Nuclear Renaissance, AI LLMs Masters Chess

Here’s a preview of what we’ll cover this week:

-

Macro: US Consumer & Retail Sales, 30-Year Mortgage Rate

-

Markets: Google and Amazon are going Nuclear

-

Company Earnings: ANF Momentum, Nvidia

-

AI: Productivity & AI, AGI delay

-

Digital Assets: Stripe Expands Horizons

-

Weekly Insights: Google DeepMind Masters Chess with an LLM

What a week it has been! We made several key appearances, and are preparing to deliver even more valuable insights at next weeks RWA conference. Here’s a quick recap:

-

Tuesday: We explored NVIDIA and AI alongside our macro market perspective in the OTM episode.

-

Wednesday: Our ‘AI Rise’ podcast episode was highlighted by Zero Hedge.

-

Friday: Ram had a livestream interview with Yahoo Finance about Tesla and NVDA.

Zero Hedge Recognition

Join Ram Ahluwalia and Andrew Brill as they discuss how AI will revolutionize industries, creating significant opportunities for some while presenting existential challenges for others. Tune in now!

Yahoo Finance

As the AI race heats up, Ram Ahluwalia, Lumida Wealth Management CEO, joins Catalysts to discuss how the competition may weigh on Nvidia (NVDA).

Check out the full interview here.

On the Margin: The Economy is in Goldilocks

Don’t miss the latest episode: The Economy is in Goldilocks!

In this episode, Ramshares his macro perspective on the markets, explaining why he believes we’re currently in a Goldilocks phase and his approach to asset allocation.

We also explore topics such as NVIDIA and AI, factor investing, and the importance of risk-adjusted returns.

Macro

The S&P continues to climb the wall of worry and hit new highs.

Last week, we described the ‘four phases’ and noted that we are entering a phase of Optimism.

People are starting to recognize that maybe there isn’t a recession after all.

