AI: Diving into OpenAI vs Anthropic financial growth metrics. RTZ #1038

Today, a deeper dive into the financial operating and capital expenditure models at the two leading LLM AI companies.

Yesterday, I covered the dramatic pruning at OpenAI of its two-year old AI video App Sora. And the discontinuation of its $1 billion investment partnership with Disney, around licensed content for that app.

As I stressed then, the move underlines a shift away from consumer AI product efforts at OpenAI, couched by senior management as reducing ‘side quests’.

All to focus on the main prize: to compete head on with sibling LLM AI company Anthropic, the ‘Pepsi’ vs its own ‘Coke’. And do so, on the enterprise side of the AI Tech Wave opportunity.

In particular, the focus now seems to be on a ‘Super-App’ that combines its latest language models, ChatGPT, Codex app, and its AI browser, into a desktop super AI app.

The better to compete with Anthropic’s runaway successful products Claude Code and Cowork on the enterprise side. As I described in a separate post, even OpenAI core partner Microsoft is using Claude Code in a co-bundled and re-branded Copilot Cowork as a premium $99 tier over its Office 365 bundled offerings to over 450 million users worldwide.

Both companies are of course sprucing up their financials ahead of mega-IPOs planned later this year. And also against the $1.25+ trillion offering by Elon Musk’s SpaceX/xAI, which is expected to file its IPO with the SEC in a few days.

Given all this, it’s useful to assess what we know about the financial growth metrics and costs at Anthropic vs OpenAI in particular, both more direct competitors than SpaceX/xAI. Particularly due to the diversity of businesses at Elon Musk’s companies.

The Information compares the two LLM AI companies’ financial dynamics in “The Math Behind Anthropic’s Mad Revenue Growth”:

“OpenAI and Anthropic’s remarkable revenue growth has invited scrutiny of how the AI startups are tallying the headline-making figures they have privately or publicly disclosed.”

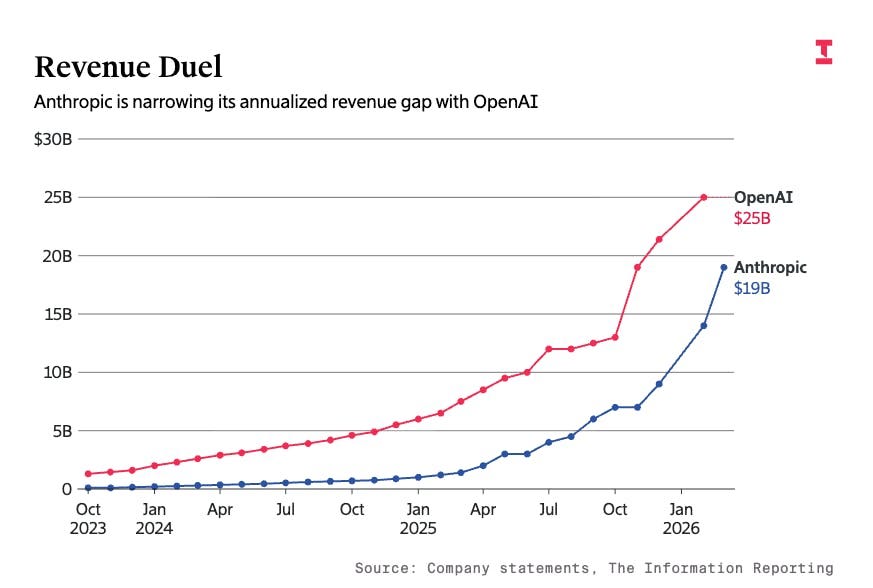

“Last month, OpenAI’s annualized revenue jumped to $25 billion, nearly four times higher than a year earlier. Anthropic has grown even faster: At the end of last month, Anthropic crossed $19 billion in annualized revenue—about 14 times higher than a year earlier. If the trend lines continue, it isn’t unfathomable to imagine Anthropic catching up to OpenAI over the next year or so!”

The ARR methodologies are similar and not apples to oranges:

“Both companies take a similar approach to calculating annualized revenue. OpenAI multiplies its total revenue for a recent four-week period by 13, which equals 52 weeks —or a full year, according to a person with direct knowledge of its finances.”

“Anthropic calculates its annualized revenue by taking the last four weeks of application programming interface revenue and multiplying it by 13, and then adding another figure: its monthly recurring chatbot subscription revenue multiplied by 12, according to a person with direct knowledge of Anthropic’s finances. The monthly figure used to calculate recurring subscriptions is based on the number of active subscriptions that day, said the person.”

“In any case, this should put to rest speculation on X that Anthropic’s annualized sales accounting may be wildly different or less valid than OpenAI’s. It’s not.”

