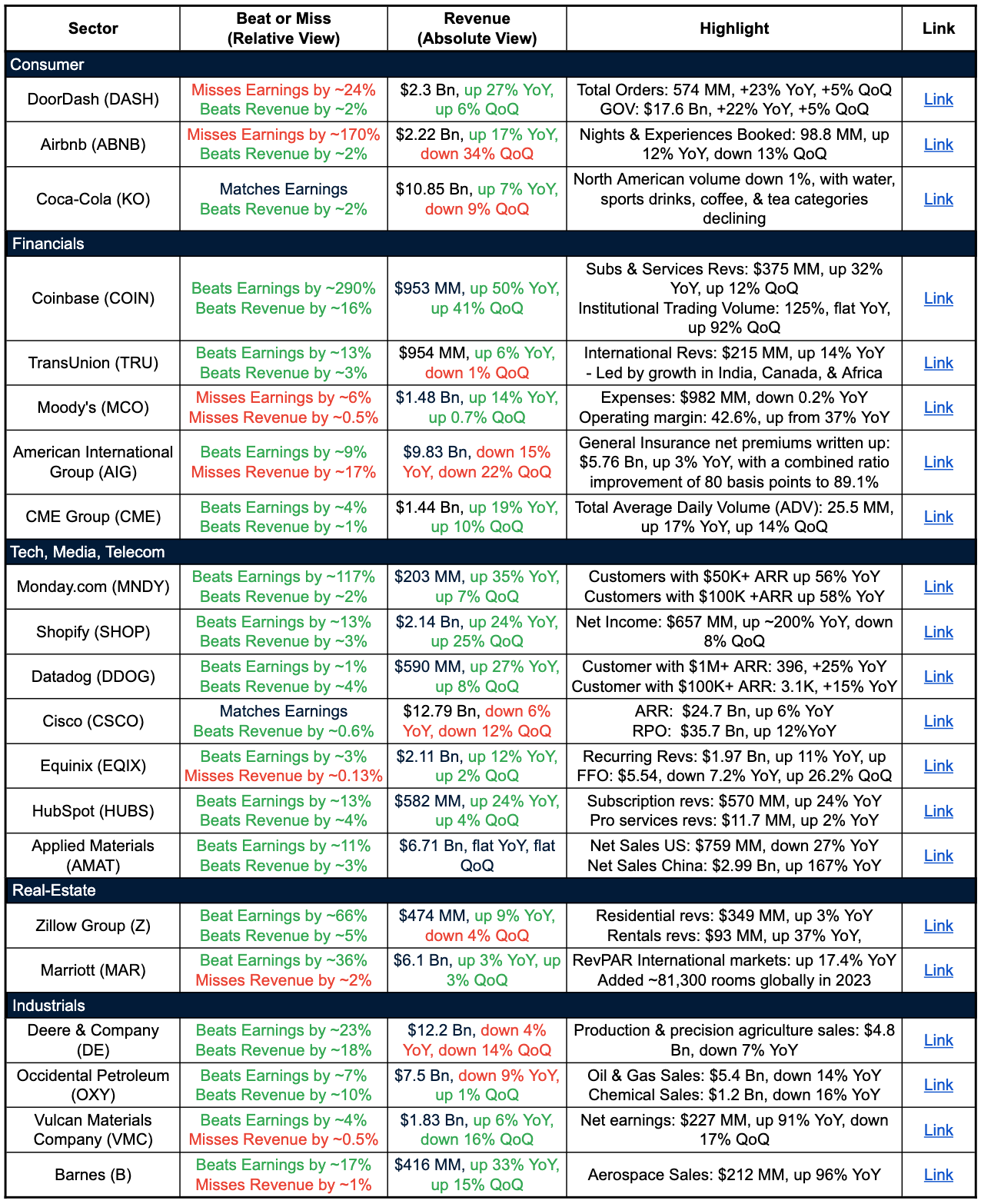

Broader Trends observations this earnings season:

Sellers to China are feeling the pinch

-

We saw this with Apple and Starbucks

Consumer:

Companies reported: DASH, ABNB, KO

-

Food delivery platforms like DoorDash are seeing steady growth in orders and gross order value, though profitability remains a challenge as consumers hesitant changing their behavior from physical to online grocery delivery

-

Travel demand uneven – Airbnb saw booking growth but had a relatively poor holiday season, with nights and experiences booked down quarterly

-

Consumer staples like Coca-Cola are facing volume declines in some key categories like water and sports drinks.