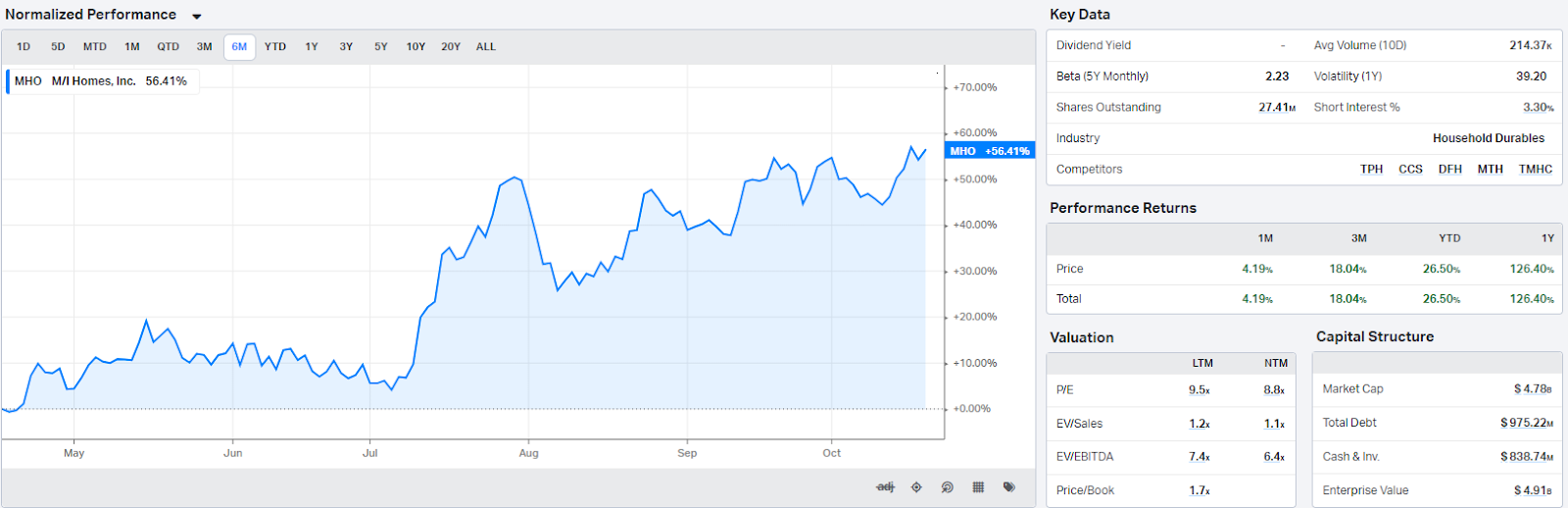

Last Sunday, I wrote this on Twitter and shared our retail favorite Abercrombie & Fitch which enjoyed a nice rally:

We did in fact get a nice retail sales beat.

US Consumer & Retail Sales

The consumer is strong, and expectations are low.

There is a vibecession. I believe it’s caused by a general anxiety.

Cost of living is higher. There are geopolitical concerns around China, Russia-Ukraine, and the Middle East. And there is an election.

Still, Mr. Market is focused on earnings.

Tell me the direction of corporate earnings and you are 70% of the way there in determining the direction of the market.

We also don’t see any ‘exogenous shock’ that can trip up this bull market – even with high valuations. The Fed is cutting into a Goldilcoks.

Non-Consensus: Back to Mag 5?

We do believe retailers are an interesting area of focus.

We also picked up Amazon in recent weeks and a number of Mag 5 names – including Microsoft.

We believe S&P earnings will do fine this quarter, and these names have lagged the 495 other stocks (apart from Nvidia).

We will see how these firms report soon. If Netflix is any indication, they should do just fine.

30-Year Mortgage Rate

30-Year Mortgage Rate jumps to 7.25%, the highest level since July

This is the great irony. The Fed cut rates and inadvertently created a tightening.

The 10-year rising has caused mortgage rates to also rise.

Thus far, homebuilders have shrugged off rising mortgage rates.

I’m not exactly sure how long that will continue. We still like homebuilders longer-term – there is a significant housing shortage and lumber and labor costs are favorable. But, there can be delays between one part of the market and another.

A good example recently was natural gas prices. We saw natural gas prices roll over and then a week later we see one of the leading natural gas firms Chenerie (LNG) roll over.

We continue to own our favorite homebuilder, M/I Homes, and recognize we may get a pull back.

Markets

Quick Thoughts on the Market

Before diving into this section, be sure to watch this brief 10-minute video:

Quick Thoughts on the Market. Themes and rotations we like going into Q4.

FIRST ORDER THINKING

1) Own the S&P

Second Order Thinking:

2) Own capex receivers (Semis)

Third Order Thinking;

3) Own the leader $NVDA

Fourth Order Thinking:

4) Own CoreWeave

Fifth Order Thinking:

5) Own utilities & natural gas $NVGS

Sixth Order Thinking;

Uranium + Nuclear Renaissance

6) Call Lumida Wealth

If you are looking for a holistic wealth manager that seeks to combine investment excellence with tax strategies, now is an excellent time to reach out as we get into Q4 positive seasonality. Email marc@lumida.com for more.

Google Goes Nuclear

First Microsoft wants to ink a deal with Three Mile Island operator.

Now Google wants to get into nuclear.

The nice thing about Uranium is that it has a built in “burn mechanism” called radioactive decay.

See my interview with ASPI CEO below and the Lumida Wealth Nuclear Renaissance thesis.

Stay ahead of the trends and subscribe to our pod at Youtube, Spotify, or Apple ‘Lumida Non-Consensus Investing’

We are believers in the Nuclear Renaissance thesis and have a whitepaper on it here.

However, in the very near term, the nucelar theme is now approaching Consensus.

I can see it by the record number of people downloading our whitepaper!

Amazon Goes Nuclear

Amazon Web Services CEO Matt Garman says Amazon is investing over $500 million in SMR nuclear reactors due to it being a safe technology with the ability to provide gigawatts of power for data centers and address the shortfall of wind and solar projects.