“While annualized sales can be questionable because the metric is usually much bigger than actual revenue, using annualized revenue may be justified in the case of OpenAI and Anthropic. That’s because of the meteoric revenue spikes they have experienced.”

Thus the focus can then shift to revenue growth metrics for both companies:

“Still, for mature companies sprinting toward public offerings, total revenue is what really matters. And there are meaningful differences in how these companies disclose revenue figures privately to current and prospective investors.”

Both have meaningful partnerships with other companies, including Microsoft.

“OpenAI shares 20% of its revenue with Microsoft due to their multifaceted business arrangement, but OpenAI’s financial statements count sales before the company gives Microsoft its slice. (OpenAI expects revenue to jump to about $30 billion for all of this year, from $13.1 billion last year.)”

“Anthropic, which generated around $4.5 billion in revenue last year, doesn’t have an agreement to share a slice of all of its revenue with a cloud provider. But, like OpenAI, it has agreed to share some of the revenue from cloud partners’ sales of its models with those partners.”

“The two firms’ cloud revenue-sharing deals differ in major ways, however, as does the way they count such revenue in their financial statements.”

And then we get the revenue recognition details:

“OpenAI, for instance, receives 20% of Microsoft sales of OpenAI models to Azure cloud customers. The ChatGPT maker counts that figure as revenue in its financial statements. (It’s not yet clear how OpenAI will account for revenue it generates through Amazon Web Services as part of a new deal between the companies.)”

“Anthropic counts such revenue very differently from OpenAI. AWS, Microsoft and Google each resell Anthropic’s Claude models to their respective cloud customers, but Anthropic reports all those sales as revenue, before the cloud providers receive their share of those sales. Instead, Anthropic accounts for the cloud provider payouts in its sales and marketing expenses, as we’ve previously reported here.”

The Microsoft/OpenAI relationship offers a differentiating twist:

“The revenue accounting differences between OpenAI and Anthropic come down to which company is considered a “principal” that controls the service that is delivered to customers. OpenAI considers Microsoft to be the principal for the Azure OpenAI service, according to a person with knowledge of the relationship, because Microsoft directly controls the Azure service in question and also has exclusive rights to use OpenAI’s intellectual property.”

“Anthropic, meanwhile, considers itself to be the principal in its relationship with cloud partners. They don’t control the delivery of the models and products and instead are so-called distributors, according to a person with knowledge of the situation.”

“Bottom line: Both companies are following Generally Accepted Accounting Principles, but because the nature of their deals with cloud providers differ markedly, they are at odds when accounting for sales through these companies. Unfortunately, we aren’t able to calculate how much that hurts OpenAI’s top line.”

All that just get to the top line comparisons. Before we get to costs, capital investments, margins, and free cash flows. And there, Anthropic has a relative advantage due to its enterprise focus, while OpenAI until now has been focused aggressively on both consumer and enterprise markets.

“Perhaps other metrics like free cash flow are a better metric to compare these AI labs. In that respect, Anthropic fares better, expecting to turn cash flow positive as soon as 2028, two years earlier than OpenAI projects it would.”

Both companies of course face rising costs of rolling out AI Data Center Compute infrastructure via a range of partners. And that has predictable downward pressures on gross margins for both companies. Anthropic started to see this recently as they’re ramping up AI capex a bit behind OpenAI.

The Information noted that trend in “Anthropic Lowers Gross Margin Projection as Revenue Skyrockets”:

“Anthropic last month projected it would generate a 40% gross profit margin from selling AI to businesses and application developers in 2025, according to two people with knowledge of its financials. That margin was 10 percentage points lower than its earlier optimistic expectations, though it’s still a big improvement from the year before.”

“The lower-than-expected gross profit margin resulted from the costs of running Anthropic models for paying customers, in a process known as inference, on servers from Google and Amazon. Those inference costs were 23% higher than the company had anticipated, the projections showed. Anthropic calculates gross margins by subtracting inference costs and other costs of selling its products.”

Again, these are common expenses for both OpenAI and Anthropic, running at difference levels and pace. With OpenAI running ahead of Anthropic due to their longer and wider focus on multiple markets. And pruning some to sharpen focus on some markets.

But AI data center capex ramps are the bane of the near-term existence of both OpenAI and Anthropic, as I’ve detailed recently.

“The data show how both companies’ reliance on renting specialized servers from cloud providers makes it harder to generate a net profit, which is why they are taking steps to create or control server hardware themselves and are in the process of raising tens of billions of dollars to shore up their balance sheets. OpenAI just announced it would launch ads to subsidize nonpaying users of its chatbot.”

“If Anthropic also counted inference costs for Claude chatbot users that don’t pay for a subscription, its gross margin would be about 38%, or a few percentage points lower than for paid users, based on The Information’s analysis.”