Industrials:

Companies reported: DE, OXY, VMC, B

-

Agriculture equipment makers like Deere are facing sales pressure in production and precision agriculture equipment.

-

Energy companies like Occidental Petroleum are growing oil and gas revenues with higher prices but the chemical segment is weaker.

-

Construction materials firms like Vulcan have higher earnings but are facing volume declines.

Tech, Media, Telecom

Companies reported: MNDY, SHOP, DDOG, CSCO, HUBS

Trend:

-

Software/SaaS companies like Datadog, Monday.com and HubSpot posting strong customer growth especially in higher spending tiers.

-

E-commerce platforms like Shopify are driving steady revenue growth and improved profitability.

-

Cloud services still seeing strong growth

Financials:

Companies reported: COIN, TRU, MCO, AIG, CME

-

Crypto/digital asset platforms like Coinbase are seeing continued user & payment volume increases due to the boost of bitcoin ETFs (COIN)

-

Growth in international markets (India,Canada & Africa) fuel consumer credit companies (TRU)

-

Credit rating agencies like Moody’s have solid revenue growth but compressed operating margins.

-

Insurers like AIG are growing premiums written in core general insurance units.

Chip manufacturing

Companies Reported: AMAT

Trend:

-

Continued trend of all semiconductor companies beating estimates on earnings and revenues

-

Contrary to other sectors, semiconductor firms selling to China are seeing a significant boost in sales

Real Estate:

Companies Reported: Z, MAR

-

Online real estate platforms like Zillow see higher growth in rentals vs residentials business segments

-

Hospitality/lodging firms like Marriott benefiting from continued travel recovery, especially in international markets.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

On AI

Nvidia’s Chat RTX is clearly a dig against competitor Microsoft and surrogate OpenAI

Make no mistake – Nvidia and Microsoft are competitors

Nvidia is pushing for an ‘on prem’ world (or a world powered by CoreWeave :), where Sovereigns fully control their stack

Microsoft’s vision is ‘plug into our cloud and we’ll make sure you are secure’

YC put out their “requests for startups” today

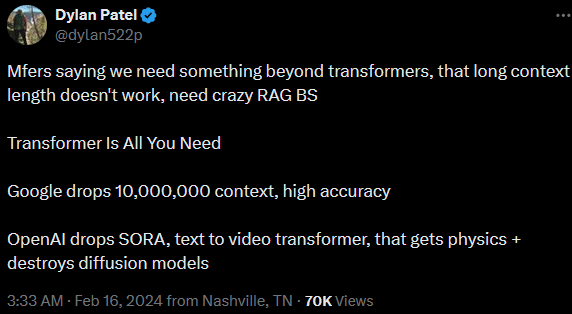

Google Gemini AI Drops

Google drops 10,000,000 context, high accuracy LLM. We are slowly starting to see Google Gemini show their hand.

As you know, we’ve been on the Google story for quite a while

Meanwhile, OpenAI drops SORA, text to video transformer, that gets physics + destroys diffusion models.

But, we’re not going to see SORA disrupt Hollywood anytime soon.

Knowledge work disruption will come from the Google multi-modal models first.