The reality is that wind and solar are not reliable enough to drive energy needs today.

Where we are now, though, I’d say it is not wise to chase Uranium names which have re-priced quickly in two weeks.

I’m investing in the opposite direction now: solar energy.

Most other newsletters are probably touting their favorite nuclear names now after the near-term move is mostly done. Not unlike China a few weeks ago.

First Solar

We picked up First Solar which is resting at the 200 day at around $200 / share.

The business has a forward PE of 11.6x – cheap by S&P standards – and a trailing PE of 17.9x.

If the business can hit its analyst earnings expectations and hold the current valuation multiple, this should generate a nice return in one year’s time.

The biggest risk to clean energy names is politics.

Clean energy names have been pummeled as Trump’s polling climbs on sites like Polymarket.

FSLR rose 13% the day after the first Presidential Debate when many polls suggested that voters thought Vice President Harris performed better than President Trump in the debate.

Take a look at the Clean Energy ETF ICLN for example:

It’s in the dumps. When we look at that, we see a name that is on the lower end of its range.

The risk is that if Trump is re-elected then the Inflation Reduction Act – and the loads of tax credits attached – which benefits FSLR may be repealed.

We believe much of that news is priced in. And that’s less likely is Elon Musk also stands to benefit from the very same tax credits.

The company also has plants in Republican areas: Ohio, Louisiana, and Alabama. They spend plenty of money on lobbying (which makes me wince but I get it).

Trump has also re-stated his support for Solar including during the debate. This debate on solar energy seems mostly theatrical.

However, if Trump does win as betting markets suggest, one should expect we’d get a price drop. That’s a price drop I would want to purchase more shares on.

Further, Trump’s proposed tariffs on China would help the name.

Holders have of clean energy stocks are demoralized and brutalized with a number of false starts.

The sector has had most of this year to form a base and shake out weak holders.

Something you may not know about First Solar.

It’s biggest customers are hyperscalars – the large megacap tech companies that are investing in Datacenters. The other customer set includes Utilities.

We like businesses with high quality customers.

First Solar has a customer backlog that includes Microsoft, Google, and Apple. We like businesses with backlogs also. The backlog extends thru 2030.

These customers also have a self-imposed mandate to hit carbon-zero objectives by 2030. Nuclear is too slow, and solar will play a key role.

First Solar generated $1 Bn in revenue and a 25% YOY increase. The EPS per share has beat Wall Street expectations.

Take a look a the stocks valuation history. The forward multiple is at 11.7x – the lowest in recent period was 11x.

Mr. Market is overly pessimistic on the name.

Eventually, First Solar will price in political risk much in the same way China continued to rally despite Trump gaining in betting markets.

First Solar also occupies a leadership position. Winners tend to keep winning. The moat is driven by a proprietary cadmium telluride technology which provides an edge over silicon-based alternatives.

I asked my AI to pull out key management quotes from the earnings transcript and other key questions.

Management’s view that the election outcome isn’t so important to First Solar’s earnings is notable. I believe the stock is trading off of narratives when ultimately earnings should shine through.

The sales backlog remained strong at 75.9 GW, extending well into 2030 and increasing 0.9 GW from Q1. Management explained on the Q2 Earnings Call that they are being very meticulous as to what they are accepting for orders at this point given their already strong backlog coupled with pricing uncertainties driven by Chinese competition and political uncertainties.

Open AI P&L

Take a look at OpenAI’s P&L.

Have you seen Mr. Wonderful on Shark Tank? He loves royalties that are paid off the top as a % of gross revenue.

Great deal for him, terrible deal for the entrepreneur.

And so it goes for OpenAI.

It looks like there is a 17.5% revenue royalty off of gross revenues paid to Microsoft.

Then the business must pay billions to train models and run models. Those funds go to Nvidia and CoreWeave.

Do you think OpenAI is a great investment at 40x sales?

That isn’t to say OpenAI doesn’t do a 3X here on ‘vibes’.

But, it is simply not a good investment.

After the company goes public, that may well be a close to market top event and you’d want to sell your shares aggressively.