“In contrast, OpenAI projected a gross margin of around 46% in 2025, including inference costs of both paying and nonpaying ChatGPT users. Nonpaying users make up roughly 95% of the chatbot’s roughly 900 million weekly active users.”

Which gets us to what we know about the margin projections from both companies:

“Anthropic has previously projected gross margins above 70% by 2027, and OpenAI has projected gross margins of at least 70% by 2029, which would put them closer to the gross margins of publicly traded software and cloud firms. But both AI developers also spend a tremendous amount on renting servers to develop new models—training costs, which don’t factor into gross margins—making it more difficult to turn a net profit than it is for traditional software firms.”

“The inference costs are in addition to costs from training the models. Anthropic last month expected its costs for training its AI models for 2025 to be roughly $4.1 billion, up roughly 5% from its summer projections. OpenAI, meanwhile, expected to spend $9.4 billion on compute for training its AI models last year.”

And of course there is sprucing going on ahead of any IPO fillings:

“Both companies have taken steps to get those costs under control. Anthropic recently agreed to purchase $21 billion of Google’s tensor processing units to gain more control over the hardware it uses so it can reduce its computing costs. OpenAI, meanwhile, has been developing a server chip to power inference—mainly for running ChatGPT—that it plans to use in the coming years as an alternative to expensive Nvidia chips.”

“On Wednesday, OpenAI Chief Financial Officer Sarah Friar said that the upcoming inference chip was “taped out,” implying the company had shared the final design with its chip manufacturer.”

Which gets us to the net possible results, and possible comparisons of the two:

“Anthropic recently projected that its 2025 revenue would be $4.5 billion, marginally lower than its previous optimistic projection of nearly $4.7 billion. Still, its 2025 revenue is nearly 12 times higher than its 2024 revenue of $381 million, a remarkable growth rate for a company that size. (In comparison, OpenAI generated revenue of more than $13 billion in 2025, up from around $3.7 billion in 2024.)”

“The revenue gap between the companies has been shrinking, as OpenAI is currently generating a little more than double what Anthropic is generating per month: $1.7 billion compared to $750 million.”

Again, the differences also lie in the products and markets:

“Anthropic’s AI for coding and white-collar tasks—Claude Code and Cowork, respectively—has been the biggest AI success story of the past month, drawing parallels with the excitement OpenAI generated among businesses and software engineers in early 2023.”

“Anthropic privately has disclosed it has at least nine customers spending more than $100 million a year on its products, according to one of the people. Microsoft’s spending on Anthropic, for instance, was on track to hit $500 million, in part for Microsoft’s GitHub CoPilot. Other popular coding tools such as Cursor and Cognition also are large customers of Anthropic.”

“About 86% of Anthropic’s 2025 revenue was expected to come from its sale of AI models to such businesses through an application programming interface, the company estimated. The rest of its revenue comes from subscription revenue from its Claude chatbot, which competes with ChatGPT.”

OpenAI is of course also focused on the enterprise:

“OpenAI, too, has been gaining business customers. In fact, its enterprise business may still be larger than Anthropic’s when including API and chatbot sales to businesses. OpenAI generates roughly 40% of revenue from business customers, according to a person familiar with its financials. That implies roughly $5.2 billion of OpenAI’s revenue is from business customers, as compared to Anthropic’s $3.9 billion.”

The question for investors both private and soon public, is how long do these investments stretch out ahead of revenues.

“While both companies’ sales are growing at a nearly unprecedented rate, some lenders are apprehensive about lending money to data center projects involving such firms because they don’t plan to generate free cash flow until near the end of the decade.”

“Their cash burn has left equity investors in the firms undaunted, however. Anthropic as of mid-December expected to lose about $5.2 billion, based on its earnings before interest, taxes, depreciation and amortization, last year, according to its most optimistic projections. OpenAI earlier projected a loss of $21.2 billion before interest and taxes, though its projected cash burn was less than half that amount.”

And the continued efforts by both to top up more funding ahead of their respective IPOs;

“Anthropic is in talks to raise more than $10 billion at a $350 billion valuation before the financing in a round led by Singapore’s GIC and Coatue Management. Nvidia and Microsoft previously committed to investing up to $10 billion and up to $5 billion, respectively, in Anthropic. Investors last valued Anthropic at $170 billion before the financing in a $13 billion September round.”

“OpenAI, meanwhile, is in talks to raise as much as $100 billion in a round that could value it around $750 billion before the investment.”

All this is to highlight the intense efforts at both companies, to get ready for their big public debuts. With Elon’s SpaceX/xAI filing any day now, we are soon going to get a lot more numbers and details.

Soon to better compare and contrast the top three ‘AI Mega-Startup’ business models and prospects, thus far this AI Tech Wave. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here)