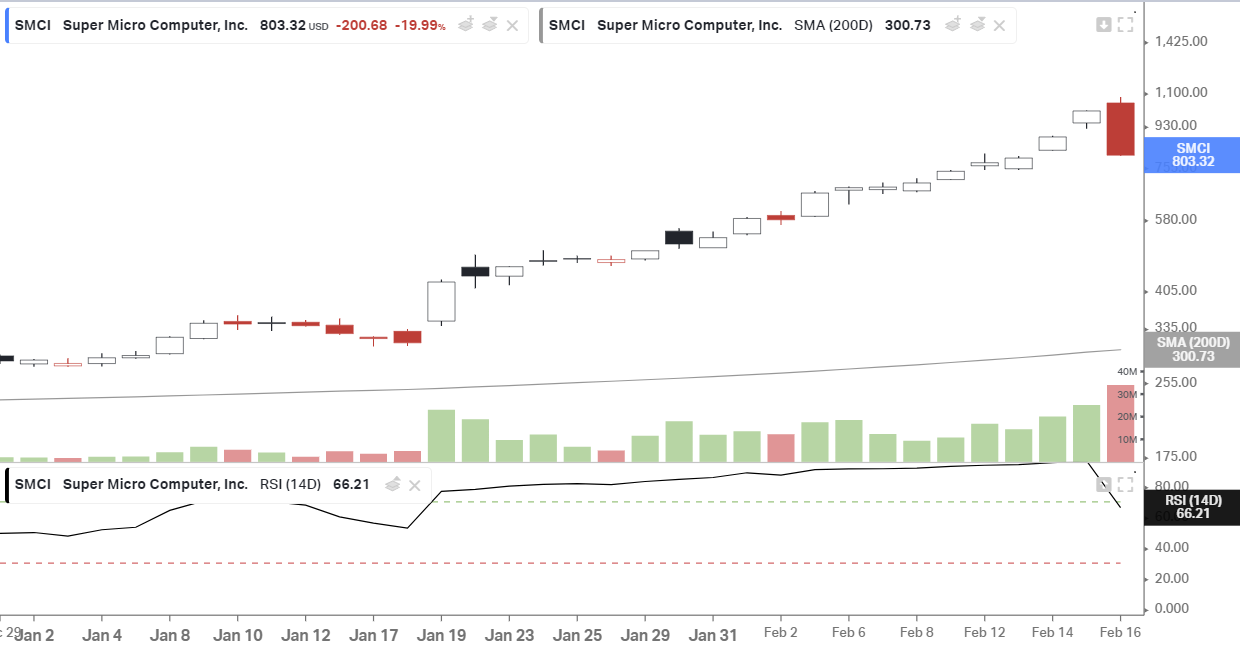

SMCI

Supermicro stock went parabolic on a ‘gamma squeeze’. That means investors were buying loads of call options forcing market makers to delta hedge and buy the stock up.

SMCI broke this Friday and dropped 20%. That’s going to change the vibe.

The stock’s rapid rise is seen by some as a sign of an coming Semiconductor and AI bubble.

It’s one of the most overbought stocks on the planet (it technically hit 100 last week).

You can see the result of that demand for shares in average volume in the chart below.

We like SMCI fundamentally, but stocks cannot go to infinity.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Digital Assets

67 days until the halving and #bitcoin is doing its thing.

On Bitcoin miners, we believe MARA will lag. Other names that have access to better compute and balance sheets will outperform.

MSTR has a near record premium to NAV. Microstrategy is likely to issue new shares and buy more bitcoin.

Long bitcoin and short MSTR is an interesting pair trade concept.

Better yet, long Bitcoin in a ‘discount to NAV’ trust (where you can still get 30%+ off in certain trusts) is even better.

An even better way to make money is via certain liquid token and hedge fund strategies.

We have done an excellent job at Lumida Wealth with our public equities as compared to the S&P and QQQ.

When I look at my passive crypto portfolio, however, the gains crush our equity returns.

We are broadening out the set of strategies and sub-advisors we work with to execute crypto strategies. These are high risk / high reward strategies.

We are still in Phase 2 of the cycle – this year should do well for crypto more generally with the Etheruem ETF and halving.

Lumida is deploying an offering soon which allows you to maintain control and custody of your private keys. We can suggest transactions which you then approve on your wallet. Stay tuned

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Quote of the Week

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” – Paul Samuelson

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.