The more well-known and hot an investment, the worse deal and future returns you tend to get.

We’re sticking with our investment in CoreWeave – the leading player ‘AWS for GPU Compute’ which powers Open AI.

We are up 3x in 12 months and have averaged up into the most recent round which closed in September.

Now and then we spot what we believe are attractive private deals. Be sure to join our notification list if you’d like to participate.

I am not permitted to share those deals in advance so you need to establish a relationship before hand.

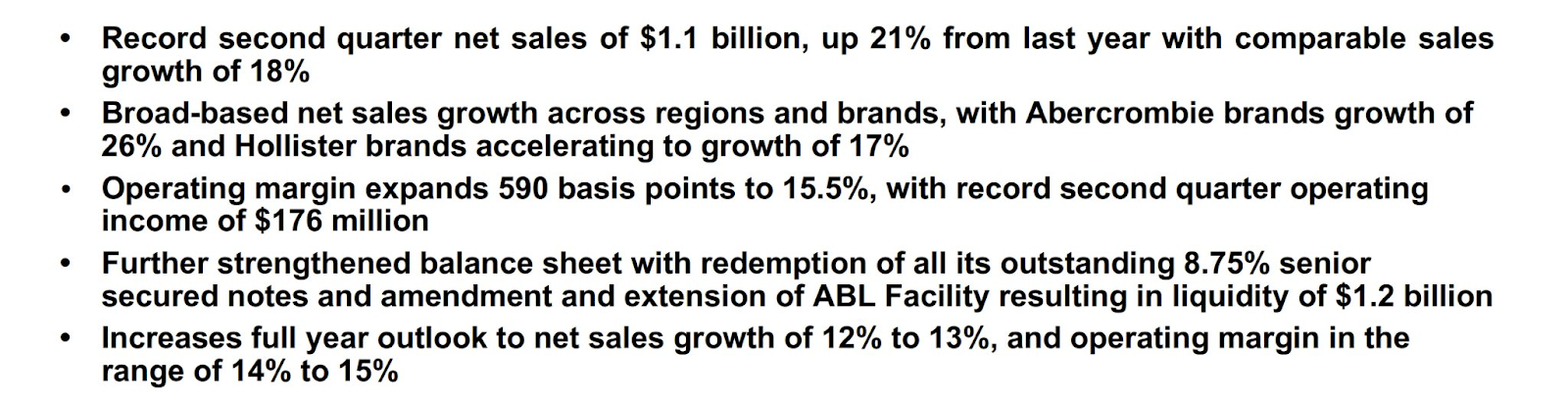

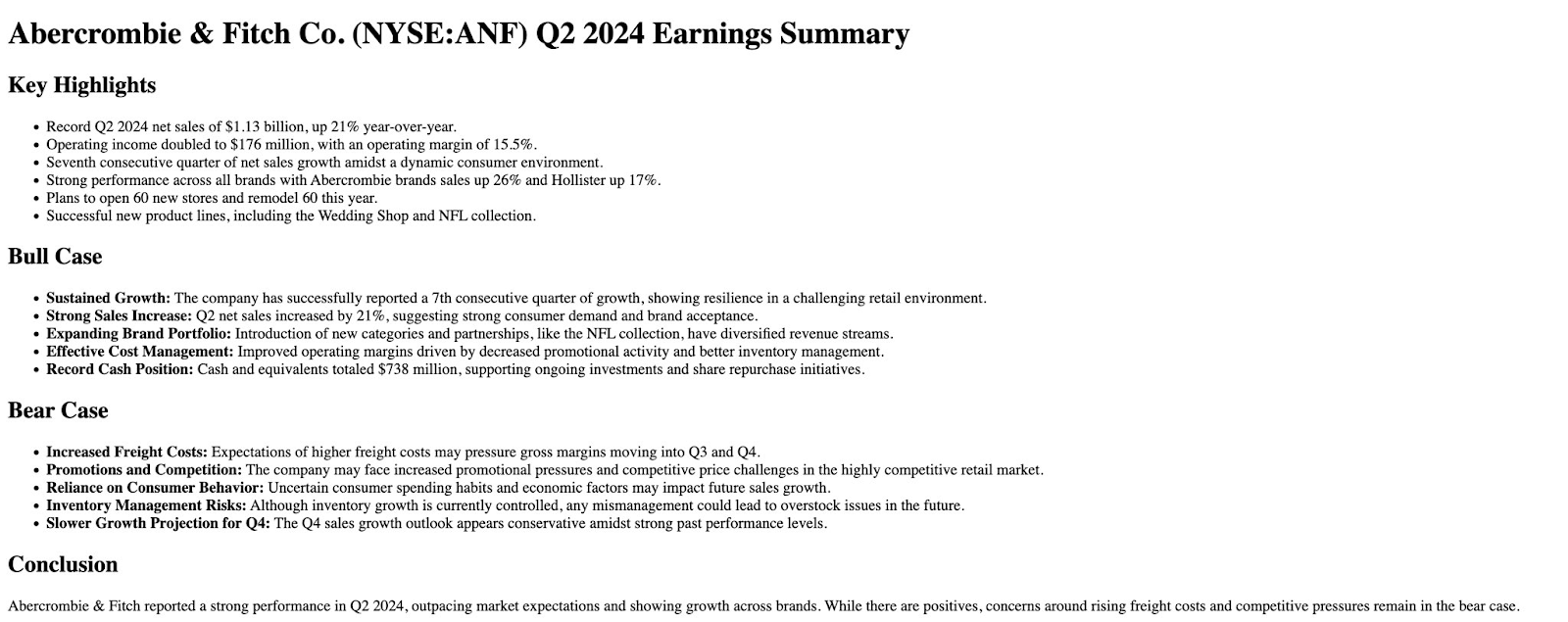

Abercrombine and Fitch Momentum

The hot ball of liquidity appears to be gobbling up our top retail stock call – Abercrombie ANF

(Thank you Citadel 🫡)

I dropped in a few notes from our AI and internal research so you can see why I like it

Note: ANF looks like it is pulling back after the frenetic buying this past week. No need to chase, be patient and wait for the entries to come to you.

Nvidia

We wrote multiple times this year Nvidia has good odds of being the most valuable company in the world.

And here we are.

The call we made in March.

Healthcare Stocks Wrecked

I’ve been busy this weekend researching the highest quality assets in the healthcare space.

The category corrected significantly on negative reports from United Health, Elevance, CVS and others.

Much of this stems from an increase in utilization on Medicare Advantage.

This is a complex topic and I may need to dedicate all of next weeks newsletter to this or create a special video to unpack it.

My headline conclusions are: it is increasingly difficult for insurance companies to make money offering insurance.

The incentives are for consumers to consume more care, and for physicians to order more tests.

That dynamic won’t change anytime soon.

The best way to play the dislocation in healthcare is on certain leading providers of testing equipment and integrated care providers such as Kaiser Permanente.

These integrated care providers do not face the conflicts of interest between insurers and care providers as the costs and benefits of both are internalized.

Unfortunately, Kaiser Permanente is a non-profit and not publicly traded.

More to come on this topic… I may need to do a long-form video as this is a complex topic.

We do believe there are strong opportunities emerging…

AI

Productivity & AI

GS: We Expect Productivity Growth of Around 1.7% Over the Next Few Years, Followed by a Larger Boost From Artificial Intelligence Later This Decade and Next

AGI delay

Demis Hassabis says AGI, artificial general intelligence, is still 10 years away because 2 or 3 big innovations are required and the next one is agent-based systems.

We believe the timeline is closer to 4 to 5 years…

Google DeepMind’s Chess Mastery

Google Deepmind trained a grandmaster-level transformer chess player.

The AI does not use a decision-tree search algorithm.

Sometimes the most transformative innovations start as a toy…

“For most of the nearly thirty years I have run Third Point, the market has been inexorably climbing a wall of worry.” – Daniel S. Loeb

As Featured In